Thinking about selling your house? Here are a few reasons why you may want to do it this season.

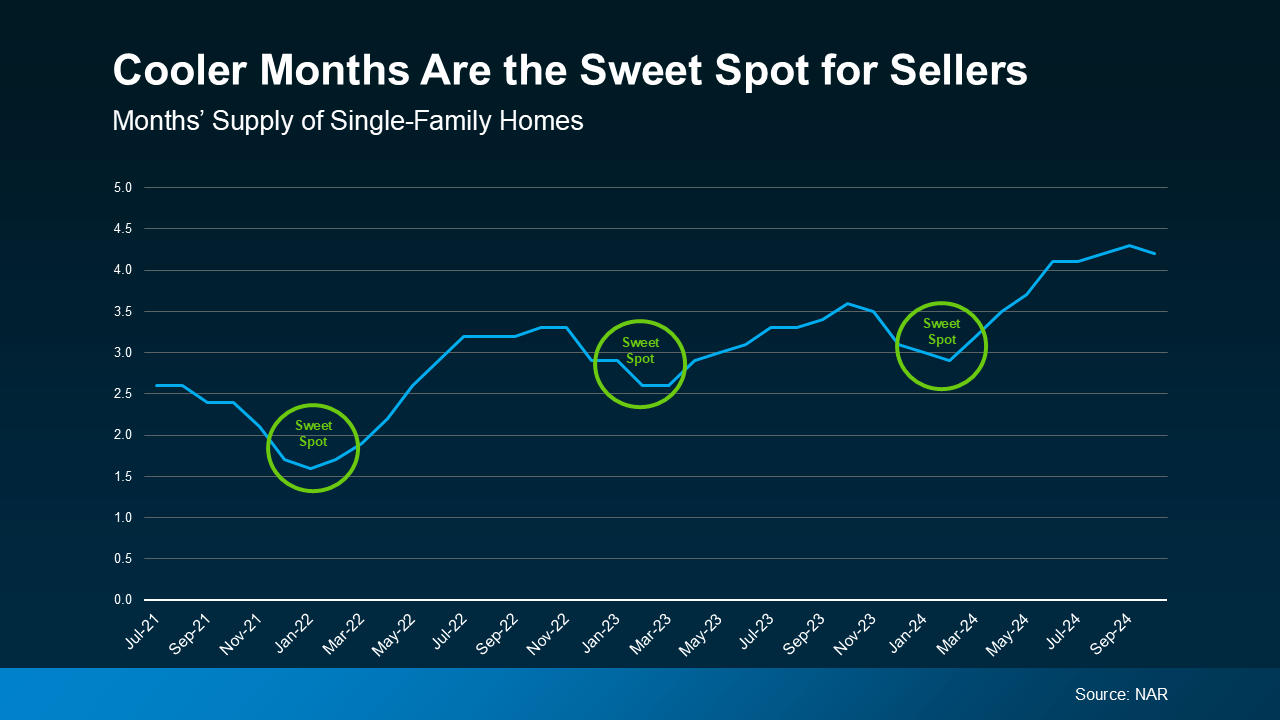

Buyers looking right now are serious about moving and the number of homes for sale is typically lower this time of year – helping your house stand out.

While inventory is higher this year than it’s been in the last few winters, you’ll still be in this year’s sweet spot.

Today’s mortgage rates and home prices may have you second-guessing whether it’s still a good idea to buy a home right now. While market factors are definitely important, there’s also a bigger picture to consider: the long-term benefits of homeownership.

Think of it this way. If you know people who bought a home 5, 10, or even 30 years ago, you’re probably going to have a hard time finding someone who regrets their decision. That’s because over time, home values usually grow – and that means a homeowner’s net worth does too. Here’s a look at how that can really add up over the years.

