If you have additional loved ones coming to live with you but don’t have enough space, it may be time to consider a larger, multigenerational home.

Some key benefits of multigenerational living include a combined homebuying budget, shared caregiving duties, enhanced relationships, and more. These benefits might be why more people are choosing to live in multigenerational homes today.

Let’s connect so you can find a house that meets your changing needs and has plenty of space for you and your loved ones.

If you’re thinking of selling your house, it may be because you’ve heard prices are rising, listings are going fast, and sellers are getting multiple offers on their homes. But why are conditions so good for sellers today? And what can you expect when you move? To help answer both of those questions, let’s turn to the data.

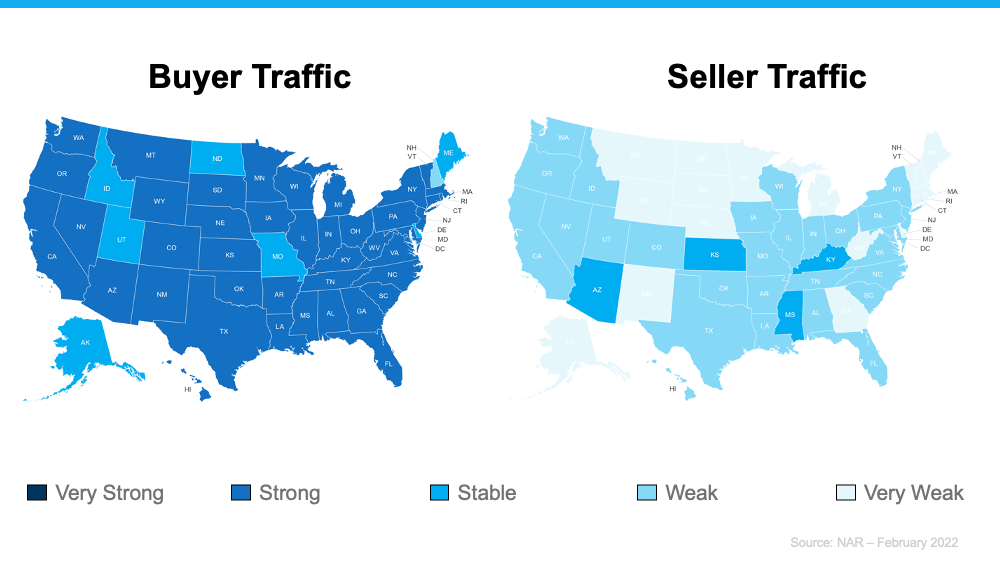

Today, there are far more buyers looking for homes than sellers listing their houses. Here are the maps of the latest buyer and seller traffic from the National Association of Realtors (NAR) to help paint the picture of what this looks like:

Notice how much darker the blues are on the left. This shows buyer traffic is strong today. In contrast, the much lighter blues on the right indicate weak or very weak seller traffic. In a nutshell, the demand for homes is significantly greater than what’s available to purchase.

What That Means for You

You have an incredible advantage when you sell your house under these conditions. Since buyer demand is so high at a time when seller traffic is so low, there’s a good chance buyers will be competing for your house.

According to NAR, in February, the average home sold got 4.8 offers. When buyers have to compete with one another like this, they’ll do everything they can to make their offer stand out. This could play to your favor and mean you’ll see things like waived contingencies, offers over asking price, earnest money deposits, and more. Selling when demand is high and supply is low sets you up for a big win.

If you’re also looking to buy a house, you may be tempted to focus more on just the seller traffic map and wonder if it means you’ll have trouble finding your next home. But remember this: perspective is key. As Danielle Hale, Chief Economist at realtor.com, says:

“The limited number of homes for sale is a lesson in perspective. This same stat that frustrates would-be homebuyers also means that today’s home sellers enjoy more limited competition than last year’s home sellers.”

If you look at the big picture, the opportunity you have as a seller today is unprecedented. Last year was a hot sellers’ market. This year, inventory is even lower, and that means an even bigger opportunity for you. Even though finding your next home in a market with low inventory can be challenging, is that concern worth passing on some of the best conditions sellers have ever seen?

As added peace of mind, remember real estate professionals have been juggling this imbalance of supply and demand for nearly two years, and they know how to help both buyers and sellers find success when they move. A skilled agent can help you capitalize on the great opportunity you have as a seller today and guide you through the buying process until you find the perfect place to call your next home.

