There’s no denying affordability is tough right now. But that doesn’t mean you have to put your plans to buy a home on the back burner.

If you’re willing to roll up your sleeves (or hire someone who will), buying a house that needs some work could open the door to homeownership. Here’s everything you need to know so you can decide if this is the right move for you.

What’s a Fixer-Upper?

A fixer-upper is a home that’s livable but requires some renovations. Think cosmetic updates like wallpaper removal and new flooring or more extensive repairs like replacing a roof or updating plumbing.

While fixer-uppers need a little TLC, here’s why they may be worth considering, especially right now:

They Usually Have a Lower Price Point. Because of the repairs involved, these homes are usually less expensive up front than move-in-ready options. According to a survey from StorageCafe, fixer-uppers come with price tags that are about 29% lower, making them a solid choice if you’re having trouble finding anything in your budget.

Less Competition. When you’re ready to make an offer, you’re less likely to deal with competition from other buyers who are focused on move-in-ready homes.

Build Equity Faster. From choosing how to redo the floors to picking which cabinets you want in the kitchen, a fixer-upper allows you to design a space that fits your needs and style. And with smart renovations, you can increase your home’s value faster and potentially see a big return on your investment.

As The Mortgage Reports notes:

“If you’re a house hunter who’s not afraid of sweat equity, buying a fixer-upper could be your ticket to homeownership. Doing so could lead to big savings, even in some of the nation’s largest and most popular housing markets. Plus, adding the right features could help your investment.”

What To Know About Buying a Fixer-Upper

The possibilities that come with a fixer-upper are exciting, but there are a few things to think about first.

Do You Have a Gameplan? Consider if you have the time, skills, or budget to tackle renovations. Be honest about what you can handle yourself, what you’ll need to hire out, and if a fixer-upper is truly a good fit for your lifestyle. Remember, you’ll likely be living in a construction zone at least for a little while.

Prioritize the Repairs and Upgrades: Don’t stress yourself out thinking you’ve got to do all the work up front. Space out renovations over time in a way that makes sense for your budget and what’s most important to tackle first.

Location Matters: You want the money you’re spending to fix up a house to be worth the investment. So, make sure the home is in an area with increasing home values and amenities locals love, like parks and restaurants.

Get a Home Inspection: Hiring an inspector to do a thorough inspection before you buy is a must. What they find will help you understand what needs to be updated, renovation costs, and if it’s a project you want to take on.

Budget for Surprises: Renovations rarely go as planned. So, be sure to set aside extra money to cover things like extended repair timelines, an increase in the cost of materials, or other unknowns that may come up.

Talk to a Lender About Financing Options: There are some renovation mortgages designed for homes that need a little work. But they may have requirements like spending and timeline limits, so talk to a trusted lender to understand the fine print.

Bottom Line

Fixer-uppers aren’t for everyone, but if you’re open to doing a bit of work, they can be a great way to overcome today’s affordability hurdles and find something in your budget. With the right mindset and careful planning, you could turn a less-than-perfect house into the perfect home for you.

So, if you’re considering taking the plunge, talk to a real estate agent about finding a fixer-upper that fits your budget and goals.

The past few years have been challenging for homebuyers, especially with higher home prices and mortgage rates. And if you’re trying to buy a home, it’s easy to worry you won’t be able to find something in your budget.

But here’s what you need to know. The number of homes for sale has grown a whole lot lately and that’s true for both existing (previously lived-in) and newly built homes. Here’s a look at those two bright spots for buyers right now and why they may make it a bit easier to find the home you’re been looking for.

