If you have questions about what to expect for the rest of the year, connect with a local agent to have a conversation about what it means for you and your plans.

When you decide to buy your first home, you may come across a number of terms and conditions you’re not familiar with. While you may have a general idea of what an inspection is, maybe you’re not sure why you need one or how it’s different from an appraisal. To keep it simple, here’s an explainer of each one and what they mean for you as a homebuyer.

Home Inspection

Once you’re under contract on a home you’d like to buy, getting an inspection is a key part of the process. An inspection gives you a clear idea of the safety and overall condition of the home – which is important for such a big transaction. As a recent Realtor.com article explains:

“A home inspection is something that protects your financial interest in what will likely be the largest purchase you make in your life—one in which you need as much information as possible.”

If anything is questionable in the inspection process – like the age of the roof, the state of the HVAC system, or just about anything else – you have the option to discuss and negotiate any potential issues or repairs with the seller before the transaction is final. And don’t worry – you don’t have to go through that process alone. Your real estate agent will be your advocate and negotiate with the seller for you.

Home Appraisal

While the inspection tells you about the current state of the house, an appraisal gives you its value. Bankrate explains:

“When buying or selling a home, an appraisal verifies that the sale price of the home is in line with fair market value. This ensures the homebuyer doesn’t pay more than the home is worth, and the mortgage lender doesn’t lend more than it is worth.”

Regardless of what you’re willing to pay for a house, if you’ll be using a mortgage to fund your purchase, the appraisal protects you from overpaying and the bank from lending you more than the home is worth.

And if there’s ever any confusion or discrepancy between the appraisal and the agreed-upon price in your contract, your trusted real estate professional will help you navigate any additional negotiations to try to close the gap.

Bottom Line

The inspection and the appraisal are different but equally important steps when buying a home – and you don’t need to manage them by yourself. Connect with an agent today so you have expert guidance from start to finish.

Should you buy a home now or should you wait? That’s a big question on many people’s minds today. And while what timing is right for you will depend on a lot of other personal factors, here’s something you may not have considered.

If you’re able to buy at today’s rates and prices, it may be better to focus on time in the market, rather than timing the market.

The Downside of Trying To Time the Market

Trying to time the market isn’t a good strategy because things can change. Here’s an example. For the better part of this year, projections have said mortgage rates will come down. And while experts agree that’s still what’s ahead, shifts in various market and economic factors have pushed back the timing of when that’ll happen. Here’s how that’s impacted homebuyers who’ve been sitting on the sidelines. As U.S. News says:

“Those who put off buying a home during the past few years as they were holding out for lower mortgage rates have been left out of the market . . . mortgage rates have stayed higher for longer than previously expected, keeping monthly housing payments elevated. In other words, affordability didn’t improve for those who chose to wait.”

This is why timing the market may not pay off if you’re ready and able to buy now.

The Proof Is in the Pudding: How Homeowners Benefit from Rising Home Prices

Delaying your plans also means missing out on the equity you’d gain if you went ahead with your purchase today. And the potential equity gains that are at stake may surprise you.

