Why Home Sales Bounce Back After Presidential Elections

With the 2024 Presidential election fast approaching, you might be wondering what impact, if any, it’s having on the housing market. Let’s break it down.

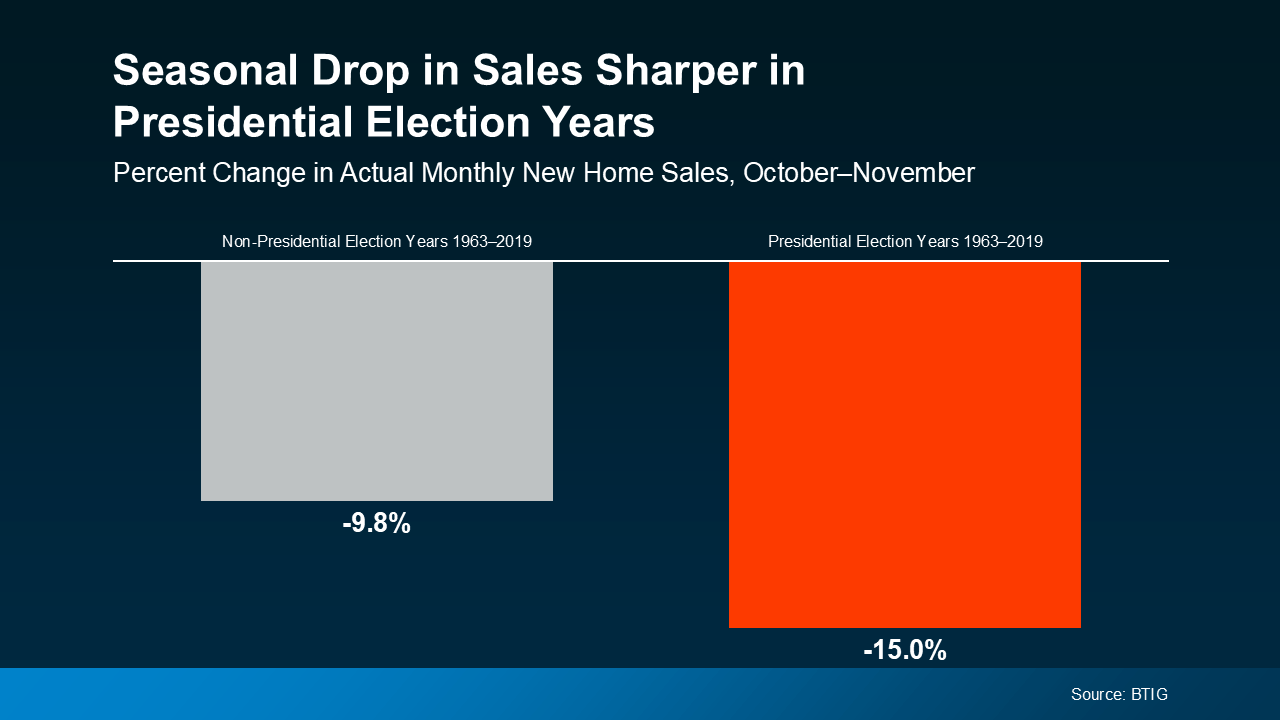

Election Years Bring a Temporary Slowdown

In any given year, home sales slow down slightly in the fall. It’s a typical, seasonal trend. However, according to data from BTIG, in election years there’s usually a slightly larger dip in home sales in the month leading up to Election Day (see graph below):

Why? Uncertainty. Many consumers hold off on making major decisions or purchases while they wait to see how the election will play out. It’s a pattern that’s shown up time and time again, and it’s particularly apparent for buyers and sellers in the housing market.

Why? Uncertainty. Many consumers hold off on making major decisions or purchases while they wait to see how the election will play out. It’s a pattern that’s shown up time and time again, and it’s particularly apparent for buyers and sellers in the housing market.

This year is no different. A recent survey from Redfin found that 23% of potential first-time homebuyers said they’re waiting until after the election to buy. That’s nearly a quarter of first-time buyers hitting the pause button, likely due to the same feelings of uncertainty.

