Even if you’re not looking to move right away, you may have questions about how the election will impact the housing market.

When we look at historical trends, combined with what’s happening right now, we can find your answers. Based on historical data, mortgage rates decrease in the months before and home prices and sales increase the year after the election.

The facts show Presidential elections only have a small and temporary impact on the housing market.

With the 2024 Presidential election fast approaching, you might be wondering what impact, if any, it’s having on the housing market. Let’s break it down.

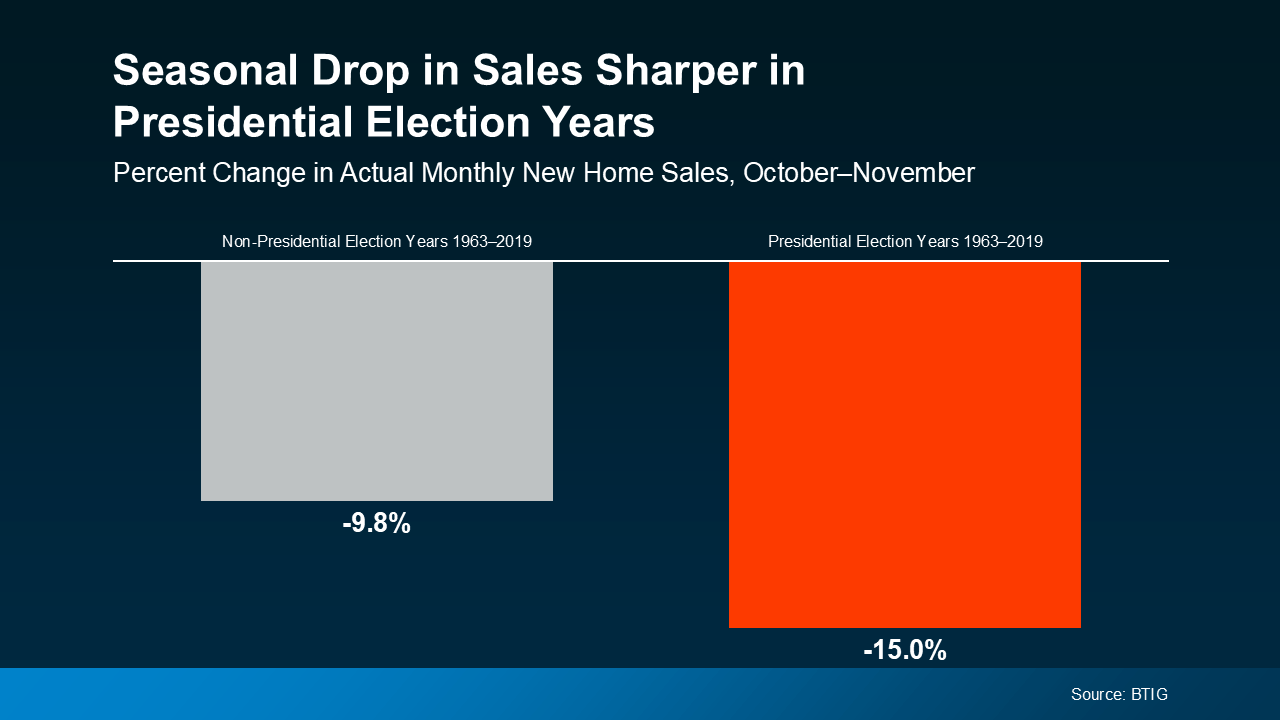

Election Years Bring a Temporary Slowdown

In any given year, home sales slow down slightly in the fall. It’s a typical, seasonal trend. However, according to data from BTIG, in election years there’s usually a slightly larger dip in home sales in the month leading up to Election Day (see graph below):

Why? Uncertainty. Many consumers hold off on making major decisions or purchases while they wait to see how the election will play out. It’s a pattern that’s shown up time and time again, and it’s particularly apparent for buyers and sellers in the housing market.

This year is no different. A recent survey from Redfin found that 23% of potential first-time homebuyers said they’re waiting until after the election to buy. That’s nearly a quarter of first-time buyers hitting the pause button, likely due to the same feelings of uncertainty.