Bottom Line

If you’re ready to move, you have an incredible opportunity in front of you today. Trust the experts. Let’s connect so you have expertise on your side that can help you win when you sell and when you buy.

There’s never been a truer statement regarding forecasting mortgage rates than the one offered last year by Mark Fleming, Chief Economist at First American:

“You know, the fallacy of economic forecasting is: Don’t ever try and forecast interest rates and or, more specifically, if you’re a real estate economist mortgage rates, because you will always invariably be wrong.”

Coming into this year, most experts projected mortgage rates would gradually increase and end 2022 in the high three-percent range. It’s only April, and rates have already blown past those numbers. Freddie Macannounced last week that the 30-year fixed-rate mortgage is already at 4.72%.

“Continuing on the recent trajectory, would have mortgage rates hitting 5% within a matter of weeks. . . .”

Just five days later, on April 5, the Mortgage News Dailyquoted a rate of 5.02%.

No one knows how swiftly mortgage rates will rise moving forward. However, at least to this point, they haven’t significantly impacted purchaser demand. Ali Wolf, Chief Economist at Zonda, explains:

“Mortgage rates jumped much quicker and much higher than even the most aggressive forecasts called for at the end of last year, and yet housing demand appears to be holding steady.”

Through February, home prices, the number of showings, and the number of homes receiving multiple offers all saw a substantial increase. However, much of the spike in mortgage rates occurred in March. We will not know the true impact of the increase in mortgage rates until the March housing numbers become available in early May.

Rick Sharga, EVP of Market Intelligence at ATTOM Data, recently put rising rates into context:

“Historically low mortgage rates and higher wages helped offset rising home prices over the past few years, but as home prices continue to soar and interest rates approach five percent on a 30-year fixed rate loan, more consumers are going to struggle to find a property they can comfortably afford.”

While no one knows exactly where rates are headed, experts do think they’ll continue to rise in the months ahead. In the meantime, if you’re looking to buy a home, know that rising rates do have an impact. As rates rise, it’ll cost you more when you purchase a house. If you’re ready to buy, it may make sense to do so sooner rather than later.

Bottom Line

Mark Fleming got it right. Forecasting mortgage rates is an impossible task. However, it’s probably safe to assume the days of attaining a 3% mortgage rate are over. The question is whether that will soon be true for 4% rates as well.

