Whether you’re buying or selling a house, here’s something to think about that most people don’t. Your decision doesn’t just impact your life and your family’s, it sparks a ripple effect that has a positive impact on your entire community.

Every year, the National Association of Realtors (NAR) puts out a report that breaks down the financial impact that comes from people buying and selling homes.

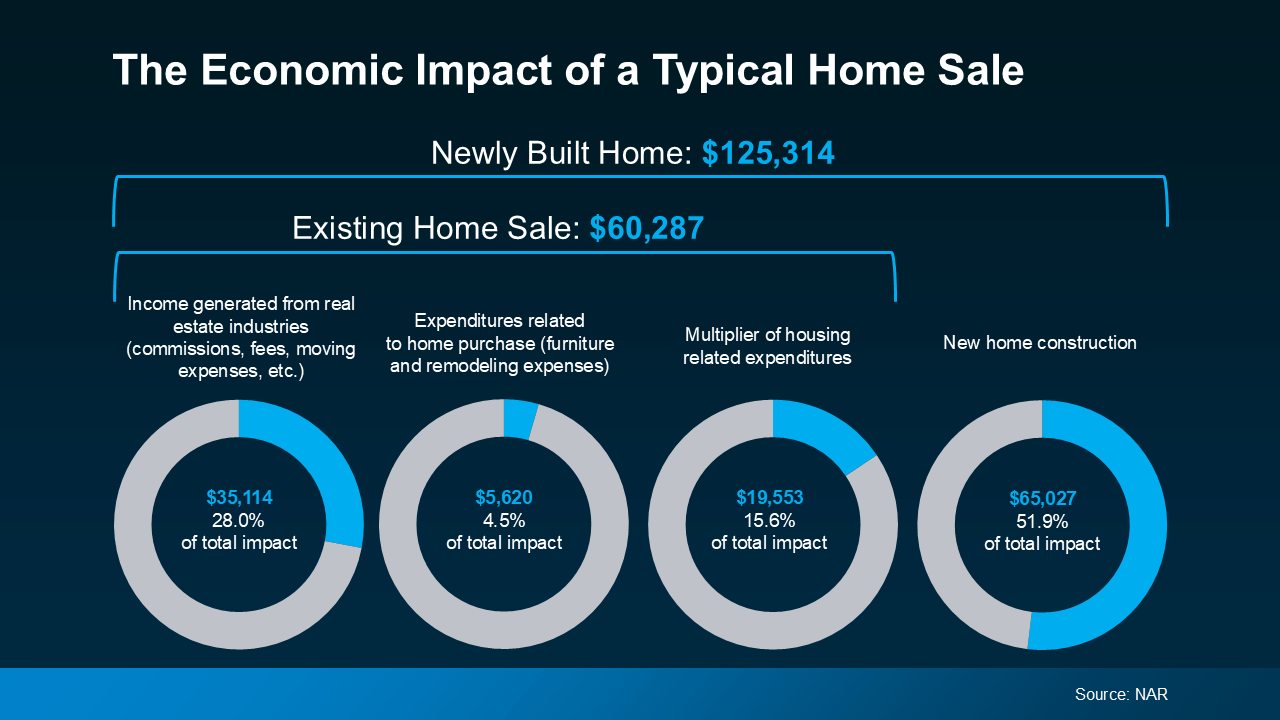

The data shows that if you buy an existing (previously lived-in) home, you’re giving the local economy a boost of just over $60K. And if you buy a newly built home, that number goes up to over $125K (see visual below):

That’s because of all the people needed to build, fix up, and sell homes. Robert Dietz, Chief Economist at the National Association of Home Builders (NAHB), explains how the housing industry adds jobs to a community:

“. . . housing is a significant job creator. In fact, for every single-family home built, enough economic activity is generated to sustain three full-time jobs for a year . . .”

When you think about it, it makes sense. Behind every home sale is a network of people involved, including contractors, city officials, real estate agents, lawyers, specialists, and more. Everyone has a job to do to help make sure your deal goes through.