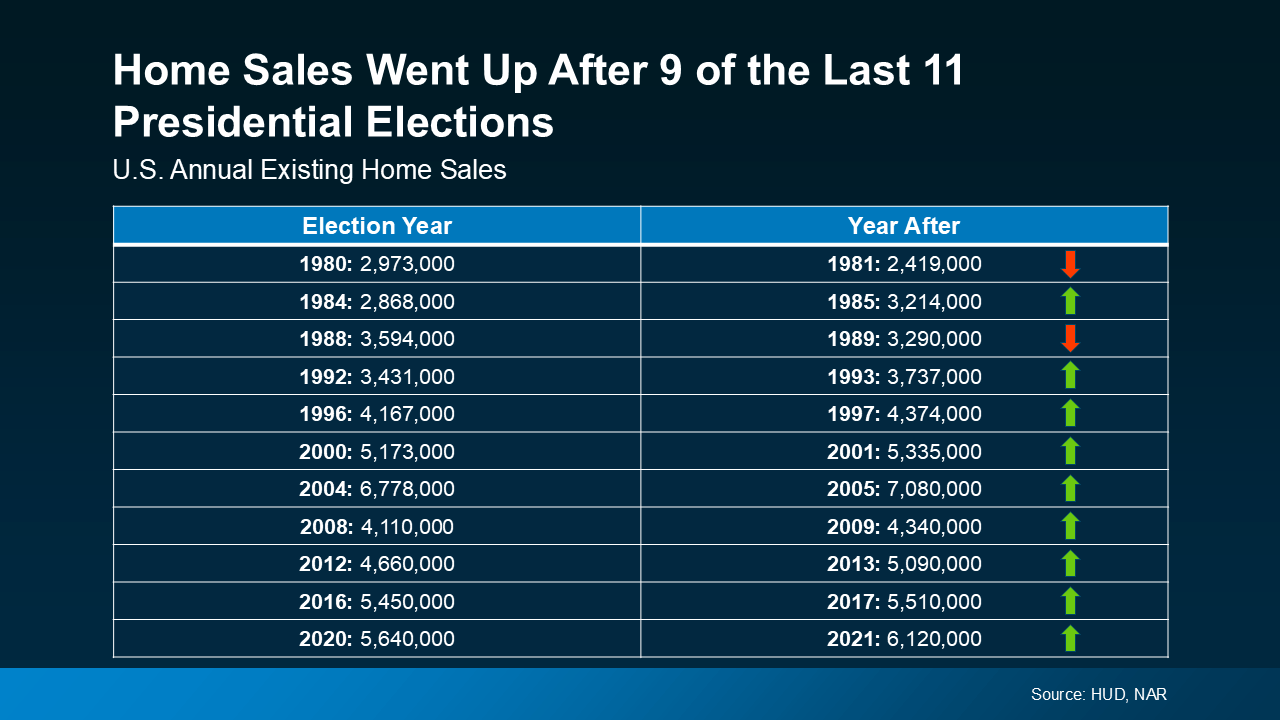

Home Sales Bounce Back After the Election

The good news is these delayed sales aren’t lost forever—they’re just postponed. History shows sales tend to rebound after the election is over. In fact, home sales have actually increased 82% of the time in the year after the election (see chart below):

That’s because once the election dust settles, buyers and sellers have a sense of what’s ahead and generally feel more confident moving forward with their decisions. And that leads to a boost in home sales.

