Once your offer is accepted, an inspector will assess the condition of the house, including things like the roof, foundation, plumbing, and more.

That information is incredibly important and paves the way for you to re-negotiate with the seller, as needed. So, you don’t want to skip this step.

An inspection is your chance to avoid costly headaches and get peace of mind. Connect with an agent to talk about other ways to make your offer stand out.

From rising home prices to mortgage rate swings, the housing market has left a lot of people wondering what’s next – and whether now is really the right time to move. There is one place you can turn to for answers you want the most. And that’s the experts.

Leading housing experts are starting to release their projections for the rest of the year. These insights will give you clarity – and a little more optimism than you might expect. Business Insider sums up the forecasts (and why they’re good news for you):

“As mortgage rates go down this year, affordability may improve slightly for homebuyers. Inventory is also expected to grow, which should help moderate price growth and make finding a home easier.”

Let’s break it down.

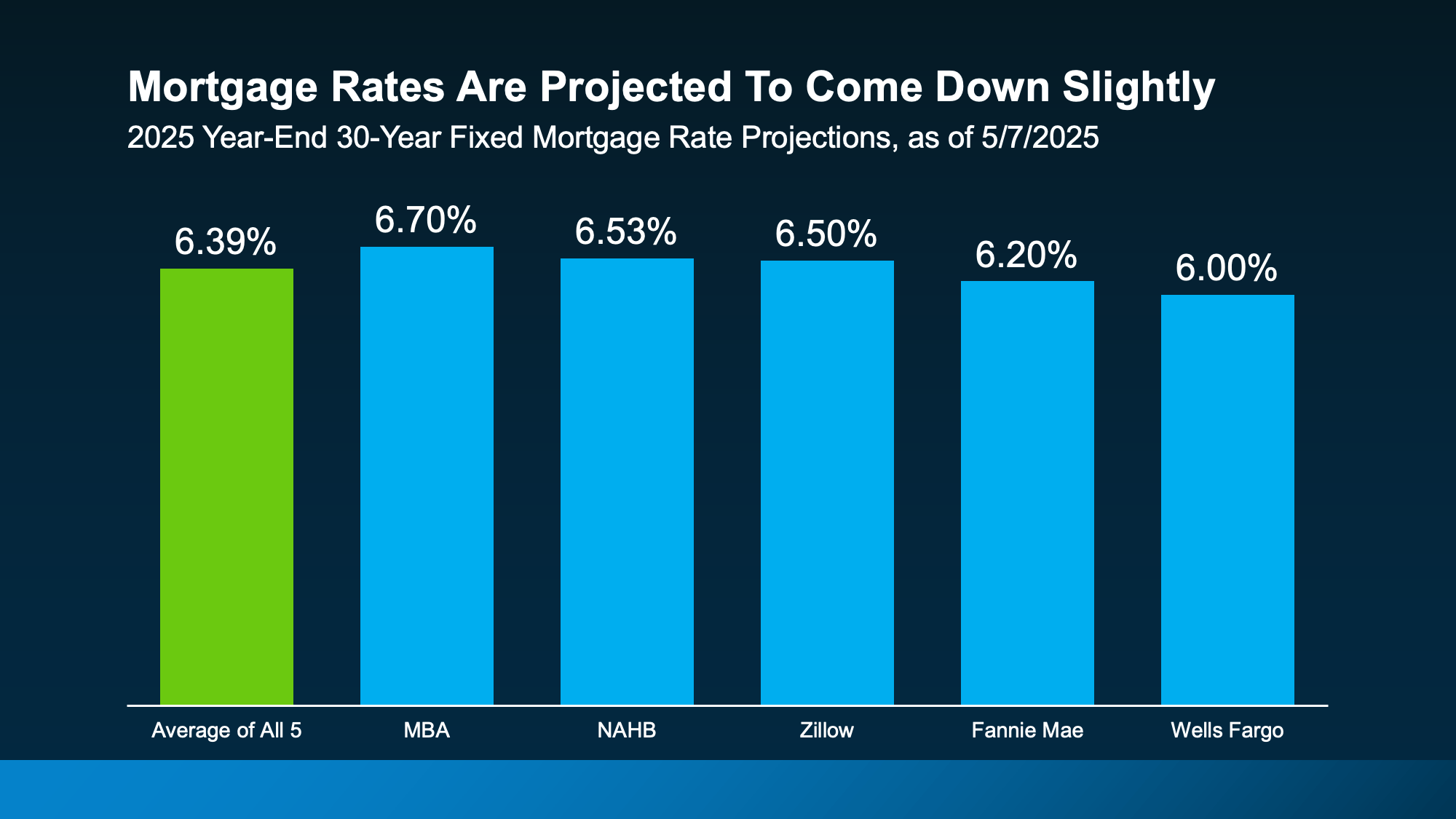

1. Mortgage Rates Should Come Down (Slightly)

While a major drop isn’t on the table, forecasters are calling for a modest decline in rates in the months ahead as the economic outlook becomes more certain. Based on the information we have right now, here’s a look at where they say rates should be by year-end (see graph below):

Even this slight decrease is a welcome change. A seemingly small decline can still help bring down your future mortgage payment and give you a bit more breathing room in your budget.

Just remember, everything from inflation to employment and broader economic shifts will have an impact on where rates go from here. So, don’t try to time the market. And do expect some volatility along the way.

2. Inventory Will Continue To Grow

Inventory has already improved a lot this year. A big portion of the growth the market has already seen is because homeowners are getting tired of sitting on the sidelines. They’ve tried the wait and see approach with rates, and it hasn’t really paid off. And at a certain point, you need to move no matter what the market is doing. This is one reason more homes have been listed lately. And experts say that should continue. As Lance Lambert, Co-founder of ResiClub, says:

“The fact that inventory is rising year-over-year . . . strongly suggests that national active housing inventory for sale is likely to end the year higher.”

If rate forecasts pan out as the experts say, that could be enough to tip some more sellers off the fence and back into the market – giving you even more options for your move.

