Kasey and Andrew started their 5 month search at the beginning of what I refer to as “The Wild, Wild, West”. It was a crazy time with so few homes available and so many home buyers competing for each one. These buyer’s had the added stress of being first time home buyers, and without the bags of cash that so many other buyers seems to have, we had to be creative with our offers!

In the end, they found this perfect ranch home! Perfectly updated, and ready to move in, it even included a fantastic outdoor space in the back with a fenced yard for the future fur-baby! They couldn’t have been happier!

Not to mention, they were able to win this home without bidding tens of thousands of dollars over asking price! Kasey and Andrew for the WIN! Enjoy your new home!

Congratulations to Genevieve, Andrew, Jonah and Roosevelt, on their new home purchase! It wasn’t easy for this family, and after falling in love with the first home they saw, and then losing out to the competition, they became even more determined to find their first home!

Heeding my wisdom in telling them that there will always be another home, this ranch that was even better than the one they lost out on, and it was even closer to Grandma and Grandpa! The BEST news is that with some out-of-the-box thinking and a creatively crafted offer, they beat all the competition and snagged this home, making their dream a reality! Oh, and did I mention that, like some of my other buyers, they did NOT have to pay over asking price!?

There are more homes for sale today than at any time last year. So, if you tried to buy a home last year and were outbid or out priced, now may be your opportunity. The number of homes for sale in the U.S. has been growing over the past four months as rising mortgage rates help slow the frenzy the housing market saw during the pandemic.

Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains why the shifting market creates a window of opportunity for you:

“This is an opportunity for people with a secure job to jump into the market, when other people are a little hesitant because of a possible recession. . . They’ll have fewer buyers to compete with.”

Two Reasons There Are More Homes for Sale

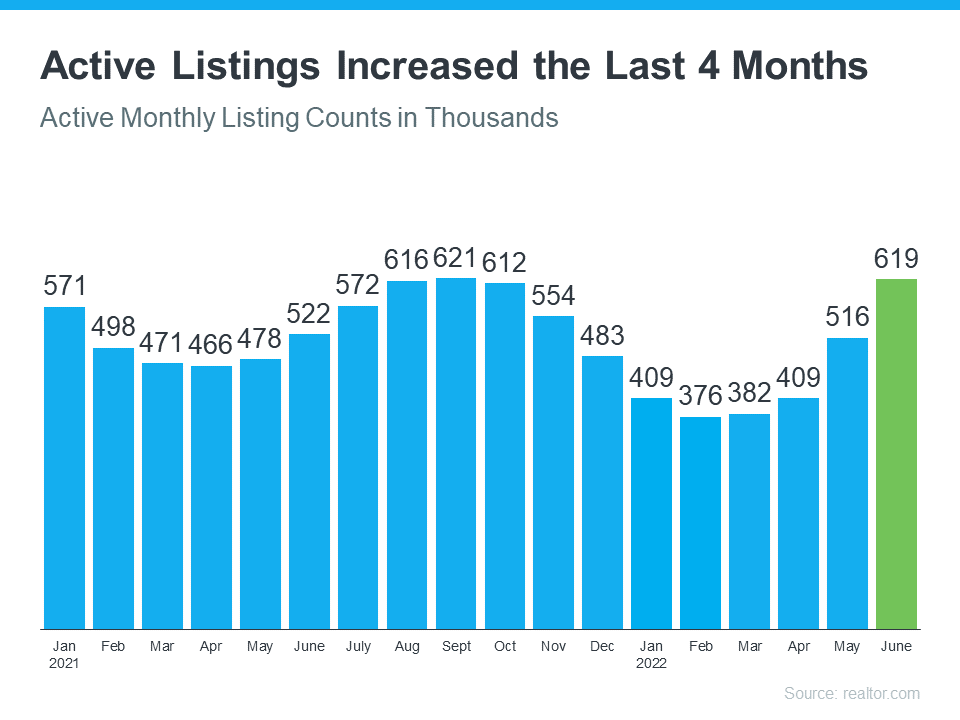

The first reason the market is seeing more homes available for sale is the number of sales happening each month has decreased. This slowdown has been caused by rising mortgage rates and rising home prices, leading many to postpone or put off buying. The graph below uses data from realtor.com to show how active real estate listings have risen over the past four months as a result.

