If you’re a young adult, you may be thinking about your goals and priorities for the months and years ahead. And if homeownership ranks high on your goal sheet, you’re in good company. Many of your peers are also pursuing their dream of owning a home. The 2022 Millennial & Gen Z Borrower Sentiment Report from Maxwell says:

“Many young adults have demonstrated their resolve to embark on the journey toward homeownership soon. More than half of millennials and Gen Zs plan to apply for a mortgage sometime within the next year.”

Let’s take a look at why homeownership makes the top of so many young buyers’ to-do list and what you need to consider to achieve your goals if you’re one of them.

Top Motivators To Buy a Home

Before you start the homebuying process, it’s helpful to know why homeownership is so important to you. The survey mentioned above sheds light on some of the top reasons why younger generations are looking to buy a home. It finds:

No matter which of these resonates the most with you, know there are many financial and non-financial reasons why you may want to buy a home. While your top motivator may be different than that of your friends, they’re all equally valid and worthwhile.

Key Obstacles and How To Overcome Them

Whether your homeownership goals come from the heart or are driven by financial aspirations (or both), it can still be hard to know where to start when you’re looking to buy a home. From understanding the homebuying process, to getting pre-approved, and exploring down payment options, it’s a lot to wrap your head around.

The same Maxwell survey also reveals key challenges for potential buyers. Thankfully, the knowledge and guidance of a trusted real estate professional can help you overcome both. Here’s a look at two of the hurdles potential homebuyers say they face:

1. The Mortgage Process Can Be Intimidating

In the Maxwell study, 33.37% said one of their obstacles was that the mortgage process is confusing or difficult to understand.

“There is a general lack of knowledge about home financing. Mortgages are a complicated topic with no one-size-fits-all answer. It’s difficult to understand the space, let alone determine what the right course of action isbased on your unique financial picture.”

While you may be tempted to do a quick search online to find instant answers to your questions, it may not get you the information you need to understand the full picture. Especially when it comes to financial advice, you want to lean on a true expert. Having trusted professionals on your side can help you to learn what it takes to achieve your dream of homeownership. Not to mention, an expert can give you advice specific to your situation, not generic advice like you’ll find online.

2. It’s Hard To Know How Much You Need To Save

In the Maxwell study, 45.75% believe they don’t have enough saved to cover their down payment or closing cost expenses.

What you may not realize is that, today, there’s a growing number of down payment assistance programs available nationwide to help relieve this pressure. A report from Down Payment Resourcesays:

“Our Q3 2022 HPI report revealed a 1.6% uptick in the number of homebuyer assistance programs available to help people finance homes, raising the number of programs to 2,309, a net increase of 36 over the previous quarter.”

Additionally, as the housing market cools, buyers are regaining some negotiation power and more sellers are willing to work with buyers to help with closing costs. Understanding what’s out there and the options available may help you achieve your dream of homeownership faster than you thought possible.

Bottom Line

If you’re serious about becoming a homeowner, know it may be more in reach than you think. Lean on trusted professionals to help you overcome challenges and prioritize your next steps.

With the rapid shift that’s happened in the housing market this year, some people are raising concerns that we’re destined for a repeat of the crash we saw in 2008. But in truth, there are many key differences between what’s happening today and the bubble in the early 2000s.

One of the reasons this isn’t like the last time is the number of foreclosures in the market is much lower now. Here’s a look at why there won’t be a wave of foreclosures flooding the market.

Not as Many Homeowners Are in Trouble This Time

After the last housing crash, over nine million households lost their homes due to a foreclosure, short sale, or because they gave it back to the bank. This was, in large part, because of more relaxed lending standards where people could take out mortgages they ultimately couldn’t afford. Those lending practices led to a wave of distressed properties which made their way into the market and caused home values to plummet.

But today, revised lending standards have led to more qualified buyers. As a result, there are fewer homeowners who are behind on their mortgages. As Marina Walsh, Vice President of Industry Analysis at the Mortgage Bankers Association (MBA), says:

“For the second quarter in a row, the mortgage delinquency rate fell to its lowest level since MBA’s survey began in 1979 – declining to 3.45%. Foreclosure starts and loans in the process of foreclosure also dropped in the third quarter to levels further below their historical averages.”

There Have Been Fewer Foreclosures over the Last Two Years

While you may have seen recent stories about the number of foreclosures rising today, context is important. During the pandemic, many homeowners were able to pause their mortgage payments using the forbearance program. The program gave homeowners facing difficulties extra time to get their finances in order and, in many cases, work out a plan with their lender.

