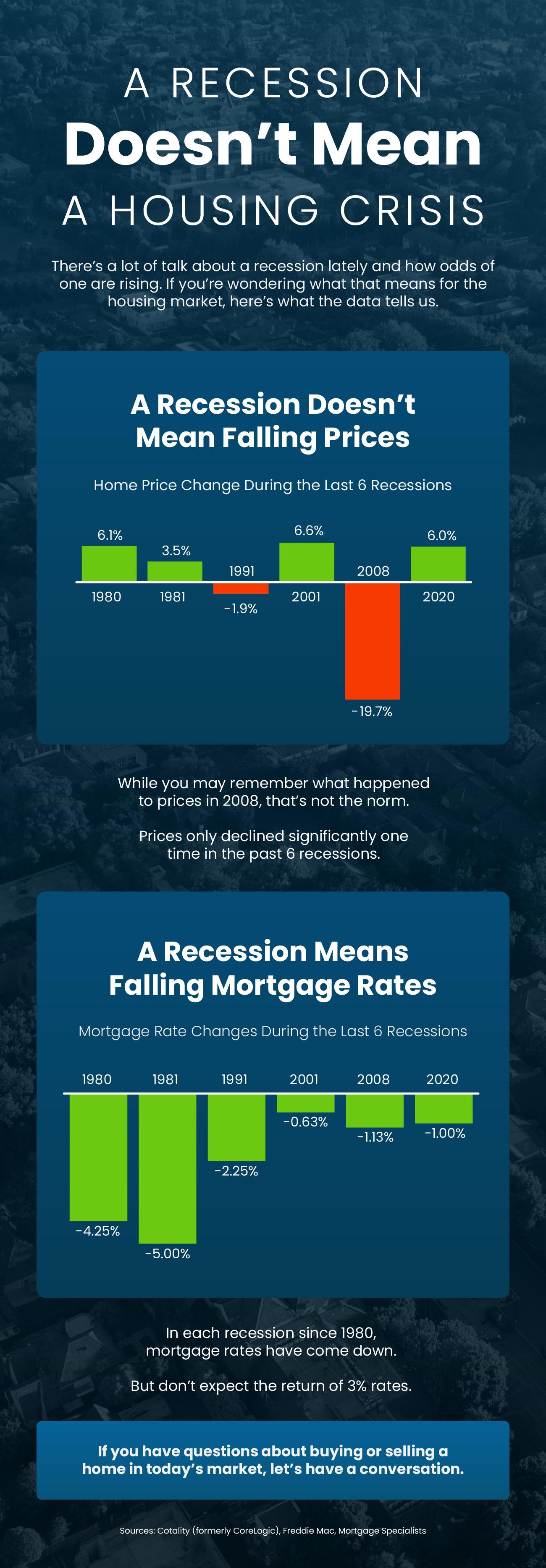

What an Economic Slowdown Could Mean for the Housing Market

Talk about the economy is all over the news, and the odds of a recession are rising this year. That’s leaving a lot of people wondering what it means for the value of their home – and their buying power.

Let’s take a look at some historical data to show what’s happened in the housing market during each recession, going all the way back to the 1980s. The facts may surprise you.

