Even if you’re not looking to move right away, you may have questions about how the election will impact the housing market.

When we look at historical trends, combined with what’s happening right now, we can find your answers. Based on historical data, mortgage rates decrease in the months before and home prices and sales increase the year after the election.

The facts show Presidential elections only have a small and temporary impact on the housing market.

With the 2024 Presidential election fast approaching, you might be wondering what impact, if any, it’s having on the housing market. Let’s break it down.

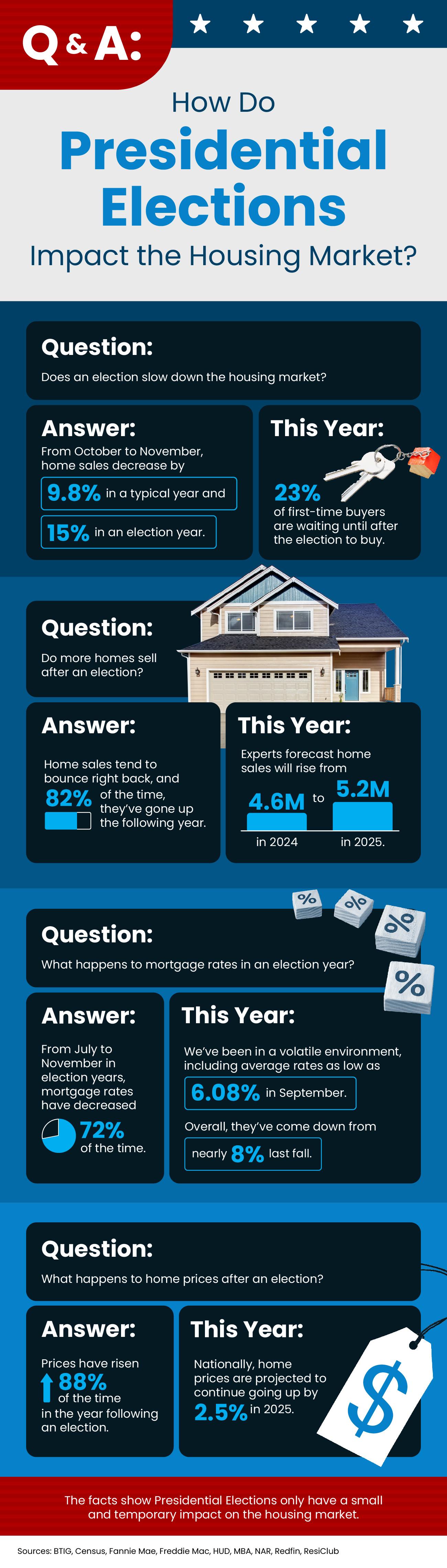

Election Years Bring a Temporary Slowdown

In any given year, home sales slow down slightly in the fall. It’s a typical, seasonal trend. However, according to data from BTIG, in election years there’s usually a slightly larger dip in home sales in the month leading up to Election Day (see graph below):

Why? Uncertainty. Many consumers hold off on making major decisions or purchases while they wait to see how the election will play out. It’s a pattern that’s shown up time and time again, and it’s particularly apparent for buyers and sellers in the housing market.

This year is no different. A recent survey from Redfin found that 23% of potential first-time homebuyers said they’re waiting until after the election to buy. That’s nearly a quarter of first-time buyers hitting the pause button, likely due to the same feelings of uncertainty.