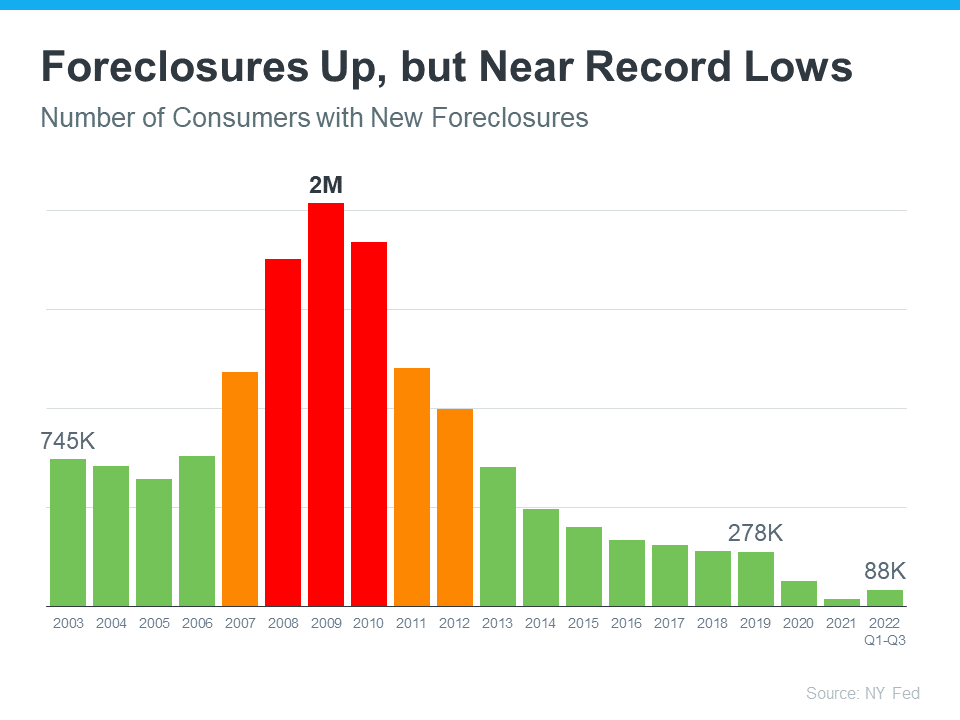

With that program, many were concerned it would result in a wave of foreclosures coming to the market. That fear didn’t materialize. Data from the New York Fed shows there are still fewer foreclosures happening today than before the pandemic (see graph below):

That means, while there are more foreclosures now compared to last year (when foreclosures were paused), the number is still well below what the housing market has seen in a more typical year, like 2017-2019.

And most importantly, the number we’re seeing now is still far below the number we saw during the market crash (shown in the red bars in the graph). The big takeaway? Don’t let a headline in the news mislead you. While foreclosures are up year-over-year, historical context is essential to understanding the full picture.

Most Homeowners Have More Than Enough Equity To Sell Their Homes

Many homeowners today have enough equity to sell their homes instead of facing foreclosure. Due to rapidly rising home prices over the last two years, the average homeowner has gained record amounts of equity in their home. And if they’ve stayed in their homes even longer, they may have even more equity than they realize. As Ksenia Potapov, Economist at First American, says:

“Homeowners have very high levels of tappable home equity today, providing a cushion to withstand potential price declines, but also preventing housing distress from turning into a foreclosure. . . the result will likely be more of a foreclosure ‘trickle’ than a ‘tsunami.’”

A recent report from ATTOM Dataexplains it by going even deeper into the numbers:

“Only about 214,800 homeowners were facing possible foreclosure in the second quarter of 2022, or just four-tenths of one percent of the 58.2 million outstanding mortgages in the U.S. Of those facing foreclosure, about 195,400, or 91 percent, had at least some equity built up in their homes.”

Bottom Line

If you see headlines about the increasing number of foreclosures today, remember context is important. While it’s true the number of foreclosures is higher now than it was last year, foreclosures are still well below pre-pandemic years. If you have questions, let’s connect.

If you’re a homeowner, odds are your equity has grown significantly over the last few years as home prices skyrocketed and you made your monthly mortgage payments. Home equity builds over time and can help you achieve certain goals. According to the latest Equity Insights Report from CoreLogic, the average borrower with a home loan has almost $300,000 in equity right now.

As you weigh your options, especially in the face of inflation and talk of a recession, it’s important to understand your assets and how you can leverage them. A real estate professional is the best resource to help you understand how much home equity you have and advise you on some of the ways you can use it. Here are a few examples.

1. Buy a Home That Fits Your Needs

If you no longer have the space you need, it might be time to move into a larger home. Or it’s possible you have too much space and need something smaller. No matter the situation, consider using your equity to power a move into a home that fits your changing lifestyle.

If you want to upgrade your house, you can put your equity toward a down payment on the home of your dreams. And if you’re planning to downsize, you may be surprised that your equity may cover some, if not all, of the cost of your next home. A real estate advisor can help you figure out how much equity you have and how you can use it toward the purchase of your next home.

2. Reinvest in Your Current House

According to a recent survey from Point, 39% of homeowners would invest in home improvement projects if they chose to access their equity. This is a great option if you want to change some things about your living space but you aren’t ready to make a move just yet.

Home improvement projects allow you to customize your home to suit your needs and sense of style. Just remember to think ahead with any updates you make, as some renovations add more value to your home and are more likely to appeal to future buyers than others. For example, a report from the National Association of Realtors (NAR) shows refinishing or replacing wood flooring has a high cost recovery. Lean on a local professional for the best advice on which projects to invest in to get the greatest return on your investment when you sell.

3. Pursue Your Personal Goals

In addition to making a move or updating your house, home equity can also help you achieve the life goals you’ve dreamed of. That could mean investing in a new business venture, retiring or downsizing, or funding an education. While you shouldn’t use your equity for unnecessary spending, leveraging it to start a business or putting it toward education costs can help you achieve other lifelong goals.

Bottom Line

Your equity can be a game changer. If you’re unsure how much equity you have in your home, let’s connect so you can start planning your next move.

![Winter Home Selling Checklist [INFOGRAPHIC] | Simplifying The Market](https://www.sellingthe608.com/wp-content/uploads/2022/12/Winter-Checklist-MEM.png)