Sellers can benefit from more offers to pick from, higher home values, and a faster sales process. That might be why 73% of people believe it’s a good time to sell.

Sellers, don’t miss out on this unique opportunity. Let’s connect so you can take advantage of this hot sellers’ market.

If you’re a renter with a desire to become a homeowner, or a homeowner who’s decided your current house no longer fits your needs, you may be hoping that waiting a year might mean better market conditions to purchase a home.

To determine if you should buy now or wait, you need to ask yourself two simple questions:

What will home prices be like in 2022?

Where will mortgage rates be by the end of 2022?

Let’s shed some light on the answers to both of these questions.

What will home prices be like in 2022?

Three major housing industry entities project continued home price appreciation for 2022. Here are their forecasts:

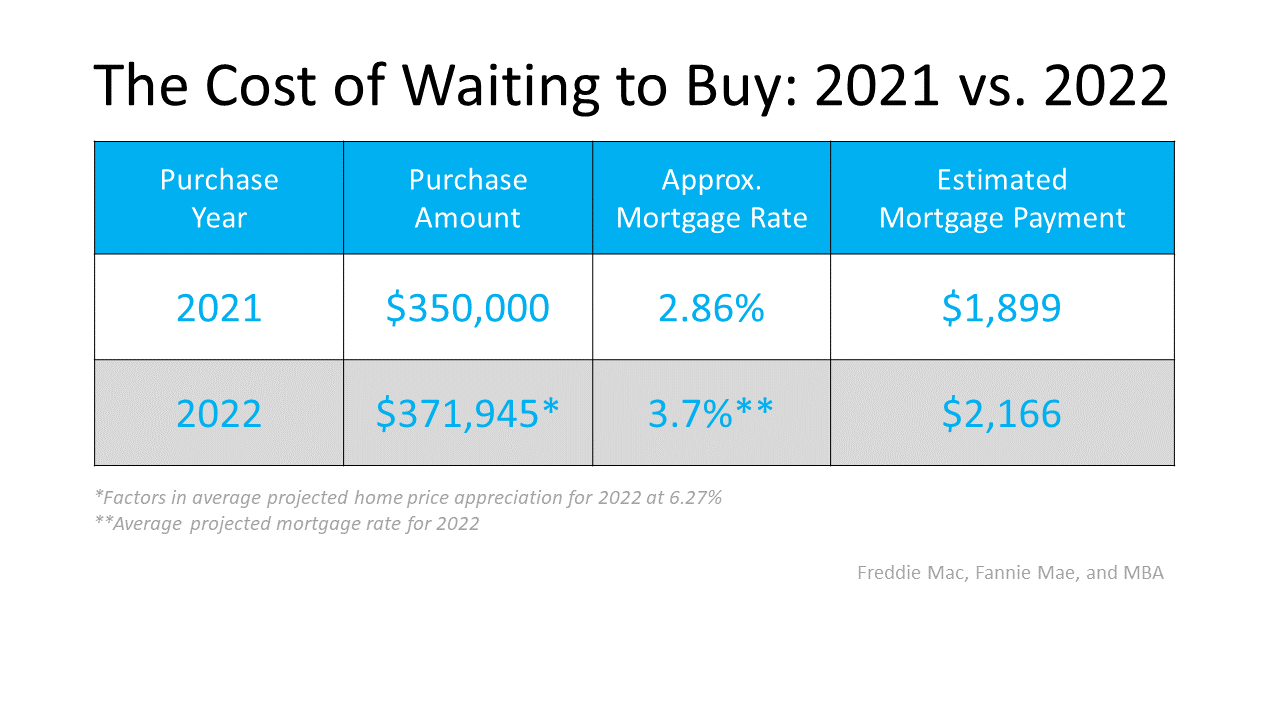

Using the average of the three projections (6.27%), a home that sells for $350,000 today would be valued at $371,945 by the end of next year. That means, if you delay, it could cost you more. As a prospective buyer, you could pay an additional $21,945 if you wait.

Where will mortgage rates be by the end of 2022?

Today, the 30-year fixed mortgage rate is hovering near historic lows. However, most experts believe rates will rise as the economy continues to recover. Here are the forecasts for the fourth quarter of 2022 by the three major entities mentioned above:

That averages out to 3.7% if you include all three forecasts, and it’s nearly a full percentage point higher than today’s rates. Any increase in mortgage rates will increase your cost.

What does it mean for you if both home values and mortgage rates rise?

You’ll pay more in mortgage payments each month if both variables increase. Let’s assume you purchase a $350,000 home this year with a 30-year fixed-rate loan at 2.86% after making a 10% down payment. According to the mortgage calculator from Smart Asset, your monthly mortgage payment (including principal and interest payments, and estimated home insurance, taxes in your area, and other fees) would be approximately $1,899.