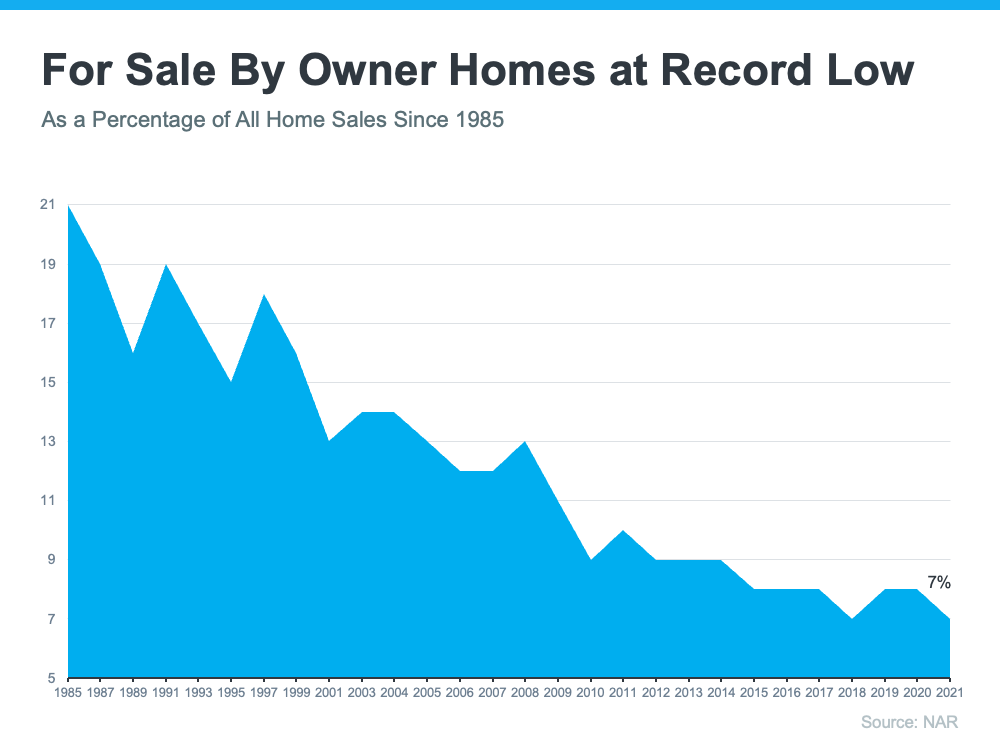

With today’s real estate market moving as fast as it is, working with a real estate professional is more essential than ever. They have the skills, experience, and expertise it takes to navigate the highly detailed and involved process of selling a home. That may be why the percentage of people who list their houses on their own, known as a FSBO or For Sale By Owner, has reached its lowest point since 1985 (see graph below):

Here are five reasons why selling with a real estate professional makes more sense, even in today’s hot market:

1. They Know What Buyers Want To See

Before you decide which projects and repairs to take on, connect with a real estate professional. They have first-hand experience with today’s buyers, what they expect, and what you need to do to make sure your house shows well.

If you don’t lean on their expertise, you may spend your time and money on something that isn’t essential. That’s because, in today’s low-inventory market, buyers are willing to take on more of the renovation work themselves. A survey from Freddie Mac finds that:

“. . . nearlytwo-in-five potential homebuyers would consider purchasing a home requiring renovations.”

A professional can help you decide what you need to tackle. It’s not canned advice you could find online – it’s recommendations specific to your house and your area.

2. They Help Maximize Your Buyer Pool

Today, the average home is getting 4.8 offers per sale according to recent data from the National Association of Realtors (NAR), and that competition is pushing prices up. While that’s promising for you as a seller, it’s important to understand your agent’s role in bringing buyers in.

Real estate professionals have an assortment of tools at their disposal, such as social media followers, agency resources, and the MLS to ensure your house is viewed by the most buyers. According to realtor.com:

“Only licensed real estate agents can list homes on the MLS, which is a one-stop online shop of sorts for getting a house seen by thousands of agents and home buyers. . . . This is certainly one of many good reasons why the majority of home sellers decide to employ the services of a listing agent rather than going it alone.”

Without access to these tools, your buyer pool is limited. And you want more buyers to view your house since buyer competition can drive your final sales price higher.

3. They Understand the Fine Print

Today, more disclosures and regulations are mandatory when selling a house. That means the number of legal documents you’ll need to juggle is growing. That’s why Investopediasays:

“One of the biggest risks of FSBO is not having the experience or expertise to navigate all of the legal and regulatory requirements that come with selling a home.”

A real estate professional knows exactly what needs to happen, what all the paperwork means, and how to work through it efficiently. They’ll help you review the documents and avoid any costly missteps that could occur if you try to handle them on your own.

4. They’re Trained Negotiators

If you sell without a professional, you’ll also be solely responsible for all the negotiations. That means you’ll have to coordinate with:

Thebuyer, who wants the best deal possible

Thebuyer’s agent, who will use their expertise to advocate for the buyer

Theinspection company, which works for the buyer and will almost always find concerns with the house

Theappraiser, who assesses the property’s value to protect the lender

Instead of going toe-to-toe with all these parties alone, lean on an expert. They’ll know what levers to pull, how to address everyone’s concerns, and when you may want to get a second opinion.

5. They Know How To Set the Right Price for Your House

If you sell your house on your own, you may over or undershoot your asking price. That could mean you’ll leave money on the table because you priced it too low or your house will sit on the market because you priced it too high. Pricing a house requires expertise. Investopediaexplains it like this:

“. . . There is no easy or universal way to determine market value for real estate.”

Real estate professionals know the ins and outs of how to price your house accurately and competitively. To do so, they compare your house to recently sold homes in your area and factor in the current condition of your house. These factors are key to making sure it’s priced to move quickly while still getting you the highest possible final sale price.

Bottom Line

There’s a lot that goes into selling your house. Instead of tackling it alone, let’s connect so you have an expert on your side throughout the entire process.

![What Is Multigenerational Housing? [INFOGRAPHIC] | Simplifying The Market](https://www.sellingthe608.com/wp-content/uploads/2022/04/20220415-MEM.png)