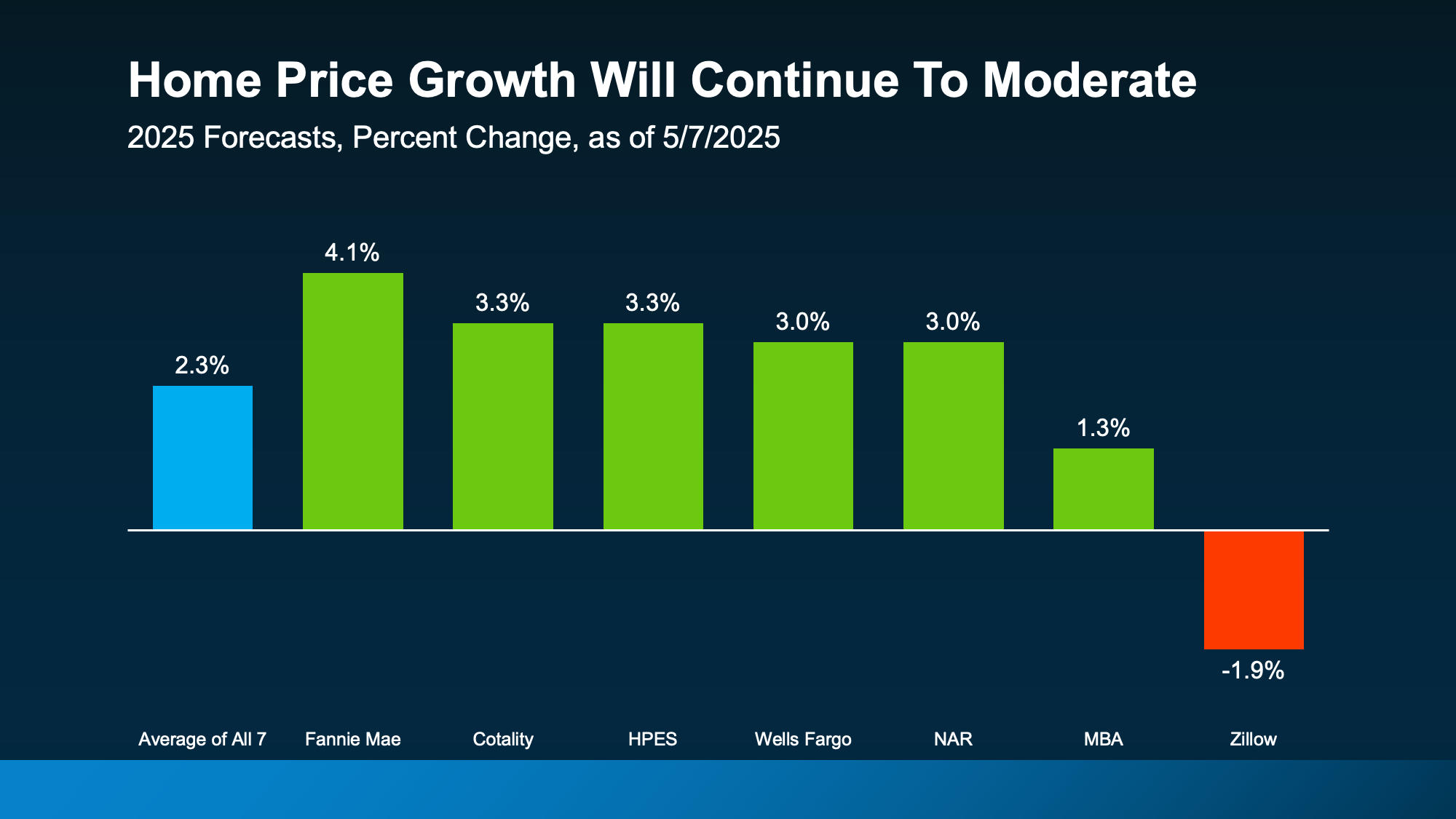

3. Home Prices Are Moderating

As more homes hit the market, there will also be less upward pressure on home prices. Expert forecasts are still calling for growth, but the pace of that growth is slowing down as inventory climbs. The average of all 7 forecasts shows prices will rise about 2% this year (see graph below):

That means you could finally get a little bit of relief from rapidly rising home prices. When you combine the forecast for healthier price growth with projections for slightly lower mortgage rates, that could mean more buying power in the months ahead.

Keep in mind, though, the housing market is hyper-local. So, this is going to vary by area. Some markets will see prices climbing higher. And some may even see prices dip a little if inventory is up significantly in that location. So, lean on a local agent for insights into what’s happening in your area.

Bottom Line

So, if you want or need to move this year, know that the experts say things should start looking up. And an agent can help you take advantage of any market shifts that work in your favor.

As you think ahead to your own move, you may have noticed some houses sell within days, while others linger. But why is that? As Redfin says:

“. . . today’s housing market has been topsy-turvy since the pandemic. Low inventory (though rising) and high prices have created a strange mix: Some homes are flying off the market, while others sit for weeks.”

That may leave you wondering what you should expect when you sell. Let’s break it down and give you some actionable tips on how to make sure your house is one that sells quickly.

Homes Are Still Selling Faster Than Pre-Pandemic

The first thing you should know is that, in most markets, things have slowed down a little bit. While you may remember how quickly homes sold a few years ago, that’s not what you should expect today.

Now that inventory has grown, according to Realtor.com, homes are taking a bit longer to sell in today’s market (see graph below):

But before you get hung up on the ten-day difference compared to the past few years, Realtor.com will help put this into perspective:

“In April, the typical home spent 50 days on the market . . . This marks the 13th straight month of homes taking longer to sell on a year-over-year basis. Still, homes are moving more quickly than they did before the pandemic . . .”