That same home could cost $371,945 by the end of 2022, and the mortgage rate could be 3.7% (based on the industry forecasts mentioned above). Your monthly mortgage payment, after putting down 10%, would increase to $2,166.

The difference in your monthly mortgage payment would be $267. That’s $3,204 more per year and $96,120 over the life of the loan.

If you consider that purchasing now will also let you take advantage of the equity you’ll build up over the next calendar year, which is approximately $22,000 for a house with a similar value, then the total net worth increase you could gain from buying this year is over $118,000.

Bottom Line

When asking if you should buy a home, you probably think of the non-financial benefits of owning a home as a driving motivator. When asking when to buy, the financial benefits make it clear that doing so now is much more advantageous than waiting until next year.

There’s a common misconception that, as a homebuyer, you need to come up with 20% of the total sale price for your down payment. In fact, a recent survey by Lending Tree asks what is keeping consumers from purchasing a home. For over half of those surveyed, the ability to afford a down payment is the biggest hurdle.

That may be because those individuals assume a 20% down payment is necessary. While putting more money down if you’re able can benefit buyers, putting 20% down is not mandatory. As Freddie Mac puts it:

“The most damaging down payment myth—since it stops the homebuying process before it can start—is the belief that 20% is necessary.”

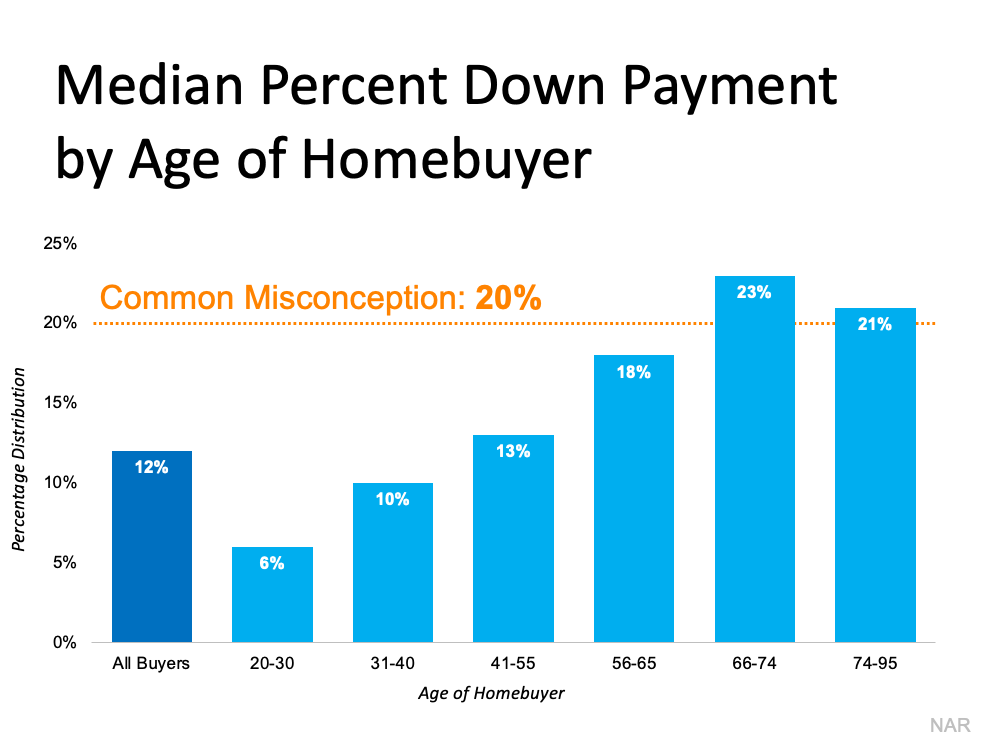

If saving that much money sounds overwhelming, you might be ready to give up on the dream of homeownership before you even begin – but you don’t have to. According to the Profile of Home Buyers and Sellers from the National Association of Realtors (NAR), the median down payment hasn’t been over 20% since 2005. It may sound surprising, but today’s average down payment is only 12%. That number is even lower for first-time homebuyers, whose average down payment is only 7%.

Based on the Home Buyers and Sellers Generational Trends Report from NAR, the graph below shows an even closer look at the down payment percentage various age groups pay:As the graph shows, the only groups who put 20% or more down on average are older homebuyers who likely can use the sale of an existing home to fuel a larger down payment on their next home.

What does this mean for you?

If you’re a prospective homebuyer, it’s important to know you don’t have to put the full 20% down. And while saving for any down payment amount may feel like a challenge, keep in mind there are programs for qualified buyers that allow them to purchase a home with a down payment as low as 3.5%. There are also options like VA loans and USDA loans with no down payment requirements for qualified applicants.

To understand your options, you do need to do your homework. If you’re interested in learning more about down payment assistance programs, information is available through sites like downpaymentresource.com. Be sure to also work with a real estate advisor from the start to learn what you may qualify for in the homebuying process.

