The Latest Expert Forecasts for the 2025 Housing Market

After several years of rising home prices and volatile mortgage rates, it looks like the housing market will start to head in a more normal direction in 2025 – at least according to the latest forecasts. And if you’ve been thinking about making a move, that means the uncertainty that could’ve been throwing off your plans may be coming to a close.

Here’s a look at the latest expert forecasts on two of the biggest factors expected to shape the market in the year ahead.

Will Mortgage Rates Come Down?

Everyone’s keeping an eye on mortgage rates, and they’re projected to settle in the mid-6% range by the end of the year (see chart below):

But remember, rate projections will continue to shift as new information becomes available. Expert forecasts are based on what they know right now. If there’s increasing uncertainty around inflation, employment, government policies, or other key economic drivers, mortgage rates will move. So, don’t get caught up in the exact numbers or try to time the market. Instead, focus on the fact that a bit more stability in rates isn’t a bad thing – and even a small change can help your bottom line.

But remember, rate projections will continue to shift as new information becomes available. Expert forecasts are based on what they know right now. If there’s increasing uncertainty around inflation, employment, government policies, or other key economic drivers, mortgage rates will move. So, don’t get caught up in the exact numbers or try to time the market. Instead, focus on the fact that a bit more stability in rates isn’t a bad thing – and even a small change can help your bottom line.

A trusted lender and your RE/MAX® agent will make sure you always have the latest data and the context to understand what it really means for you and your monthly payment.

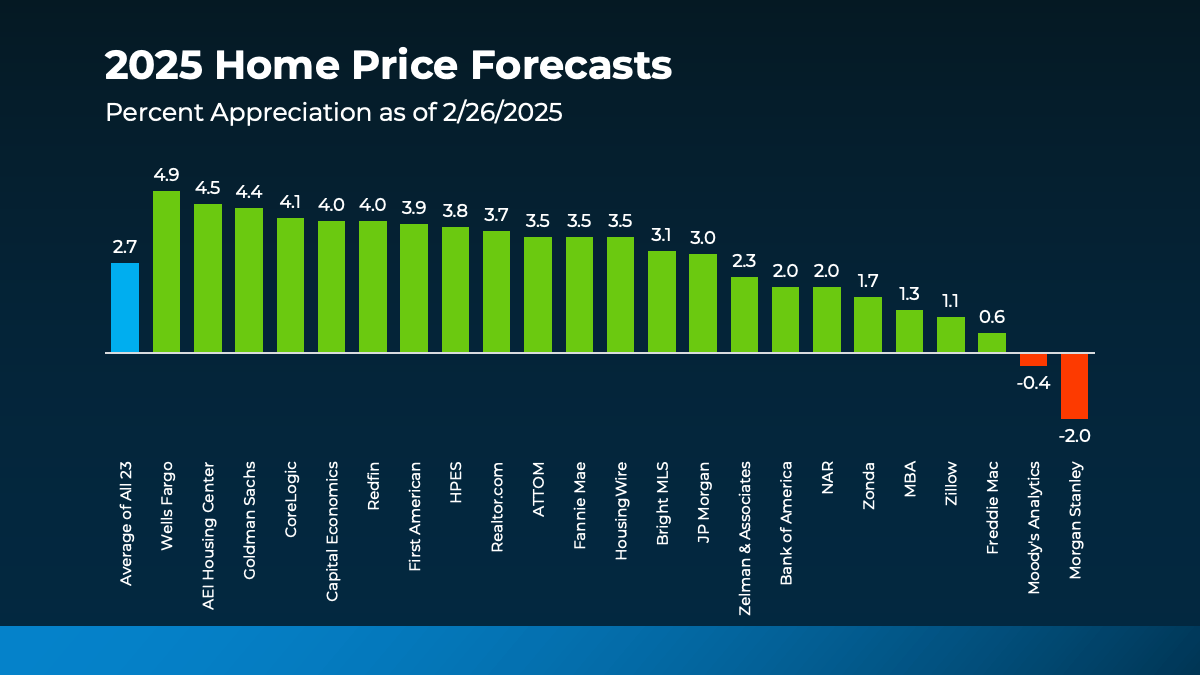

Will Home Prices Fall?

The short answer? Not likely. Home prices are projected to keep rising in most areas – just at a slower, more normal pace. If you average the expert forecasts together, you’ll see prices are expected to go up by about 2.7%, with the majority of the projections hitting somewhere in the 3 to 4% range by the end of the year. And that’s a much more typical and sustainable rise (see graph below):

So, don’t expect a sudden drop that’ll score you a big deal if you’re thinking of buying this year. While that may sound disappointing if you’re hoping prices will come down, refocus on this. It means you won’t have to deal with the steep increases the market felt in recent years, and you’ll also likely see any home you do buy go up in value after you get the keys in hand. And that’s a good thing.

So, don’t expect a sudden drop that’ll score you a big deal if you’re thinking of buying this year. While that may sound disappointing if you’re hoping prices will come down, refocus on this. It means you won’t have to deal with the steep increases the market felt in recent years, and you’ll also likely see any home you do buy go up in value after you get the keys in hand. And that’s a good thing.

Prices normalizing is a welcome sign after years of unsustainable home price growth. It means we’re moving into a healthier market. And that’s something we haven’t been able to say in a while.

And if you’re wondering how it’s even possible prices are still rising, here’s your answer. It all comes down to supply and demand. Even though there are more homes for sale now than there were just a year ago, there still aren’t enough houses on the market to keep up with all the buyers out there.

Keep in mind, though, the housing market is hyper-local. So, this will vary by area. Some markets will see even higher price appreciation. And some may see prices level off or even dip slightly. In most markets though, prices will continue to rise (as they usually do).

If you want to find out what’s happening where we live, you need to lean on your local RE/MAX® agent who can explain the latest trends and what they mean for your plans.

Bottom Line

The housing market is shifting, and the experts say 2025 will move toward a more normal, healthier pace for the year. With rates stabilizing and home prices rising at a more typical and sustainable rate, it’s all about staying informed and making a plan that works for you.

What mortgage rate are you waiting for to make your move? Tell me your number, and I’ll show you how the math works out for your monthly mortgage payment. It may be more attainable this spring than you think.