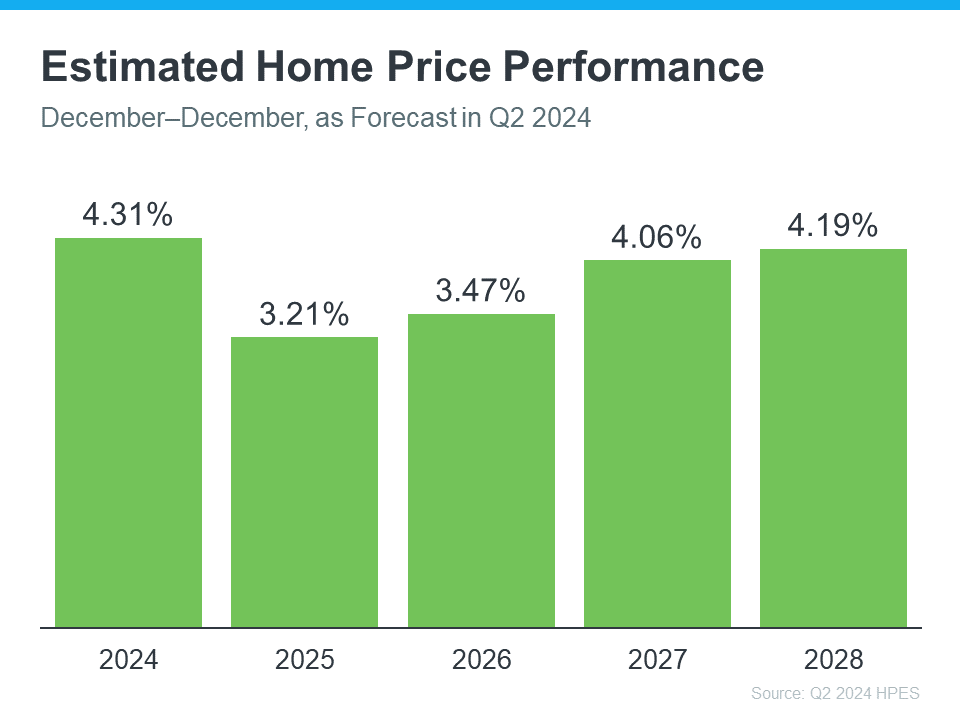

Each quarter, Fannie Mae releases the Home Price Expectations Survey. It asks over one hundred economists, real estate experts, and investment and market strategists what they forecast for home prices over the next five years. In the latest release, experts are projecting home prices will continue to rise through at least 2028 (see the graph below):

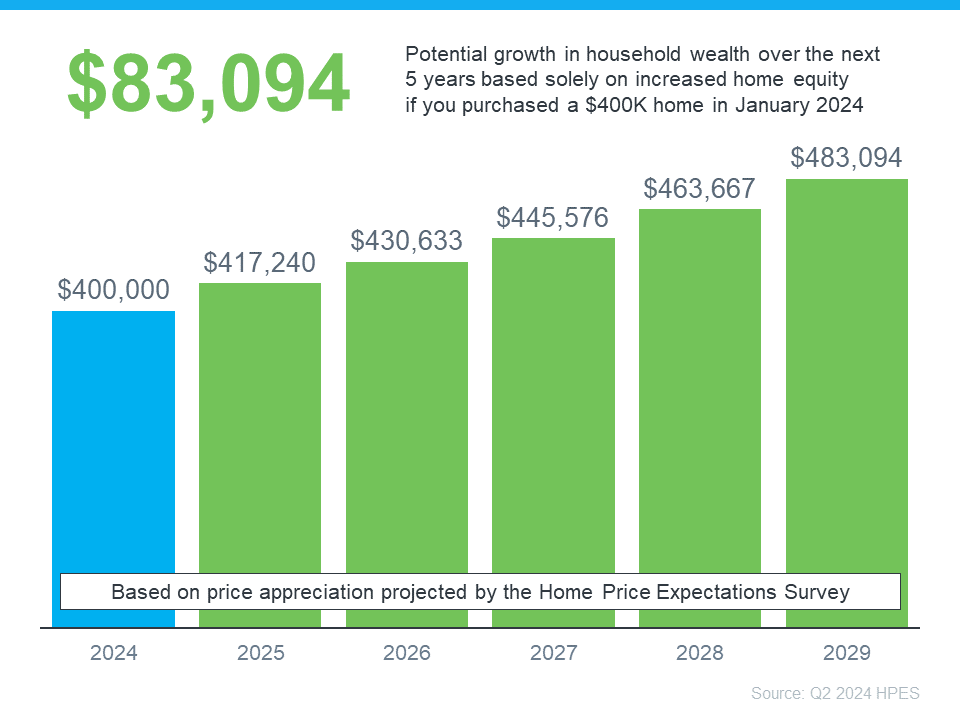

To give these numbers context, let’s take a look at a breakdown of what you stand to gain once you buy. The graph below uses a typical home’s value to show how a home could appreciate over the next few years using those HPES projections:

In this example, let’s say you went ahead and bought a $400,000 home at the beginning of this year. Based on the expert forecasts from the HPES, you could gain more than $83,000 in household wealth over the next five years. That’s not a small number.

This data helps paint the picture of why time in the market really matters.

The Advice You Need To Hear If You’re Ready and Able To Buy Now

Prices are expected to continue climbing, just at a more moderate pace. And while a moderate rise in prices may not be fun for you now, once you own a home, that growth will be a huge perk. That’s the time in the market piece.

Sure, you could try timing the market, but the equity you’ll be missing out on in the meantime is something to seriously consider. If you’re ready and able to buy now, you have to decide: is it really worth waiting?

Rather than focusing on timing the market. It’s better to have time in the market.

As U.S. News Real Estate sums up:

“There’s never a one-size-fits-all answer to whether now is the right time to buy a home. . . . There’s also no way to predict precisely what the market will do in the near future . . . Perfectly timing the market shouldn’t be the goal. This decision should be determined by your personal needs, financial means and the time you have to find the right home.”

Bottom Line

If you’re debating whether to buy now or wait, remember it’s time in the market, not timing the market. And if you want to get the ball rolling and set yourself up for those big equity gains, connect with an agent to make it happen.