Bottom Line

Don’t let the myth of the 20% down payment halt your homebuying process before it begins. If you want to purchase a home this year, let’s connect to start the conversation and explore your options.

A lot has changed over the past year. For many people, the rise in remote work influenced what they’re looking for in a home and created a greater appetite for a dedicated home office. Some professionals took advantage of the situation and purchased a bigger home. Other people thought working from home would be temporary, so they chose to get creative and make the space they already had work for them. But recent headlines indicate working from home isn’t a passing fad.

If you’re still longing for a dedicated home office, now may be the time to find the home that addresses your evolving needs. More and more companies are delaying their plans to return to the office – others are deciding to remain fully remote permanently. According to economists from Goldman Sachs in a recent article from CNN:

“Job ads increasingly offer remote work and surveys indicate that both workers and employers expect work from home to remain much more common than before the pandemic.”

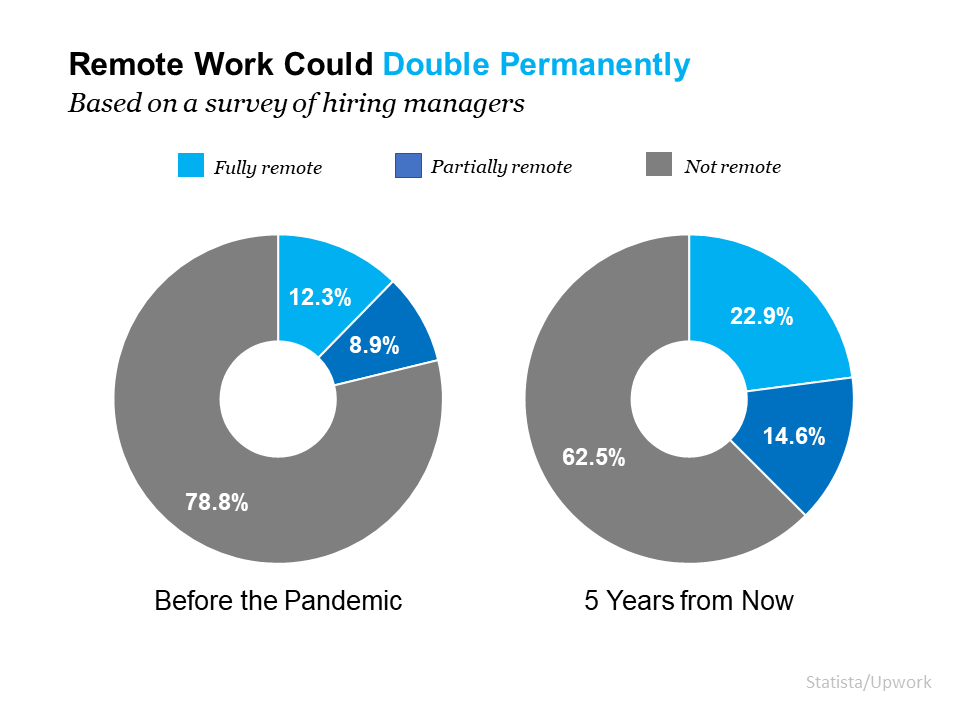

Other experts agree. A survey conducted by Upwork of 1,000 hiring managers found that due to the pandemic, companies were planning more remote work now and in the years to come. Upwork elaborates:

“The number of remote workers in the next five years is expected to be nearly double what it was before COVID-19: By 2025, 36.2 million Americans will be remote, an increase of 16.8 million people from pre-pandemic rates.”

The charts below break down their findings and compare pre- and post-pandemic percentages.

How Does This Impact Homeowners?

If you own your home, it’s important to realize that continued remote work may give you opportunities you didn’t realize you had. Since you don’t need to be tied to a specific area for your job, you have more flexibility when it comes to where you can live.

If you’re one of the nearly 23% of workers who will remain 100% remote:

You have the option to move to a lower cost-of-living area or to the location of your dreams. If you search for a home in a more affordable area, you’ll be able to get more home for your money, freeing up more options for your dedicated office space and additional breathing room.

You could also move to a location where you’ve always wanted to live – somewhere near the beach, the mountains, or simply a market that features the kind of weather and community amenities you’re looking for. Without your job tying you to a specific location, you’re bound to find your ideal spot.

If you’re one of the almost 15% of individuals who will have a partially remote or hybrid schedule:

Relocating within your local area to a home that’s further away from your office could be a great choice. Since you won’t be going in to work every day, a slightly longer commute from a more suburban or rural neighborhood may be a worthy trade-off for a home with more features, space, or comforts.

Bottom Line

If ongoing remote work is changing what you need in a home, let’s connect to find one that delivers on your new wish list.

![It’s Still a Sellers’ Market [INFOGRAPHIC] | Simplifying The Market](https://www.sellingthe608.com/wp-content/uploads/2021/09/20210924-MEM.png)