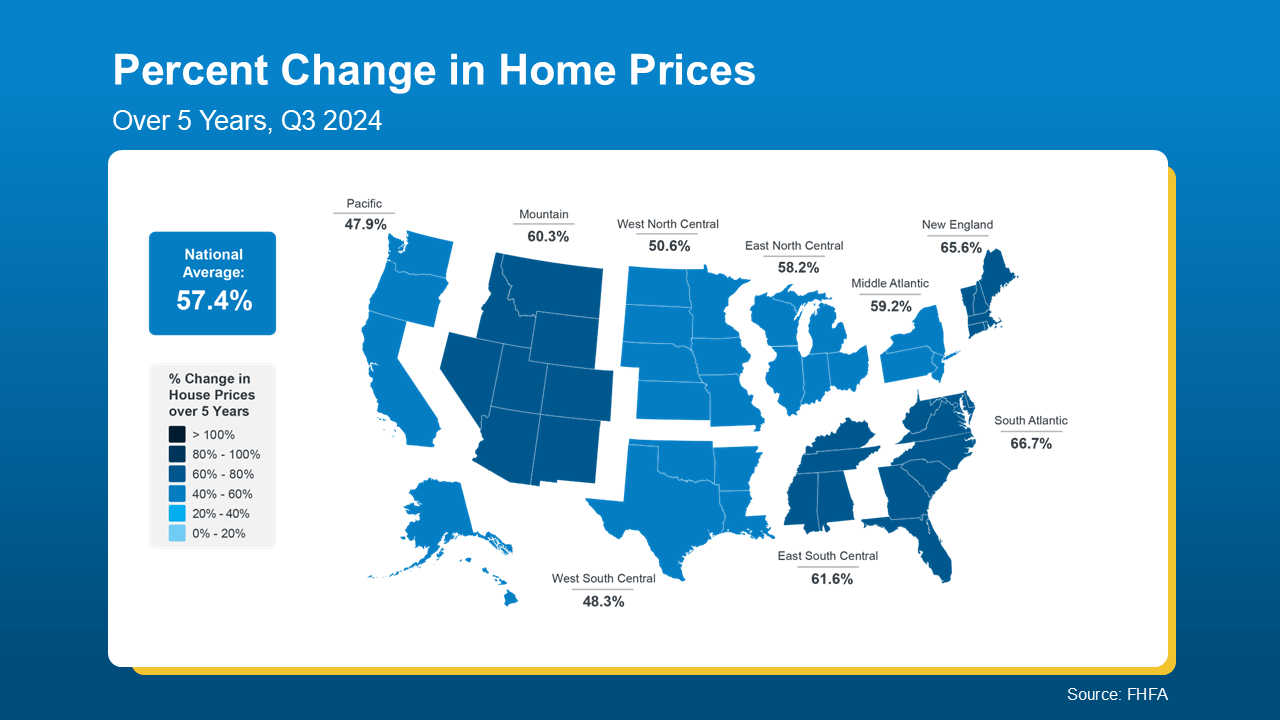

Home Price Growth over Time

The map below uses data from the Federal Housing Finance Agency (FHFA) to show how much prices have grown over the last five years. Since home prices vary by area, the map is broken out regionally to really showcase larger market trends:

You can see that nationally, home prices increased by over 57% in just five years.