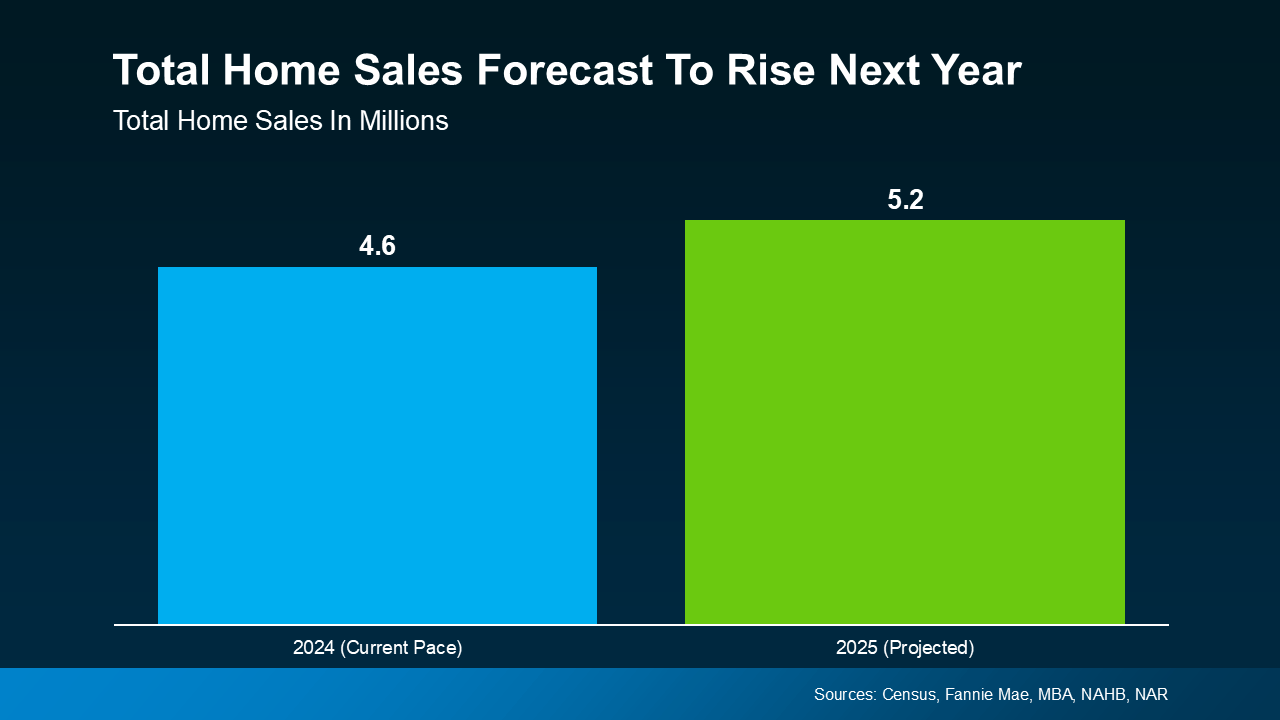

What To Expect in 2025

If history is any indicator, that means more homes will sell next year. And based on the latest forecasts, that’s exactly what you should expect. As the graph below shows, the housing market is on pace to sell a total of 4.6 million homes this year, and projections are for 5.2 million total sales next year (see graph below):

And that aligns with the typical pattern of post-election rebounds.

So, while it might feel like the market is slowing down right now, it’s more of a temporary dip rather than a long-term trend. As has been the case before, once the election uncertainty passes, buyers and sellers will return to the market.

Bottom Line

It’s important to remember that while election years often bring a short-term slowdown in the housing market, the pause is usually temporary. Those sales are not lost. Data shows home sales typically increase the year after a Presidential election, and current forecasts indicate 2025 will be no different. If you’re waiting for a clearer picture before making a move, just know that the market is expected to pick up speed in the months ahead.