By this comparison, if your house does take a little more time to sell this year, it’s not really a concern. It’s actually still faster than the norm. Plus, it gives you a bit more time to find your next home, which is welcome relief when you’re trying to move, too.

Just remember, some homes sell in less time than this. Some take even longer. So, what’s the real difference? Why do some homes attract eager buyers almost instantly, while others sit and struggle?

It comes down to having the right agent and strategy. Here are a few tips you need to know.

1. Price It Right

One of the biggest reasons homes sit on the market is overpricing. Many sellers want to shoot for a higher price, thinking they can lower it later – but that backfires by turning buyers away.

What to do: Work with an agent to make sure your house is priced right. They’ll analyze recent comparable sales (what other homes have sold for recently in your area), so you know you’re pricing appropriately for today’s market and what buyers are willing to pay. As Chen Zhao, Economic Research Lead at Redfin, explains:

“My advice to sellers is to price your home fairly for the shifting market; you may need to price lower than your initial instinct to sell quickly and avoid giving concessions.”

2. Focus on the First Impression

A messy yard or a house that needs paint? It’ll turn buyers off. Since buyers decide within seconds whether they like a home, a good first impression is key.

What to do: Outside, clean up your front yard, tidy up your landscaping, power wash walkways, and add fresh mulch. Inside, declutter and depersonalize. And consider minor touch-ups like repainting in a neutral tone. Your agent will offer advice on what to tackle.

3. Strong Marketing & High-Quality Listing Photos

If your listing or your photos don’t look professional, you could have trouble drawing in buyers who think you’re trying to cut corners.

What to do: Instead, lean on your agent’s skills, expertise, and resources. They’ll help you make sure you have:

High-resolution listing photos showing the home in its best light.

Detailed descriptions that highlight differentiating features of your house.

Your listing on multiple platforms, including major real estate sites and social media.

4. The Location of the Home

You may have heard the phrase “location, location, location” when it comes to real estate. And there’s definitely some truth to that. Homes in highly sought-after neighborhoods tend to sell faster.

What to do: While you can’t change where your house is located, your agent can highlight the best features of your neighborhood or community in your listing. By showcasing what’s great about your area, they can help draw buyers into what life would look like in your house.

Bottom Line

Homes that sell quickly don’t necessarily have better features – they have better agents and a better strategy.

Are you thinking about selling? Connect with an agent to talk about how to get your home sold quickly and for top dollar.

With all the uncertainty in the economy, the stock market has been bouncing around more than usual. And if you’ve been watching your 401(k) or investments lately, chances are you’ve felt that pit in your stomach. One day it’s up. The next day, it’s not. And that may make you feel a little worried about your finances.

But here’s the thing you need to remember if you’re a homeowner. According to Investopedia:

“Traditionally, stocks have been far more volatile than real estate. That’s not to say that real estate prices aren’t ever volatile—the years around the 2007 to 2008 financial crisis are just one memorable example—but stocks are more prone to large value swings.”

While your stocks or 401(k) might see a lot of highs and lows, home values are much less volatile.

