If you’re like a lot of aspiring homebuyers, there’s a major hurdle standing in your way — the cost of living. From groceries to gas, eggs, and just about everything else, prices have gone up. And that rings true for home prices, too.

But even when everything feels expensive, there are still ways to make homeownership more than an item on your wish list. You may just need to think about where you plan to buy a bit differently.

Think of Your First Home as a Stepping Stone

One of the biggest misconceptions among buyers is that their first home has to be their forever home – or that it has to check all the boxes of what they want right out of the gate. In reality, it’s just a starting point.

Once you own a home, you start to build equity, which grows over time as home prices rise. Down the road, if you want to move — whether to a larger space, a better location, or both — the equity you’ve gained can help you do just that.

So rather than waiting until you can afford your dream home in your ideal neighborhood, consider starting with something that works for now.

Expand Your Search To Find More Affordable Options

If high home prices in your favorite area are holding you back, it’s time to cast a wider net. By keeping an open mind and being flexible with location, you may be surprised at what’s possible within your budget. Many buyers find success by looking in surrounding areas – and some even choose to move out of state.

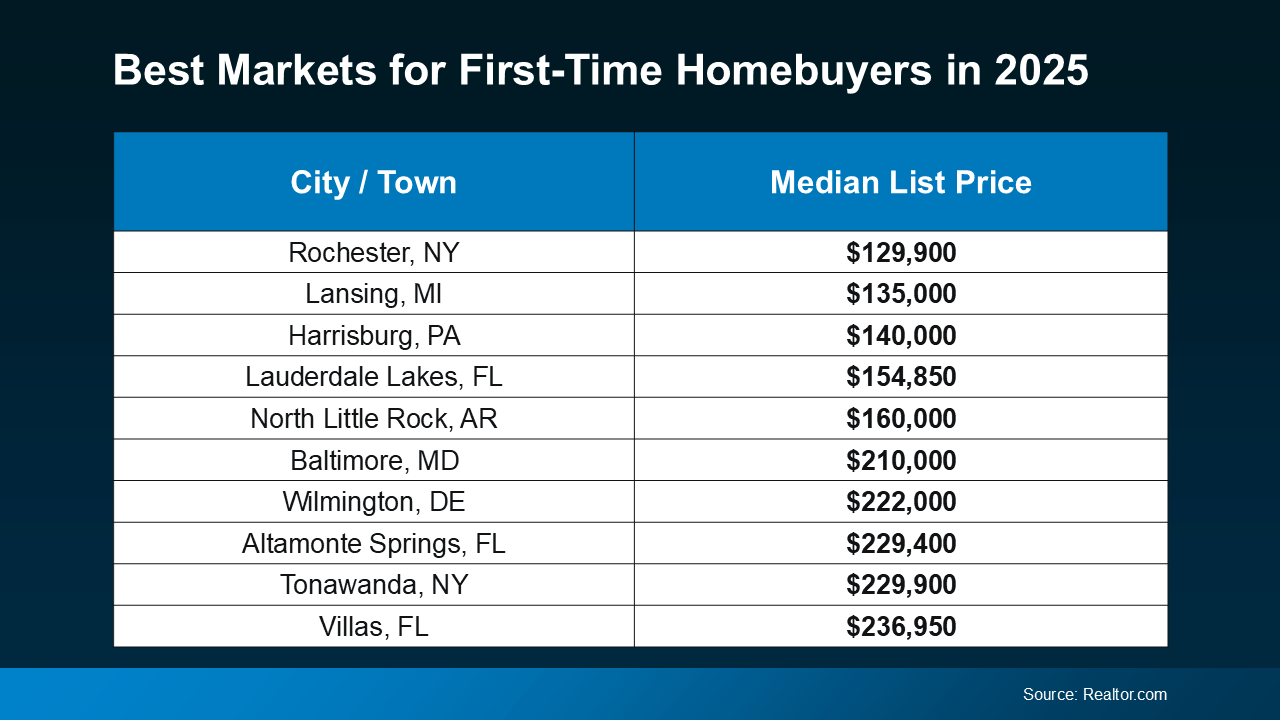

According to a report from Realtor.com, these are some of the best markets for first-time homebuyers this year (see chart below):

Of course, moving to a different state isn’t for everyone – and isn’t a necessity. The right agent can help you find more cost-effective options wherever you are.

If you want to stay local, looking just outside your preferred neighborhood could help you find something you can afford that’s still pretty close to your favorite restaurants, shops, and activities. Sometimes, moving as little as 10 minutes away makes a big difference.

And the best way to see what’s available is to work with a real estate agent who understands the local market and can help you identify hidden gems nearby. An agent can point you to communities you may not have considered that have lower price tags now and are steadily gaining value and appeal. That way you can buy your first home and be set up to gain equity through the years.