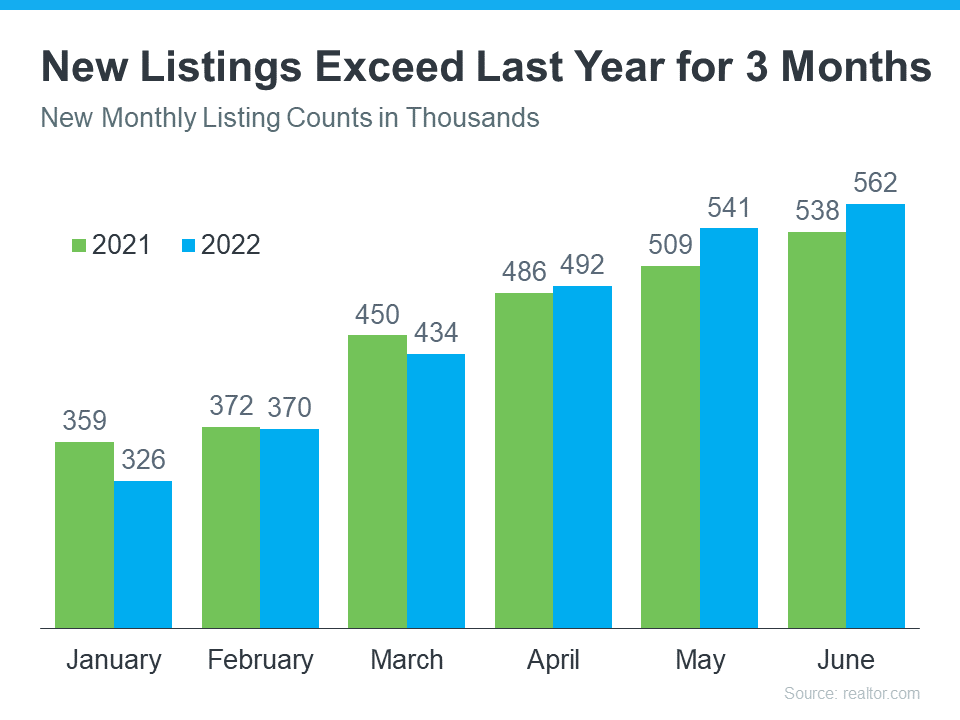

The second reason the market is seeing more homes available for sale is because the number of people selling their homes is also rising. The graph below outlines new monthly listings coming onto the market compared to last year. As the graph shows, for the past three months, more people have put their homes on the market than the previous year.

Bottom Line

The number of homes for sale across the country is growing, and that means more options for those thinking about buying a home. This is the opportunity many have been waiting for who were outbid or out priced last year.

Mortgage rates are much higher today than they were at the beginning of the year, and that’s had a clear impact on the housing market. As a result, the market is seeing a shift back toward the range of pre-pandemic levels for buyer demand and home sales.

But the transition back toward pre-pandemic levels isn’t a bad thing. In fact, the years leading up to the pandemic were some of the best the housing market has seen. That’s why, as the market undergoes this shift, it’s important to compare today not to the abnormal pandemic years, but to the most recent normal years to show how the current housing market is still strong.

Higher Mortgage Rates Are Moderating the Housing Market

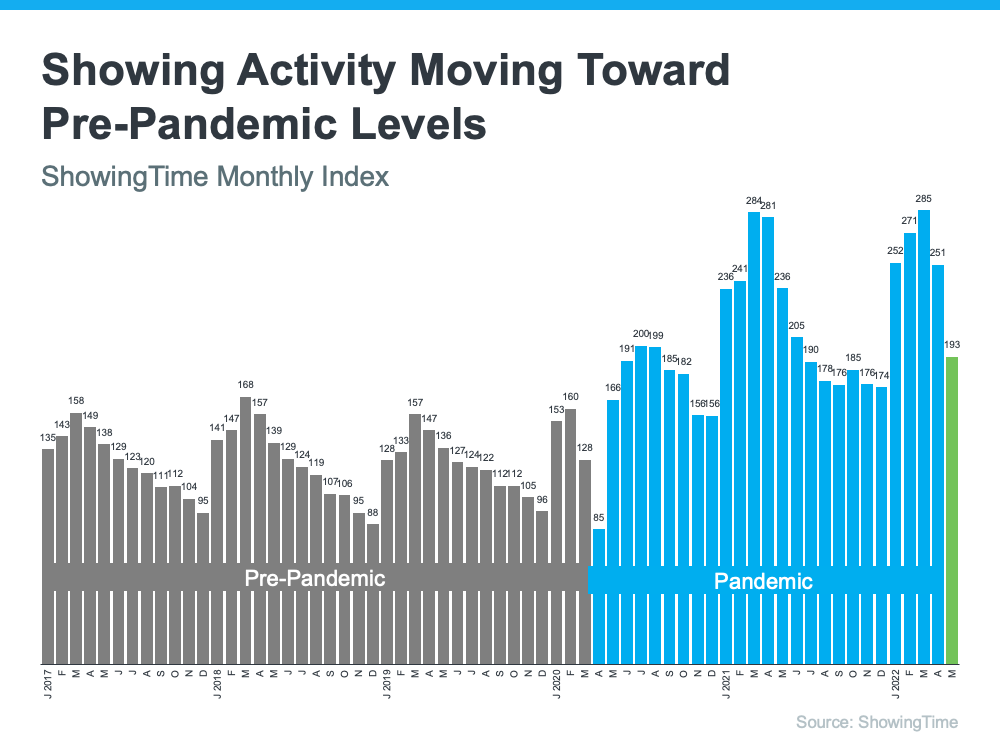

The ShowingTime Showing Index tracks the traffic of home showings according to agents and brokers. It’s also a good indication of buyer demand over time. Here’s a look at their data going back to 2017 (see graph below):

Here’s a breakdown of the story this data tells:

The 2017 through early 2020 numbers (shown in gray) give a good baseline of pre-pandemic demand. The steady up and down trends seen in each of these years show typical seasonality in the market.