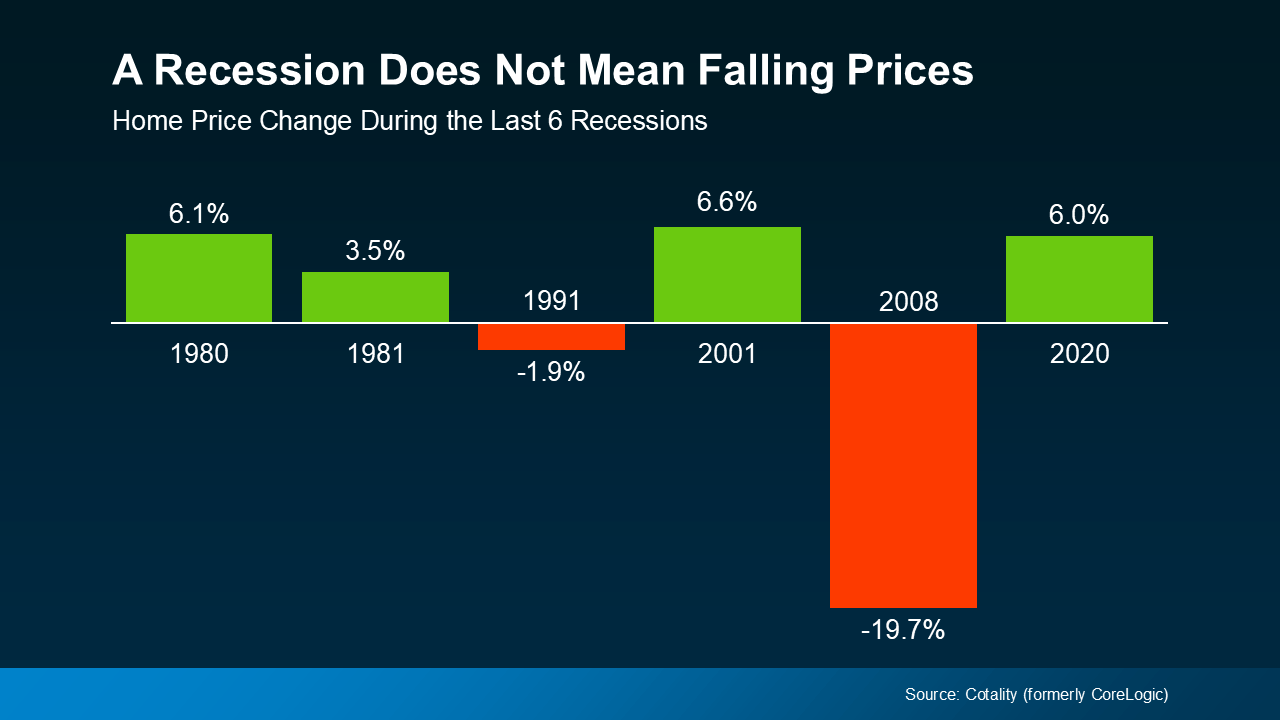

A Recession Doesn’t Mean Home Prices Will Fall

Many people think that if a recession hits, home prices will fall like they did in 2008. But that was an exception, not the rule. It was the only time the market saw such a steep drop in prices. And it hasn’t happened since, mainly because inventory is still so low overall. Even in markets where the number of homes for sale has started to rise this year, inventory is still far below the oversupply of homes that led up to the housing crash.

In fact, according to data from Cotality (formerly CoreLogic), in four of the last six recessions, home prices actually went up (see graph below)

So, don’t assume a recession will lead to a significant drop in home values. The data simply doesn’t support that idea. Instead, home prices usually follow whatever trajectory they’re already on. And right now, nationally, home prices are still rising, just at a more normal pace.

So, don’t assume a recession will lead to a significant drop in home values. The data simply doesn’t support that idea. Instead, home prices usually follow whatever trajectory they’re already on. And right now, nationally, home prices are still rising, just at a more normal pace.

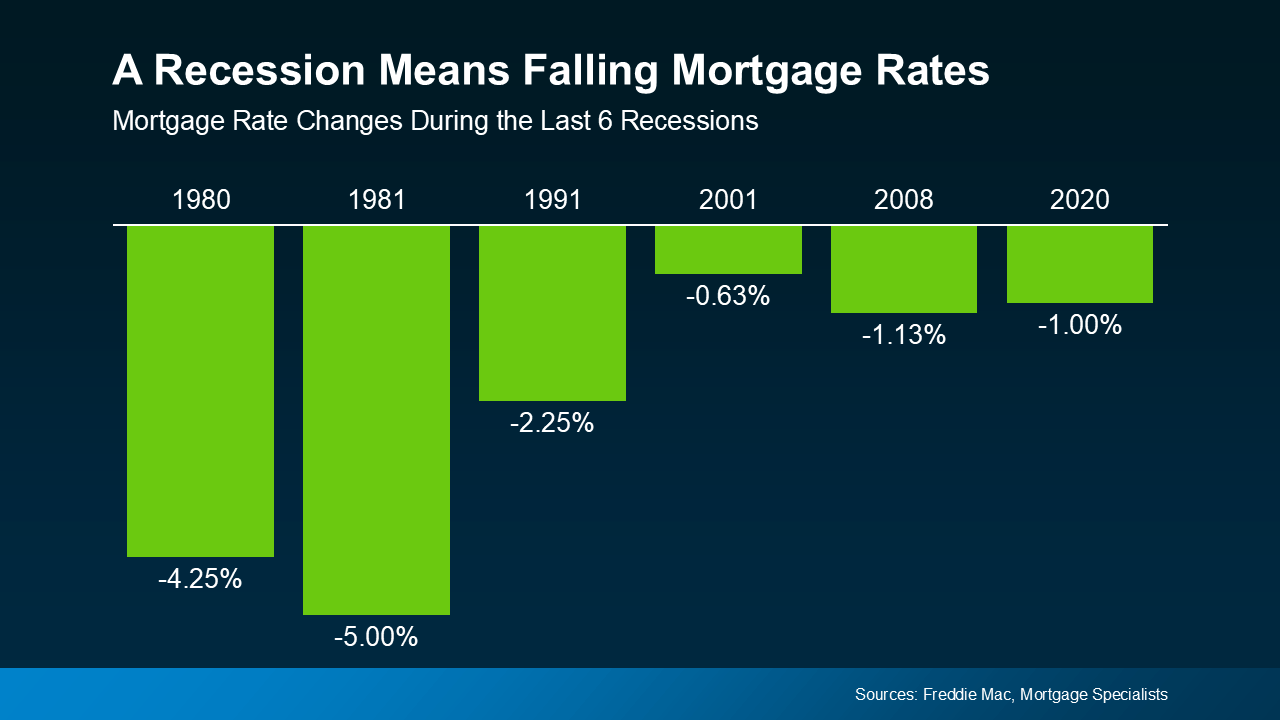

Mortgage Rates Typically Decline During Recessions

While home prices tend to stay on their current path, mortgage rates usually drop during economic slowdowns. Again, looking at data from the last six recessions, mortgage rates fell each time (see graph below):

So, a recession means rates could decline. And while that would help with your buying power, don’t expect the return of a 3% rate.

So, a recession means rates could decline. And while that would help with your buying power, don’t expect the return of a 3% rate.

Bottom Line

The answer to the recession question is still unknown, but the odds have gone up. However, that doesn’t mean you have to worry about what it means for the housing market – or the value of your home. Historical data tells us what usually happens.

If you’re wondering how the current economy is impacting your local market, connect with an agent.