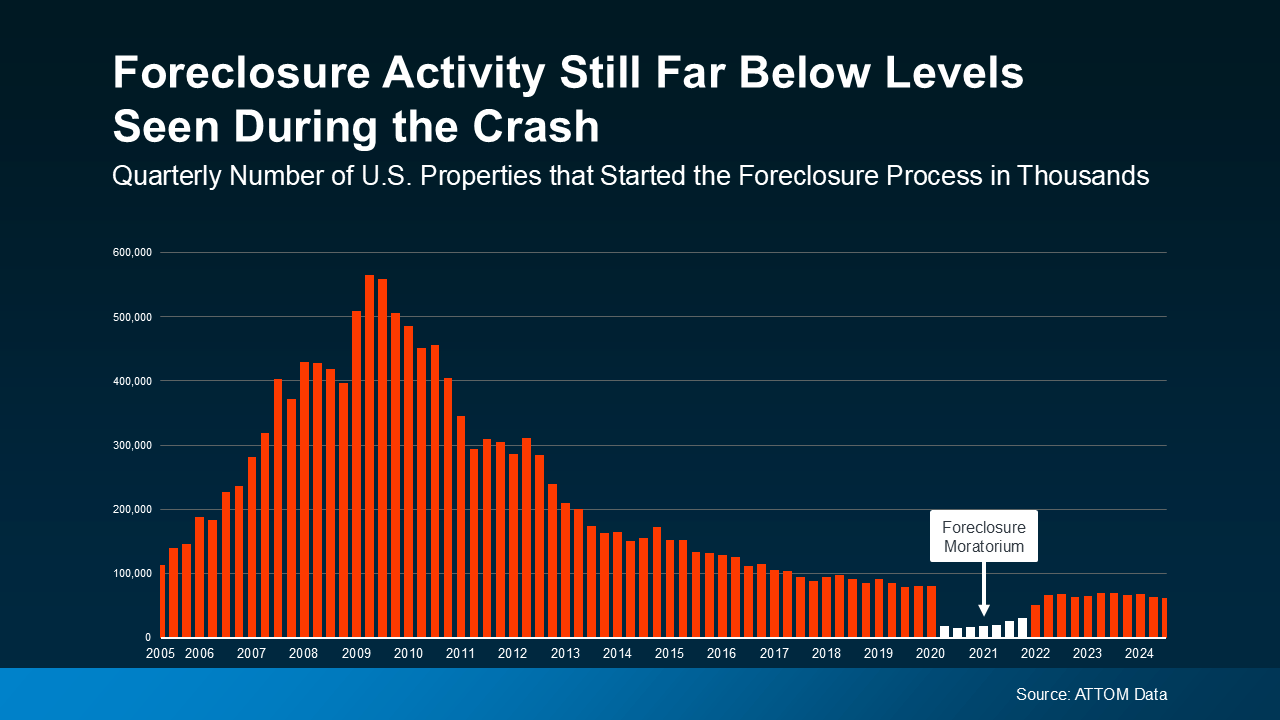

With everything feeling more expensive these days, it’s natural to worry about how rising costs might impact the housing market. Many people are concerned that high prices and tighter budgets could cause more homeowners to fall behind on their mortgage payments, leading to a wave of foreclosures.

But before you start worrying about a housing market crash, here’s a look at what’s really happening. And the good news is: the latest foreclosure data shows there’s no wave on the horizon.

How Today’s Market Is Different from 2008

Let’s ease those fears by looking at the bigger picture. The graph below uses research from ATTOM, a property data provider, to show that the number of homeowners starting the foreclosure process is nowhere near what we saw coming out of 2008. Back then, there was a big spike in how many foreclosures were happening. Today, the number is much lower – it’s even dropped some in the latest report. There’s a big difference between what’s happening now, and what happened when the housing market crashed (see graph below):

Just in case you’re wondering why the number of foreclosure filings has ticked up slightly since 2020 and 2021, here’s what you need to know. During those years, there was a moratorium (shown in white) designed to help millions of homeowners avoid foreclosure in challenging times. That’s why the numbers for just a few years ago were so incredibly low. If you look further back, it’s clear overall foreclosure filings are down significantly.

And if you’re wondering: how are there fewer foreclosures today, even when the cost of living has gotten so pricey? Here’s your answer. One of the main reasons is that homeowners today have a lot more equity built up in their homes than they did back in 2008. As an article from Bankrate explains:

“In the years after the housing crash, millions of foreclosures flooded the housing market, depressing prices. That’s not the case now. Most homeowners have a comfortable equity cushion in their homes.”

This equity acts like a safety net and is allowing many homeowners to avoid going into foreclosure if they’re facing financial hardships.Even if someone is struggling to make their monthly payments, they may be able to sell their home and avoid foreclosure altogether. This is a far cry from the conditions during the crash when homeowners owed more on their mortgages than their homes were worth.

What’s Ahead for the Housing Market

It’s true that today’s higher cost of living across the board is a challenge for many people right now. But this doesn’t mean we’re heading for a surge in foreclosures.

The equity cushion that people have is helping to keep foreclosure filings low. Today’s homeowners have more options to avoid going into foreclosure.

Bottom Line

Yes, everyday costs for gas and food have gotten more expensive—but that doesn’t mean the housing market is on the brink of another foreclosure crisis. Data shows the market is far from a foreclosure wave. Homeowners today are in a much stronger financial position than they were during the 2008 crash, thanks to significant equity.

You may have heard chatter recently about the economy and talk about a possible recession. It’s no surprise that kind of noise gets some people worried about a housing market crash. Maybe you’re one of them. But here’s the good news – there’s no need to panic. The housing market is not set up for a crash right now.

“A housing market crash happens when home values plummet due to a lack of demand for homes or an oversupply.”

With that definition in mind, here are two reasons why this just isn’t on the horizon.