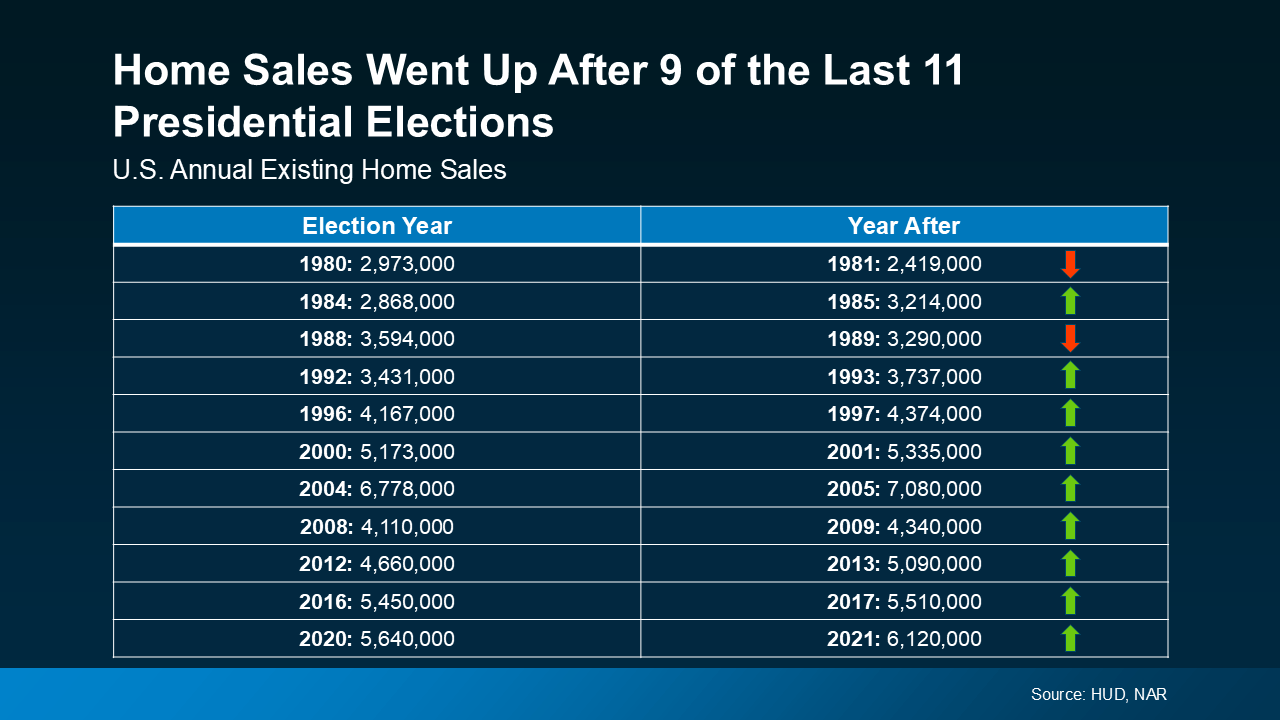

Home Sales Bounce Back After the Election

The good news is these delayed sales aren’t lost forever—they’re just postponed. History shows sales tend to rebound after the election is over. In fact, home sales have actually increased 82% of the time in the year after the election (see chart below):

That’s because once the election dust settles, buyers and sellers have a sense of what’s ahead and generally feel more confident moving forward with their decisions. And that leads to a boost in home sales.

That’s because once the election dust settles, buyers and sellers have a sense of what’s ahead and generally feel more confident moving forward with their decisions. And that leads to a boost in home sales.

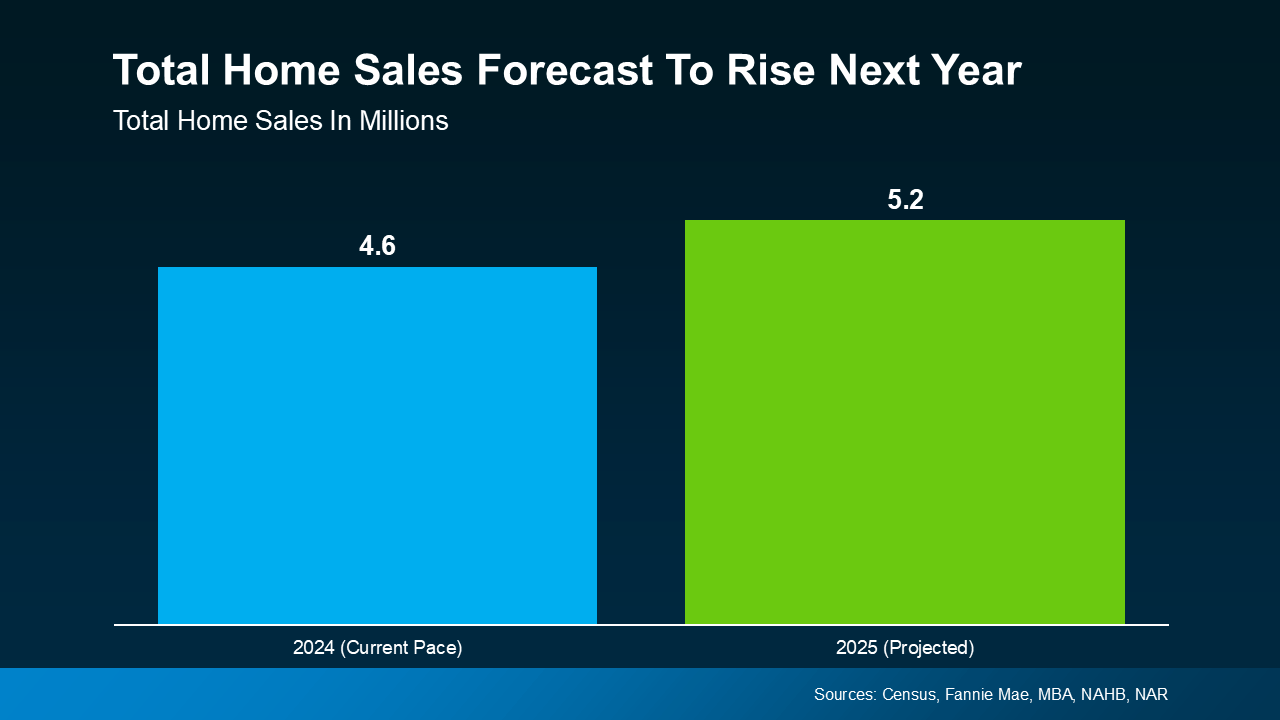

What To Expect in 2025

If history is any indicator, that means more homes will sell next year. And based on the latest forecasts, that’s exactly what you should expect. As the graph below shows, the housing market is on pace to sell a total of 4.6 million homes this year, and projections are for 5.2 million total sales next year (see graph below):

And that aligns with the typical pattern of post-election rebounds.

And that aligns with the typical pattern of post-election rebounds.

So, while it might feel like the market is slowing down right now, it’s more of a temporary dip rather than a long-term trend. As has been the case before, once the election uncertainty passes, buyers and sellers will return to the market.

Bottom Line

It’s important to remember that while election years often bring a short-term slowdown in the housing market, the pause is usually temporary. Those sales are not lost. Data shows home sales typically increase the year after a Presidential election, and current forecasts indicate 2025 will be no different. If you’re waiting for a clearer picture before making a move, just know that the market is expected to pick up speed in the months ahead.