Why Achieving the Dream of Homeownership Can Be More Difficult for Some Americans

Today we take time to honor and recognize the past and present experiences of Black Americans. When it comes to real estate specifically, equitable access to housing has come a long way, but the path to homeownership is still steeper for households of color.

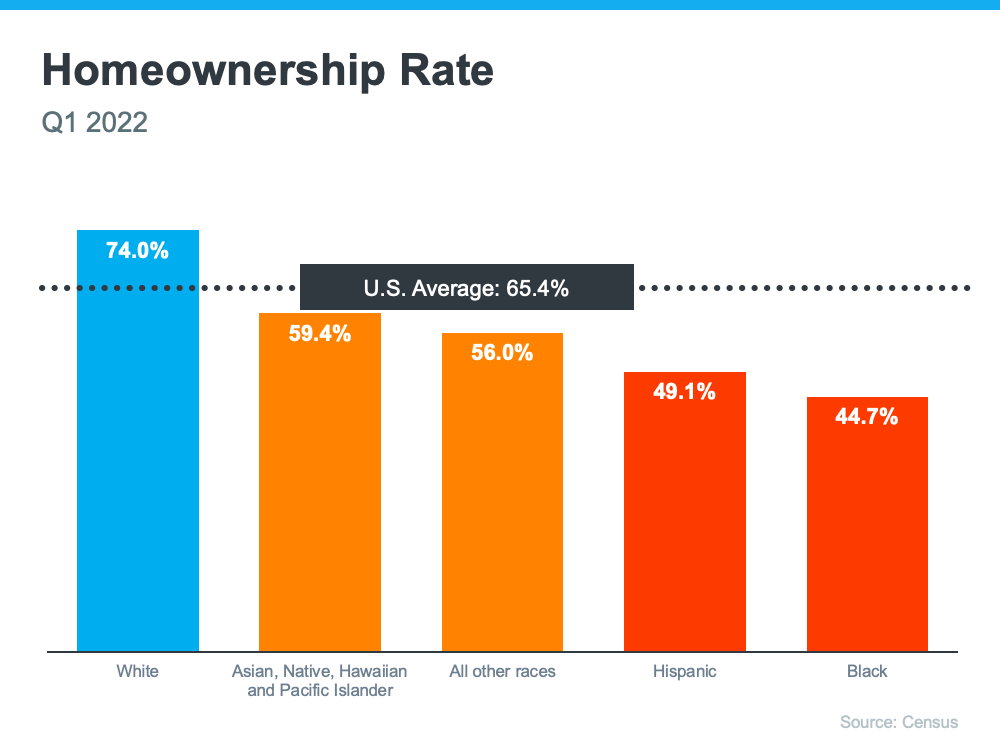

The Gap in Homeownership Rate in America

It’s a more challenging journey to achieve homeownership for some buyers, as shown by the measurable gap between the overall average U.S. homeownership rate and that of non-white groups. Today, Census data shows the lowest homeownership rate persists in the Black community (see graph below):

This graph clearly indicates there’s a gap that still exists in the percentage of people in each community who are able to achieve homeownership.

How Homeownership Impacts Household Wealth

One of the challenges that could make buying a home harder for these groups is how difficult it can be to accumulate wealth. Even today, there are obstacles certain racial and ethnic groups, especially the Black community, still face. A recent article from NextAdvisor explains:

“The median Black household earns 61 cents for every dollar earned by a comparable White household, according to the Economic Policy Institute. This not only makes it more difficult to afford a home, but also to accumulate and pass on generational wealth.”

This can delay or prevent many from achieving homeownership, challenging their ability to grow their net worth and build wealth that can pass down to future generations – a point that’s clear in a 2022 report from the National Association of Realtors (NAR):

“Given that homeownership contributes to wealth accumulation and the homeownership rate is lower in minority groups, data shows that the net worth for these groups is also lower. At $188,200, the net worth of a typical white family was nearly 8 times greater than that of a Black family ($24,100) in 2019.”

It’s important to talk about the experience Black homebuyers may have and the challenges they may face as they pursue their dream of homeownership. The inequity that remains in housing can be a point of pain and frustration. That’s why it’s so important for members of diverse groups to have the right team of experts on their sides throughout the homebuying process.

These professionals aren’t only experienced advisors who understand the market and give the best advice. They’re also compassionate allies who will advocate for your best interests every step of the way. They can point you to important resources and tools that can help you throughout your journey to homeownership.

Bottom Line

Opportunities in real estate improve every day, but there are still equity challenges that many face. Let’s connect to make sure you have an advocate on your side to help you achieve your dream of homeownership.

![More Listings Are Coming onto the Market [INFOGRAPHIC] | Simplifying The Market](https://www.sellingthe608.com/wp-content/uploads/2022/06/20220617-MEM.png)