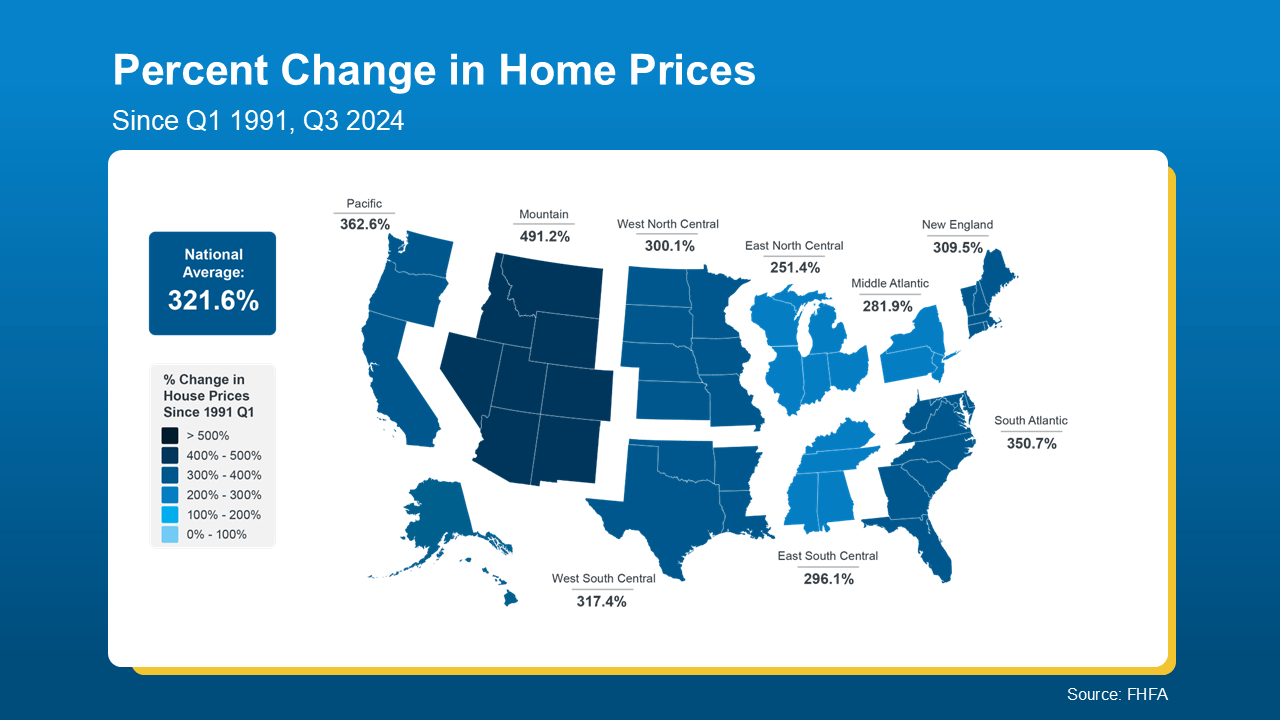

Some regions are slightly above or below that average, but overall, home prices saw a big uptick in a short time. And if you zoom out even more, the benefit of homeownership — and the drastic gains homeowners made over the years — become even more clear (see map below):

The second map shows that, over a roughly 30-year span, home prices appreciated by an average of more than 320% nationally.

So the typical homeowner who bought a house about 30 years ago saw their home triple in value during that time. And that’s a major reason so many homeowners who bought their homes years ago are still happy with their decision today.

Bottom Line

There’s no denying today’s market is complex. But if you’re ready and able to buy right now, get in touch with an agent to talk through how you can still make your move happen. That way you can take advantage of the long-term advantages that come with homeownership, like your ability to build wealth as your home value rises.

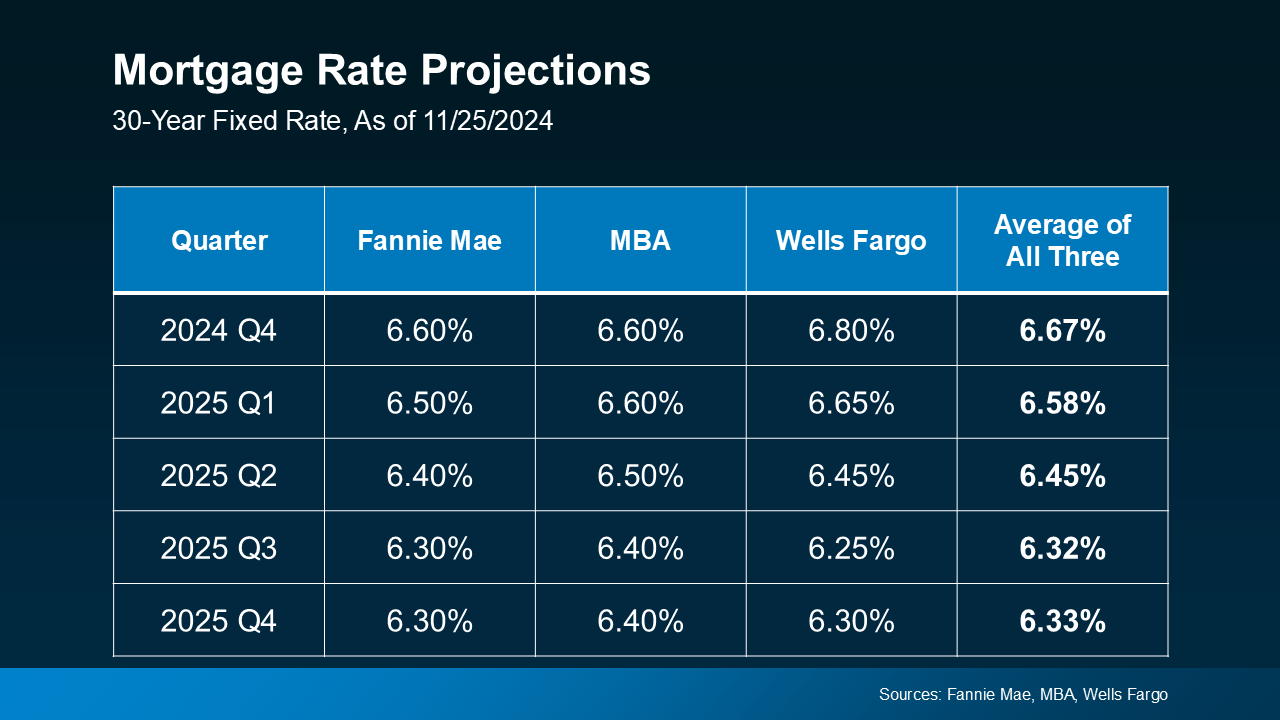

One of the biggest questions on everyone’s minds right now is: when will mortgage rates come down? After several years of rising rates and a lot of bouncing around in 2024, we’re all eager for some relief.