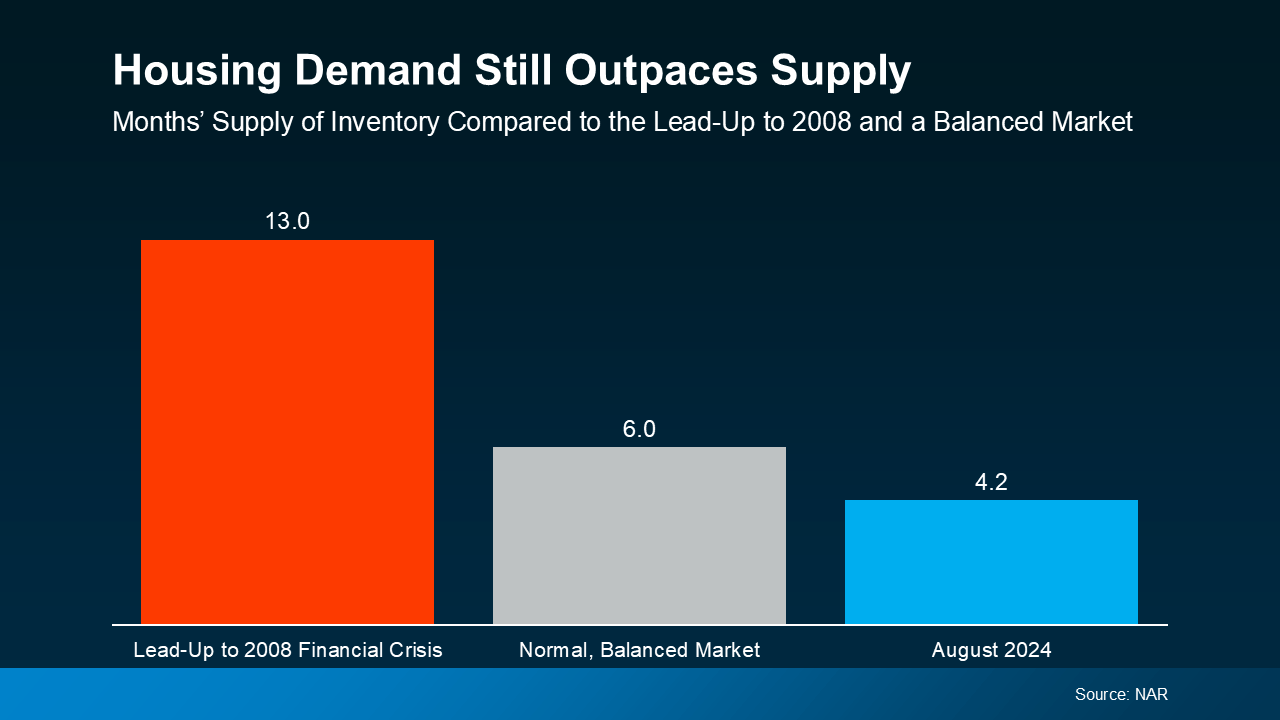

1. Demand for Homes Is Higher than Supply

One of the biggest reasons the housing market crashed back in 2008 was an oversupply of homes. Today, though, it’s a very different story.

It’s a general rule of thumb that a market where supply and demand are balanced has a six-month supply of homes. A higher number means supply outpaces demand, and a lower number means demand outpaces supply. The graph below uses data from NAR to put today’s situation into context:

The graph compares housing supply during three different periods of time. The red bar shows there were 13 months of supply before the 2008 crisis, which was far too much. The gray bar shows a balanced market with six months of supply, for context. And the blue bar shows there are only 4.2 months of supply today.

Put simply, there are more people who want to buy homes than there are homes available to buy right now. So, demand is greater than supply. When that happens, home prices stay steady or rise – the opposite of a housing market crash.

It’s important to note that inventory levels differ from market to market. Some areas may be more balanced, while a few could have a slight oversupply, which can impact prices locally. However, most markets continue to experience a shortage of homes.

Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“We simply don’t have enough inventory. Will some markets see a price decline? Yes. [But] with the supply not being there, the repeat of a 30 percent price decline is highly, highly unlikely.”