Put simply, when you buy or sell a home, you’re helping out your neighbors. So, your decision to move doesn’t just meet your needs; it supports their families, strengthens your town, and shapes the future of your community.

Imagine walking through the front door of your next home, knowing your decision helped a local contractor keep their crew working or a small business thrive. Remember that feeling as you make your decision this year.

Bottom Line

Moving isn’t just a personal milestone – it’s an investment in your community, too. If you’re ready to make a move, connect with a local real estate agent. You’ll make a difference for more people than you know.

What’s most important to you as you prepare to buy or sell your house this year?

Homeowner’s insurance is a must-have to protect what’s probably your biggest investment – your home. And while you never want to think about worst-case scenarios, the right coverage is basically your safety net if something goes wrong. Here’s how it helps you.

Covers Repairs and Rebuilding Costs: If your home is damaged by fire, storms, or other covered events, your policy helps pay for repairs or even a full rebuild.

Protects Your Belongings: Many policies can also cover personal items like furniture, electronics, and clothing if they’re stolen or damaged.

Provides Liability Coverage: If someone gets injured on your property, homeowner’s insurance can help cover medical bills or legal expenses.

In the simplest sense, it gives you peace of mind. Knowing you have protection against unexpected events helps you worry less. And with such a big purchase, having that reassurance is a big deal.

And while your first insurance payment will be wrapped into your closing costs, you’ll want this to be a part of your budget beyond closing day too. That’s because it’s a recurring expense you’ll have once you get the keys to your home.

Here’s what you need to know to help you budget for this important part of homeownership today.

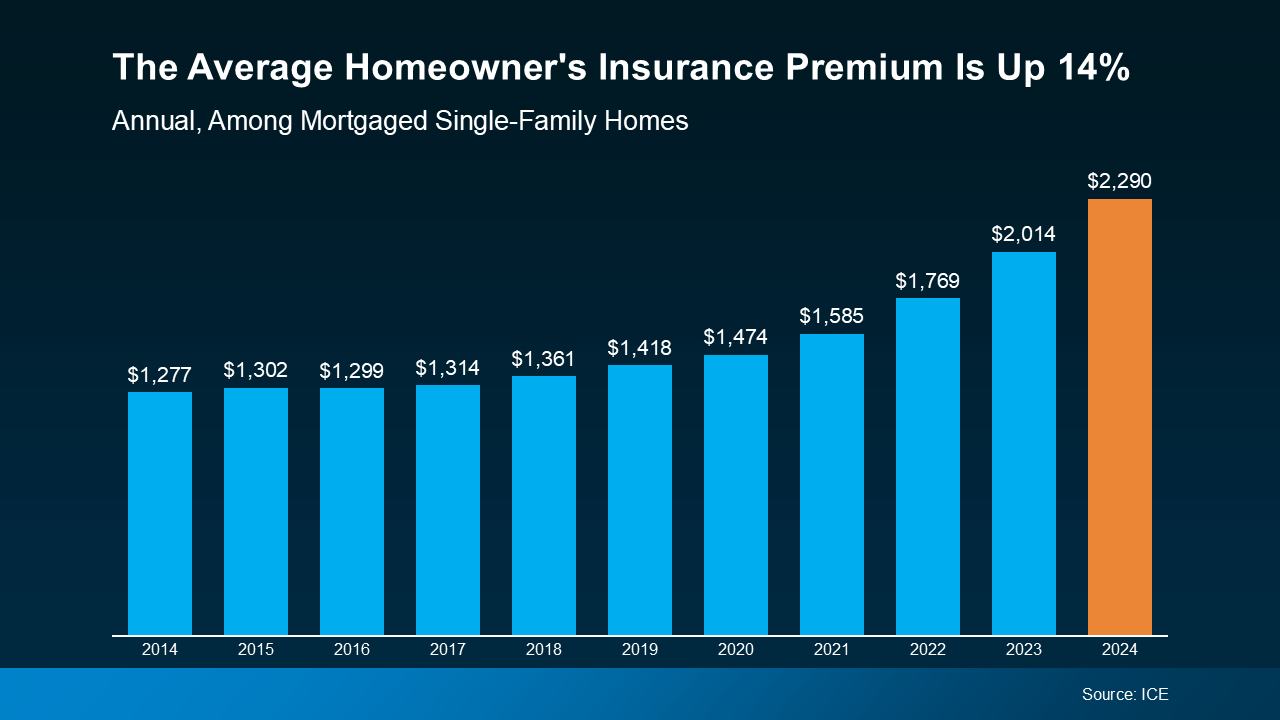

Costs and Claims Are Rising

In recent years, insurance costs have been climbing. According to Insurance.com, there are four big reasons behind the jump in premiums:

More severe weather events and wildfires are leading to higher claims.

Insurance companies are pulling out of high-risk areas, reducing options for homeowners in some states.

Past rate increases haven’t kept up with the rise in claims.

The cost to rebuild or repair homes has gone up due to higher material and labor costs.

Basically, disasters are happening more often, repairs cost more, and insurers have to adjust their rates to keep up. Data from ICE Mortgage Technology helps paint the picture of how the average yearly premium has climbed over the last decade (see graph below):

What You Can Do About It

Homeowner’s insurance is a must to protect your home and your investment. But with costs rising, you’ll want to do your homework to balance the best coverage you can get at the best price possible.

Homeowner’s insurance rates vary widely based on location, provider, and coverage. Shop around and compare quotes before settling on a policy. And don’t forget to ask about discounts. Things like security systems or bundling with auto insurance could help lower your insurance costs.

Bottom Line

When you’re planning to buy a home, it’s important to look beyond just your mortgage payment. You’ll also want to budget for your homeowner’s insurance policy. It gives you a lot of protection against the unexpected. And while it’s true those costs are rising, there are things you can do to try to get the best price possible.

What’s your biggest concern when it comes to budgeting for homeownership? Talk to an agent to make sure you’re set up for success.

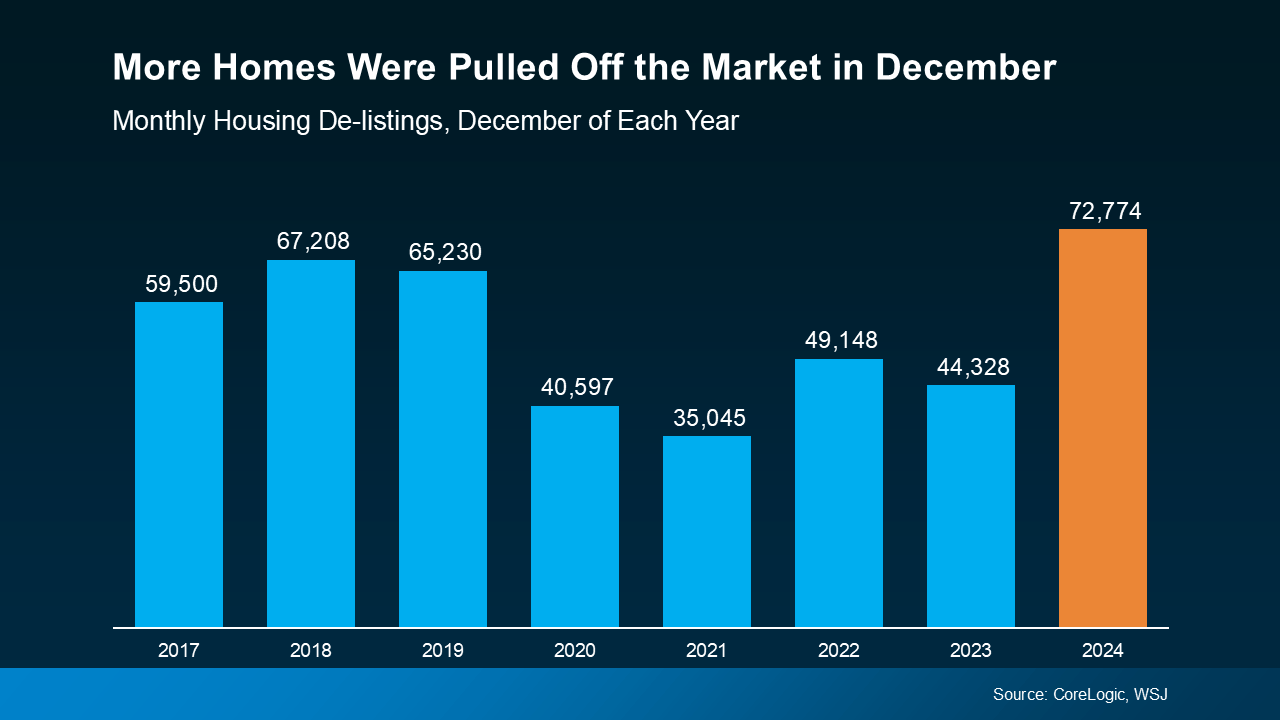

If you took your house off the market in late 2024, you’re not the only one. Newsweek reports that data from CoreLogic and the Wall Street Journal (WSJ) says nearly 73,000 homes were pulled from the market in December alone – that’s more than any other December going all the way back to 2017 (see graph below):

Whether it was because offers weren’t coming in, the timing around the holidays felt overwhelming, or they wanted to see if the market would improve in the new year – a lot of other homeowners decided to press pause, too.

But now, with spring fast approaching, it’s time to reassess. The market is already picking up, and waiting any longer to jump back in may only mean you’d face more competition from other sellers down the road.

Why Now Could Be the Right Time

Selma Hepp, Chief Economist at CoreLogic, explains that some of those sellers may have pulled their listings late last year with the goal of trying again this spring:

“Another reason for a step back could be that sellers wanted to wait and see how spring home buying season goes, and if mortgage rates fall, which would bring more home buyers and competition back in the market.”

That’s because spring is when buyer demand is typically at its highest point for the year. More people start their home search once the weather warms up. They’re eager to close on a home so they can move in during the summer. So, it’s a great window for sellers. It means more buyers.