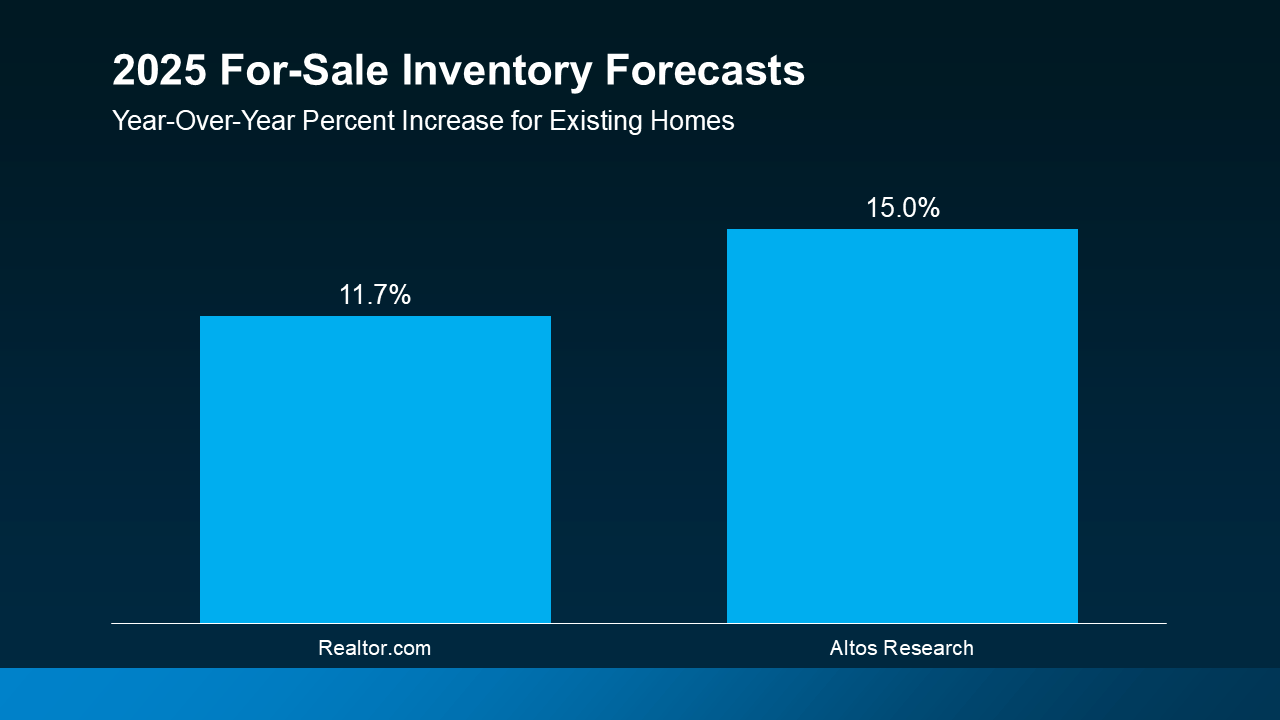

1. There Are 22% More Existing Homes for Sale

Data from Realtor.com says the number of existing homes for sale improved by an impressive 22% in 2024. And experts say your pool of options is expected to get even better this year. Forecasts show inventory is projected to grow another 11-15% by the end of this year (see graph below):

Here’s why this is so good for your search. If you haven’t seen a house with all the features you need, just know that, as the number of homes for sale grows, you’ll have more options to choose from. That means a better chance of finding a home that checks all your boxes. As Ralph McLaughlin, Senior Economist at Realtor.com,says:

“It could be a particularly good time to get out into the market . . . you’re going to have more choice. And that’s not something that buyers have really had much over the past several years.”