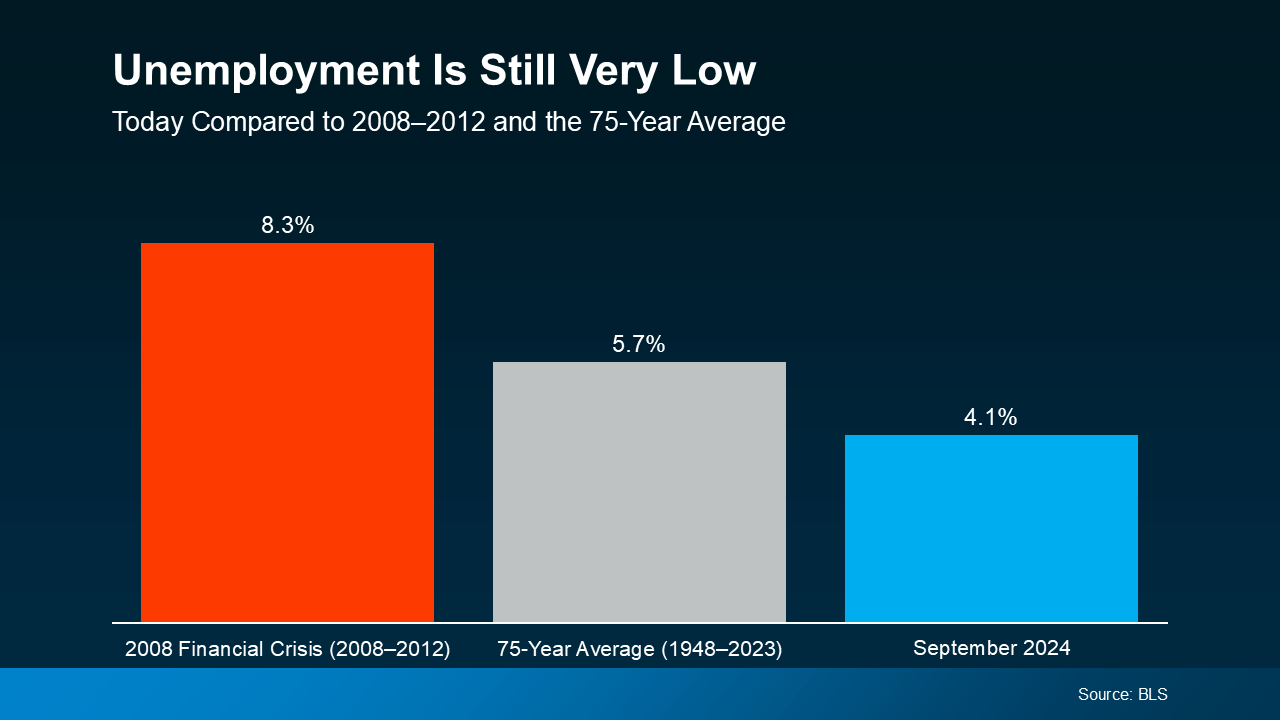

2. Unemployment Is Still Low

When people are unemployed, they’re more likely to have trouble making their mortgage payments and may be forced to sell or face foreclosure. That was a big problem during the 2008 financial crisis. Today, the employment situation is much more stable (see graph below):

Again, this graph shows three different periods of time, but this one is the unemployment rate. The red bar represents the 2008 financial crisis when unemployment was very high at 8.3%. The gray bar shows the 75-year average of 5.7%. And the blue bar shows the unemployment rate today, and it’s much lower at just 4.1%.

Right now, people are working, earning an income, and making their mortgage payments. That’s one reason why the wave of foreclosures that happened in 2008 isn’t going to happen again this time. Plus, since so many people are employed right now, many are actually in a position to buy a home, and this demand keeps upward pressure on prices.

Today’s Housing Market Is Stronger than in 2008

While it’s understandable to be concerned when you hear talk of a recession and economic uncertainty, but know this: the housing market is in a much better place than it was in 2008. According to Rick Sharga, Founder and CEO at CJ Patrick Company:

“Literally everything is different about today’s housing market dynamics than the conditions that led to the housing crisis.”

Demand for homes still outpaces supply, and unemployment remains low. And these are two key factors that will help prevent the housing market from crashing any time soon.

Bottom Line

The housing market is in a much better place than it was in 2008, but it’s important to remember that real estate is very local.

So, it’s always a good idea to stay informed about your specific market. If you have any questions or want to discuss how these factors are playing out in your area, reach out to a local real estate agent.