Bottom Line

Today’s cost of living is a challenge for many homebuyers. But by exploring different areas and working with a knowledgeable agent, you can take that first step toward owning a home — and building equity for your future.

How far outside of your area would you look to make homeownership happen? Connect with a local agent to chat through your options.

A recent report from Realtor.comsays 20% of Americans don’t think homeownership is achievable. Maybe you feel the same way. With inflation driving up day-to-day expenses, saving enough to buy your first home is more of a challenge. But here’s the thing. With the right resources and help, you can still make it happen.

There are options that can help make buying a home possible today — even if your savings are limited or your credit isn’t perfect. Let’s explore just two of the solutions that could help get you into your first home no matter the market.

1. FHA Loans

If your down payment savings and your credit score aren’t where you want them to be, an FHA loan could be your pathway to buying a home. According to the U.S. Department of Housing and Urban Development (HUD) and Bankrate, the big perks of an FHA home loan are:

Lower Down Payments: They typically require a smaller down payment than conventional loans, sometimes as low as 3.5% of the home’s purchase price.

Lower Credit Score Requirements: They’re designed to help buyers with credit scores that might not qualify for conventional financing. This means, when conventional loans aren’t an option, you may still be able to get an FHA loan.

The first step is to connect with a lender who can help you explore your options and determine if you qualify.

2. Homeownership Assistance Programs

And if you need a more budget-friendly down payment, that’s not your only option. Did you know there are over 2,000 homeownership assistance programs available across the U.S. according to Down Payment Resource? And more than 75% of these programs are designed to help buyers with their down payment. Here’s a bit more information about why these could be such powerful tools for you:

Financial Support: The average benefit for buyers who qualify for down payment assistance is $17,000. And that’s not a small number.

Stackable Benefits: To make it even better, in some cases, you may be able to qualify for multiple programs at once, giving your down payment an even bigger boost.

Rob Chrane, CEO of Down Payment Resourceconfirms a little-known fact:

“Some of these programs can be layered. And so, in other words, you may not be limited to just one program.”

If you want to learn more or see what you qualify for, be sure to lean on the pros. A trusted real estate agent and a lender can guide you through the process, explain the help that’s out there, and connect you with resources to make buying a home a reality.

Bottom Line

If you’re ready to stop wondering if buying a home is possible and start exploring solutions, connect with an expert agent and trusted lender.

Turning a dream into reality starts with one thing: a plan. And if buying your first home is on your list of goals, now’s the perfect time to put a plan in motion to help you save.

And the best part? Reaching your savings goal doesn’t mean making huge sacrifices overnight – small, consistent steps can get you there over time. Here are a few strategies that can help speed up the process.

Step 1: Build a Budget That Works for You

Knowing where your money’s going is the first step to saving more of it. Take some time to track the money you’ve got coming in and going out. This helps you spot areas where you’re spending more than you realize. It also helps to give yourself some guidelines on what you want to spend for groceries, gas, and more – try to stick to whatever caps you put on each spending category.

Step 2: Cut Down on Any Extras (It Adds Up)

Once you’ve got a clear budget, it’s time to tighten up. Look for areas where you can cut down your costs – like services you don’t really need – or ways you can reduce recurring expenses and put that money in your house fund instead. Every dollar you save now brings you closer to your future house. As Bankrate says:

“If you’re saving for a house, cutting back on your spending can help. Start with cutting unnecessary expenses, like subscription services, entertainment, delivery services or eating out. If possible, negotiate down recurring monthly or annual expenses, such as getting a better car insurance rate or reducing an internet bill . . . .”

Step 3: Automate Your Savings

Consistency is the real game-changer. If you have to transfer money manually, you may forget to do it. That’s why setting up automatic transfers to a dedicated savings account makes it easier to save regularly. Even apps that round up purchases to the nearest dollar and save the difference can help you build momentum without effort. As an article from Forbes explains:

“Automating your savings helps to keep your progress toward your goal consistent. Set up automatic transfers from your checking account to a dedicated savings account. This will help you prioritize saving and minimize the chances of spending your money on other things.”

Step Four: Put Any Extra Money To Work

Got a tax refund, work bonus, or a cash gift? Don’t fall into the temptation to spend it on something you don’t actually need. Use those unexpected boosts to make big strides toward your savings goal. Treating this extra cash as an opportunity, not just a nice surprise, will help you get there faster.

Bottom Line

Saving for your first house isn’t about perfection – it’s about progress. A solid plan, a little discipline, and a clear goal will take you further than you think. If you’re ready to make homeownership happen, connect with an agent. Together you can map out the next steps to get you closer to the keys to your first home.

Of course, moving to a different state isn’t for everyone – and isn’t a necessity. The right agent can help you find more cost-effective options wherever you are.

Of course, moving to a different state isn’t for everyone – and isn’t a necessity. The right agent can help you find more cost-effective options wherever you are.