The blue on the graph represents the pandemic years. The height of those blue bars indicates home showings skyrocketed during the pandemic.

The most recent data (shown in green), indicates buyer demand is moderating back toward more pre-pandemic levels.

This shows that buyer demand is coming down from levels seen over the past two years, and the frenzy in real estate is easing because of higher mortgage rates. For you, that means buying your next home should be less challenging than it would’ve been during the pandemic because there is more inventory available.

Higher Mortgage Rates Slow the Once Frenzied Pace of Home Sales

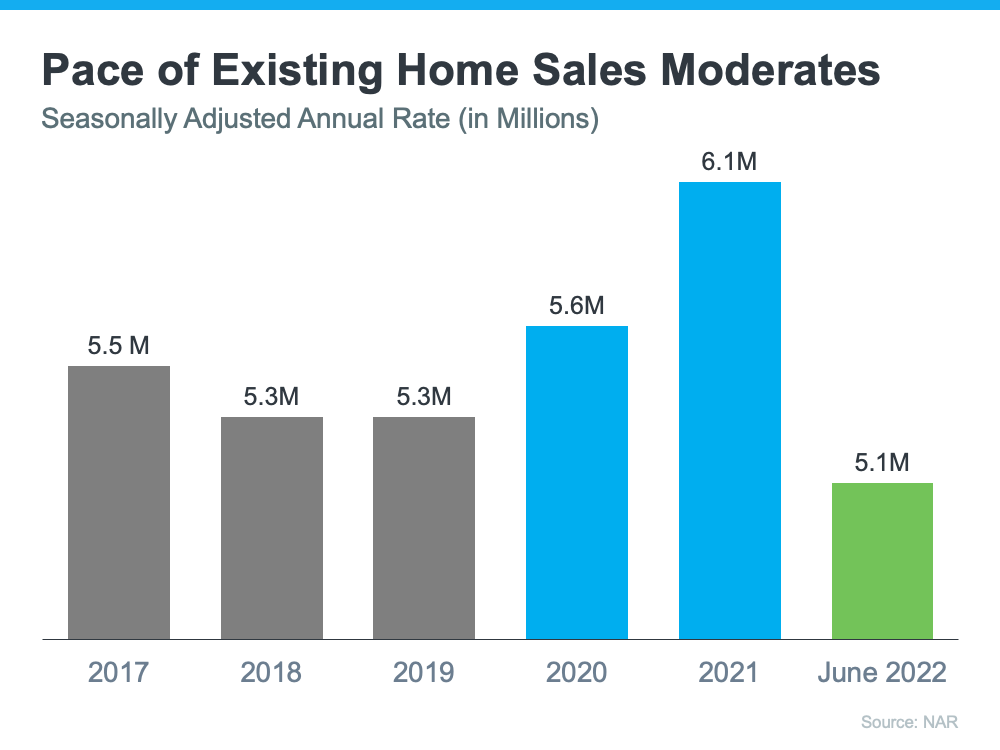

As mortgage rates started to rise this year, other shifts began to occur too. One additional example is the slowing pace of home sales. Using data from the National Association of Realtors (NAR), here’s a look at existing home sales going all the way back to 2017. Much like the previous graph, a similar trend emerges (see graph below):

Again, the data paints a picture of the shift:

The pre-pandemic years (shown in gray) establish a baseline of the number of existing home sales in more typical years.

The pandemic years (shown in blue) exceeded the level of sales seen in previous years. That’s largely because low mortgage rates during that time spurred buyer demand and home sales to new heights.

This year (shown in green), the market is feeling the impact of higher mortgage rates and that’s moderating buyer demand (and by extension home sales). That’s why the expectation for home sales this year is closer to what the market saw in 2018-2019.

Why Is All of This Good News for You?

Both of those factors have opened up a window of opportunity for homeowners looking to move and for buyers looking to purchase a home. As demand moderates and the pace of home sales slows, housing inventory is able to grow – and that gives you more options for your home search.

So don’t let the headlines about the market cooling or moderating scare you. The housing market is still strong; it’s just easing off from the unsustainable frenzy it saw during the height of the pandemic – and that’s a good thing. It opens up new opportunities for you to find a home that meets your needs.

Bottom Line

The housing market is undergoing a shift because of higher mortgage rates, but the market is still strong. If you’ve been looking to buy a home over the last couple of years and it felt impossible to do, now may be your opportunity. Buying a home right now isn’t easy, but there is more opportunity for those who are looking.