You want your house to sell fast. And you may be wondering how long the whole process is going to take. One way to get your answer? Work with a local real estate agent.

They have the expertise to tell you how quickly homes are selling in your area and what’s impacting timelines for other sellers. That way you have realistic expectations and can work together to come up with a plan that’s based on today’s market.

Here’s a high-level overview of just one of the factors a great agent will walk you through – the supply of homes for sale and how that impacts your process.

The Growing Supply of Homes for Sale

Over the past few months, the number of homes for sale has increased. This is good news when you move because it means you’ll have more options as you search for your next home. But it also means buyers have more to choose from, so if your house doesn’t stand out – it may take a bit longer to sell.

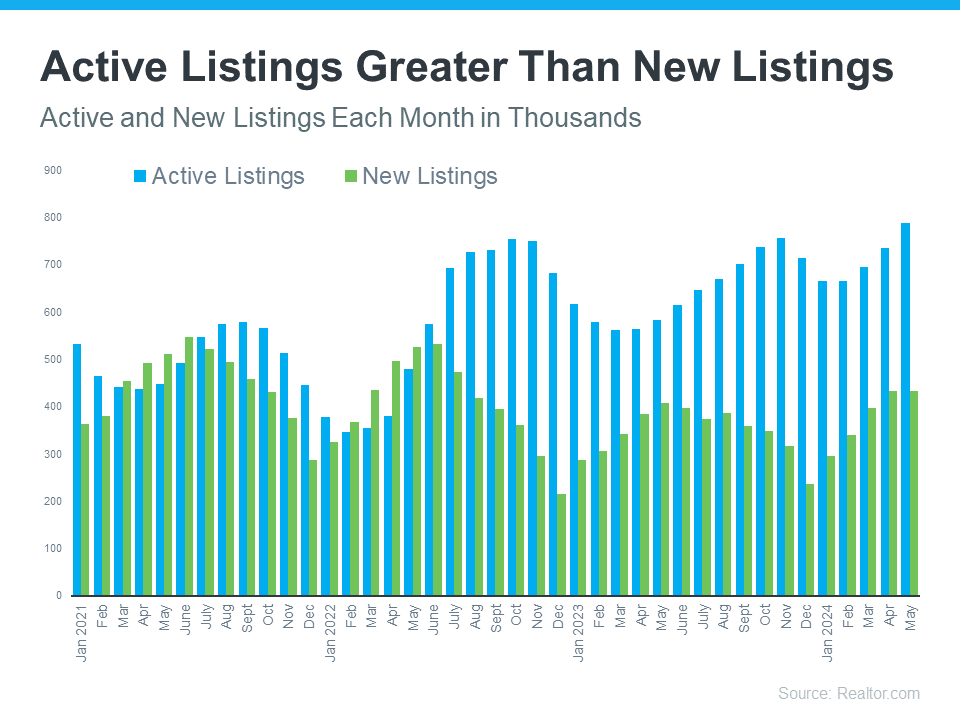

Available inventory is made up of new listings (homes that were just put up for sale) and active listings (homes that were already on the market but haven’t sold yet). And if you look at data from Realtor.com you can see a good portion of the recent growth is from active listings that are sticking around (see the blue bars in the graph below):

How It’s Impacting Listings Today

Think of the homes on the market like loaves of bread for sale in a bakery. When a fresh batch of bread is put out, everyone wants the newest and hottest one. But if a loaf sits there too long, it starts to get stale, and fewer people want to buy it.

The same goes for homes. New listings are the freshest and most sought-after. But if a home isn’t priced correctly, doesn’t show well, or it doesn’t have an effective sales or marketing strategy behind it, it can sit on the market and become less appealing to buyers over time.

An Agent Will Help Your House Stand Out and Sell Quickly

Timing is important to you. You want to get this done, fast. By leaning on a pro, they’ll make sure your listing is fresh and doesn’t stick around long enough to go stale. As the National Association of Realtors (NAR) explains:

“Home sellers without an agent are nearly twice as likely to say they didn’t accept an offer for at least three months; 53% of sellers who used an agent say they accepted an offer within a month of listing their home.”

Your agent will factor the recent inventory growth into their plan and create a customized selling strategy for your house. The supply of homes for sale can vary a lot by area. So they’ll do things like share their valuable insights into what’s happening with supply in your market, help you price your home correctly, and create a marketing plan that gets your home noticed.

Don’t let your listing get stale—reach out to a real estate agent today to make sure your listing is fresh and appeals to buyers from the start. It makes a big difference.

Bottom Line

If you want your house to sell fast, you need to work with a pro. Connect with a local agent, so you’ve got someone who understands the current market trends and how to build a strategy around those factors, so your house is set up to sell quickly.