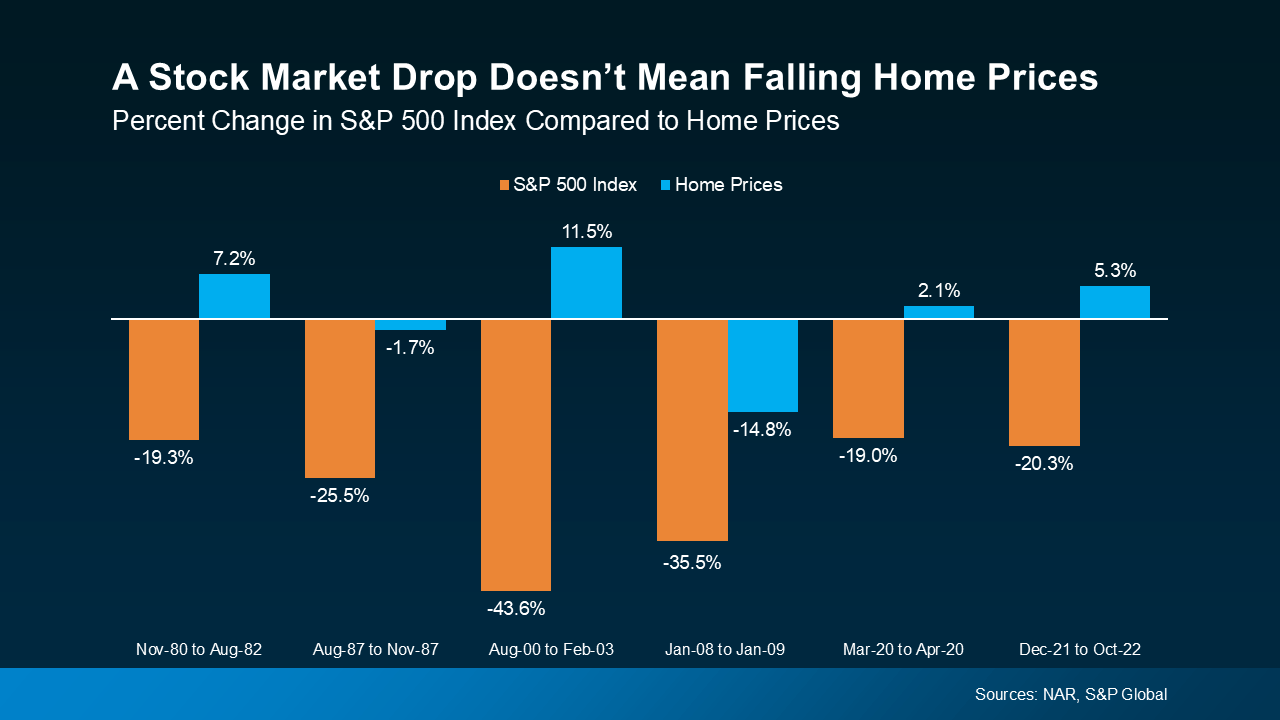

A Drop in the Stock Market Doesn’t Mean a Crash in Home Prices

Take a look at the graph below. It shows what happened to home prices (the blue bars) during past stock market swings (the orange bars):

Even when the stock market falls more substantially, home prices don’t always come down with it.

Big home price drops like 2008 are the exception, not the rule. But everyone remembers that one. That stock market crash was caused by loose lending practices, subprime mortgages, and an oversupply of homes – a scenario that doesn’t exist today. That’s what made it so different.

In many cases before and after that time, home values actually went up while the stock market went down, showing that real estate is generally much more stable.

This graph shows how stock prices go up and down (the orange line), sometimes by more than 30% in a year. In contrast, home prices (the blue line) change more slowly (see graph below):

Basically, stock values jump around a lot more than home prices do. You can be way up one day and way down the next. Real estate, on the other hand, isn’t usually something that experiences such dramatic swings.

That’s why real estate can feel more stable and less risky than the stock market.

So, if you’re worried after the recent ups and downs in your stock portfolio, rest assured, your home isn’t likely to experience the same volatility.

And that’s why homeownership is generally viewed as a preferred long-term investment. Even if things feel uncertain right now, homeowners win in the long run.

Bottom Line

A lot of people are feeling nervous about their finances right now. But there’s one reason for you to feel more secure – your investment in something that’s stood the test of time: real estate.

Even when the stock market falls more substantially, home prices don’t always come down with it.

Even when the stock market falls more substantially, home prices don’t always come down with it.