While no one can project where rates will go with complete accuracy or the exact timing, experts offer some insight into what we might see going into next year. Here’s what the latest forecasts show.

Mortgage Rates Are Expected To Ease and Stabilize in 2025

After a lot of volatility and uncertainty, the most updated forecasts suggest rates will start to stabilize over the next year, and should ease a bit compared to where they are right now (see graph below):

As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“While mortgage rates remain elevated, they are expected to stabilize.”

Key Factors That’ll Impact the Future of Mortgage Rates

It’s important to note that the timing and the pace of what happens with mortgage rates is one of the most challenging forecasts to make in the housing market. That’s because these forecasts hinge on a few key factors all lining up. So don’t be fooled, because while rates are expected to come down slightly, they’re going to be a moving target. And the ups and downs of ongoing economic drivers will likely stick around. Here’s a look at just a few of the things that’ll influence where they go from here:

Inflation: If inflation cools, rates could dip a bit more. On the flip side, if inflation rises or remains stubbornly high, rates may stay elevated longer.

Unemployment Rate: The unemployment rate also plays a significant role in upcoming decisions by the Federal Reserve (the Fed). And while the Fed doesn’t set mortgage rates, their actions do reflect what’s happening in the greater economy, which can have an impact.

Government Policies: With the next administration set to take office in January, fiscal and monetary policies could also affect how financial markets respond and where rates go from here.

Remember, these forecasts are based on the best information available right now. As new economic data comes out, experts will revise their projections accordingly. So, don’t try to time the market based on these forecasts alone.

Instead, the best thing you can do is focus on what you can control right now. Work on improving your credit score, put away any extra cash for your down payment, and automate your savings. All of these things will help you reach your homeownership goals even faster.

And be sure to connect with a trusted agent and a lender, so you always have the latest updates – and an expert opinion on what that means for your move.

Bottom Line

If you’re planning to move and want to stay informed about where mortgage rates are heading, connect with a trusted agent and lender.

A lot of people assume spring is the ideal time to sell a house. And sure, buyer demand usually picks up at that time of year. But here’s the catch: so does your competition because a lot of people put their homes on the market at the same time.

So, what’s the real advantage of selling your house before spring? It’ll stand out.

Historically, the number of homes for sale tends to drop during the cooler months – and that means buyers have fewer options to choose from.

You can see how that trend played out over the past few years in this data from the National Association of Realtors (NAR). Each time, the supply of homes for sale dipped during these cooler months. And then, after each winter lull, inventory started to climb as more sellers jumped into the market closer to spring (see graph below):

Here’s why knowing how this trend works gives you an edge. While inventory is higher this year than it‘s been in the last few winters, if you work with an agent to list now, it’ll still be in this year’s sweet spot. So, while other sellers are taking their homes off the market, you can sell before the spring wave of new listings hits, and your house will have a better chance of standing out.

Why wait until spring when you can get ahead of the curve now?

Fewer Listings Also Means More Eyes on Your Home

Another big perk of selling in the winter? The buyers who are looking right now are serious about making a move.

During this season, the window-shopper crowd tends to stay busy with other things, like holiday celebrations, and avoids looking for homes when the weather’s cooler. So, the buyers out looking aren’t casually browsing—they’re motivated, whether it’s because of a job relocation, a lease ending, or some other time-sensitive reason. And those are the types of buyers you want to work with. Investopedia explains:

“. . . if your house is up for sale in the winter and someone is looking at it, chances are that person is serious and ready to buy.”

Bottom Line

With less competition and serious buyers on the hunt, you’ll be in a great position to sell your house this winter. Connect with a local agent to get the process started.

The second map shows that, over a roughly 30-year span, home prices appreciated by an average of more than 320% nationally.

The second map shows that, over a roughly 30-year span, home prices appreciated by an average of more than 320% nationally.