And while mortgage rates haven’t fallen dramatically, they have come down some in recent weeks. Early signs already show buyers are becoming more active as a result. Since January, demand has picked up – and that should continue as spring draws even closer.

What To Do Differently This Time

Start by checking the status of your listing agreement. Because even if you pulled your listing, you may still be under contract. And until your listing expires, your agent or brokerage is your best resource on what else you could try to get it sold. Realtor.com offers this advice:

“If you aren’t sure of the status of your listing, whether active, expired, or withdrawn, take a look at your listing agreement and talk to your real estate agent.”

If your contract is still active, now’s the perfect time to reconnect with your agent to explore strategies to get your home sold this time around. If your contract has expired and you’re considering other options, reach out to a trusted real estate professional who can help you figure out where to go from here.

Either way, take some time to reflect on your last experience. What held you back from getting it sold before? And what can you do to improve your chances this time around?

Be sure to include your agent in this thought process. They’ll give you an objective point of view and some advice based on what may have gone wrong last time, like:

Your Pricing Strategy: Did buyers overlook your house because it was priced too high? Your real estate agent can help you analyze the latest sales in your area to make sure you’re hitting the right number. Believe it or not, you could actually be leaving money on the table by not pricing competitively. When it’s priced appropriately for the market, your opportunities for multiple offers and buyer competition increase.

Your Marketing Approach: Was your home staged to look its best? Did you use a skilled photographer for your listing photos? Small tweaks can make a big difference in how buyers see your house. Something as simple as taking new photos now that it’s spring can help your house show better than it did in the winter listing.

Offering Concessions: Were you willing to offer incentives to buyers? As the supply of homes for sale grows, more sellers are entertaining the idea of concessions or incentives to get the deal done. If you weren’t open to those conversations, that may have been a factor, too.

Showings and Flexibility: Did you have limits on when buyers could see the home? If your house is accessible and available, you’ll likely get more offers.

Bottom Line

If your house didn’t sell last year, spring may be your second chance. With buyer activity rising, it’s the perfect time to talk to an agent about coming back into the market with a fresh strategy.

What do you want to do differently this time around? Talk to your agent to go over your options and make a plan.