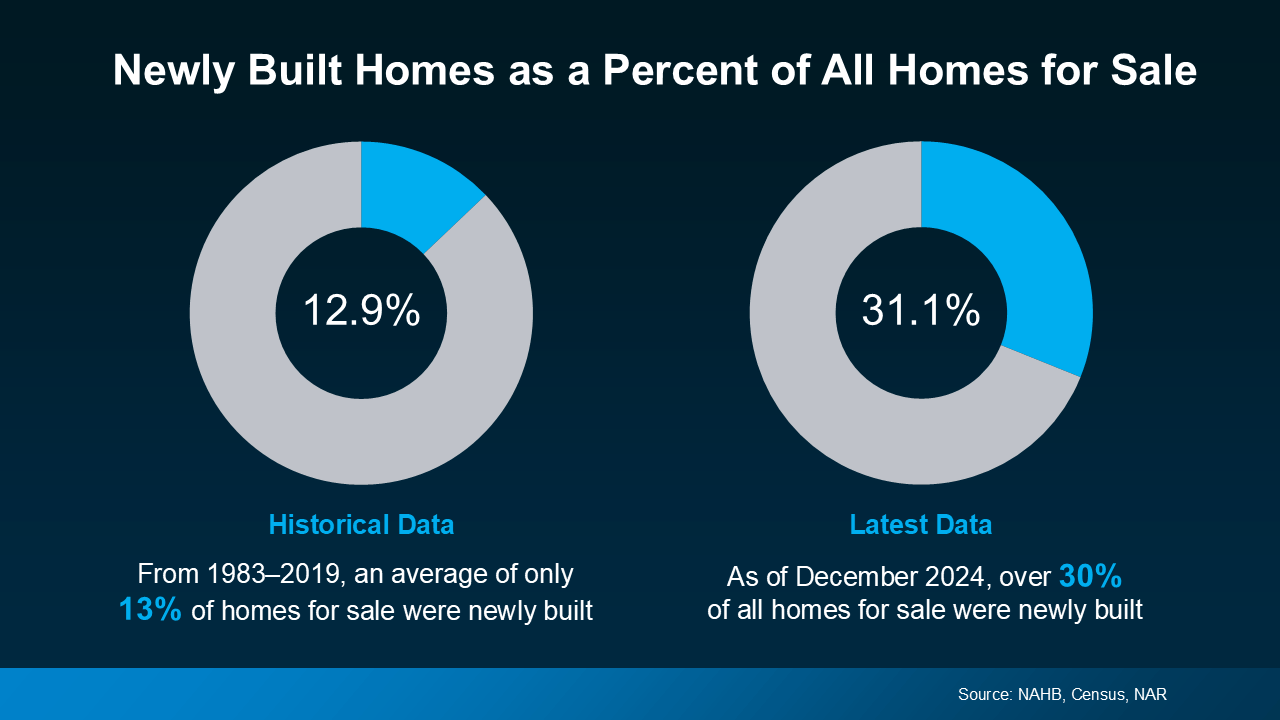

2. There Are More Newly Built Homes on the Market

According to data from the Census and the National Association ofRealtors (NAR), 31.1%, or roughly 1 in 3, homes on the market right now are newly built homes. That’s more than the norm (see charts below). But don’t worry, that’s not because builders are overdoing it – it’s just that they’re trying to catch up after years of underbuilding.

And the best part is, since builders have been focusing on smaller homes with lower price points, you may actually find out new builds are less expensive than you’d expect. So, while a lot of people write off new construction because it’s easy to assume the costs are way higher, lately, that price gap isn’t as big as you’d think. As CNET says:

“If you live in an area where there’s a lot of new construction happening . . . you might be able to purchase a new house for a price similar to or even less than a pre-owned one.”

If you haven’t been able to find a home that’s in your budget, it’s time to ask your agent about new builds. If you don’t, you may have been cutting your pool of options by about a third.

Bottom Line

More choices could be the key to unlocking your homebuying goals in 2025. Talk to a local agent if you want to see what’s available in your area.

What features are you looking for in your next home? Let an agent know so they can put together a list of homes you’d love.

A recent report from Realtor.comsays 20% of Americans don’t think homeownership is achievable. Maybe you feel the same way. With inflation driving up day-to-day expenses, saving enough to buy your first home is more of a challenge. But here’s the thing. With the right resources and help, you can still make it happen.

There are options that can help make buying a home possible today — even if your savings are limited or your credit isn’t perfect. Let’s explore just two of the solutions that could help get you into your first home no matter the market.

1. FHA Loans

If your down payment savings and your credit score aren’t where you want them to be, an FHA loan could be your pathway to buying a home. According to the U.S. Department of Housing and Urban Development (HUD) and Bankrate, the big perks of an FHA home loan are:

Lower Down Payments: They typically require a smaller down payment than conventional loans, sometimes as low as 3.5% of the home’s purchase price.

Lower Credit Score Requirements: They’re designed to help buyers with credit scores that might not qualify for conventional financing. This means, when conventional loans aren’t an option, you may still be able to get an FHA loan.

The first step is to connect with a lender who can help you explore your options and determine if you qualify.

2. Homeownership Assistance Programs

And if you need a more budget-friendly down payment, that’s not your only option. Did you know there are over 2,000 homeownership assistance programs available across the U.S. according to Down Payment Resource? And more than 75% of these programs are designed to help buyers with their down payment. Here’s a bit more information about why these could be such powerful tools for you:

Financial Support: The average benefit for buyers who qualify for down payment assistance is $17,000. And that’s not a small number.

Stackable Benefits: To make it even better, in some cases, you may be able to qualify for multiple programs at once, giving your down payment an even bigger boost.

Rob Chrane, CEO of Down Payment Resourceconfirms a little-known fact:

“Some of these programs can be layered. And so, in other words, you may not be limited to just one program.”

If you want to learn more or see what you qualify for, be sure to lean on the pros. A trusted real estate agent and a lender can guide you through the process, explain the help that’s out there, and connect you with resources to make buying a home a reality.

Bottom Line

If you’re ready to stop wondering if buying a home is possible and start exploring solutions, connect with an expert agent and trusted lender.