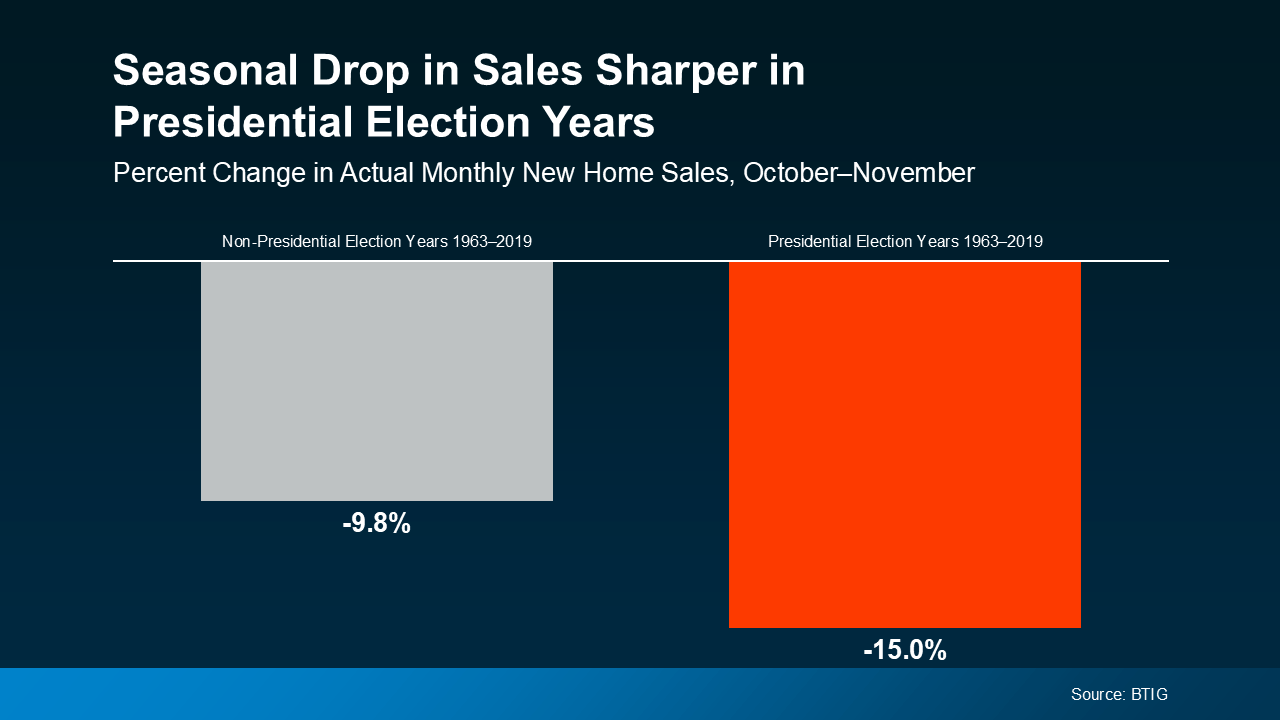

Home Sales Bounce Back After the Election

The good news is these delayed sales aren’t lost forever—they’re just postponed. History shows sales tend to rebound after the election is over. In fact, home sales have actually increased 82% of the time in the year after the election (see chart below):

That’s because once the election dust settles, buyers and sellers have a sense of what’s ahead and generally feel more confident moving forward with their decisions. And that leads to a boost in home sales.

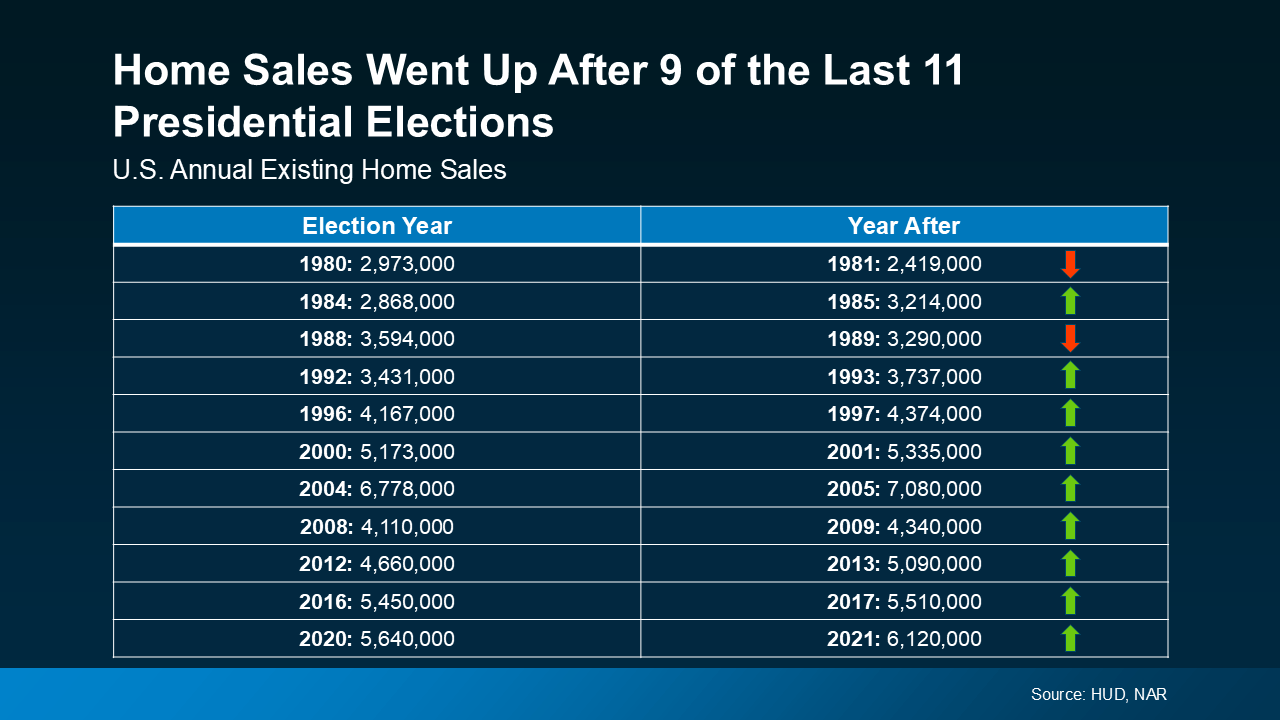

What To Expect in 2025

If history is any indicator, that means more homes will sell next year. And based on the latest forecasts, that’s exactly what you should expect. As the graph below shows, the housing market is on pace to sell a total of 4.6 million homes this year, and projections are for 5.2 million total sales next year (see graph below):

And that aligns with the typical pattern of post-election rebounds.

So, while it might feel like the market is slowing down right now, it’s more of a temporary dip rather than a long-term trend. As has been the case before, once the election uncertainty passes, buyers and sellers will return to the market.

Bottom Line

It’s important to remember that while election years often bring a short-term slowdown in the housing market, the pause is usually temporary. Those sales are not lost. Data shows home sales typically increase the year after a Presidential election, and current forecasts indicate 2025 will be no different. If you’re waiting for a clearer picture before making a move, just know that the market is expected to pick up speed in the months ahead.

Curious about where the housing market is headed in 2025? The good news is that experts are offering some promising forecasts, especially when it comes to two key factors that directly affect your decisions: mortgage rates and home prices.

Whether you’re thinking of buying or selling, here’s a look at what the experts are saying and how it might impact your move.

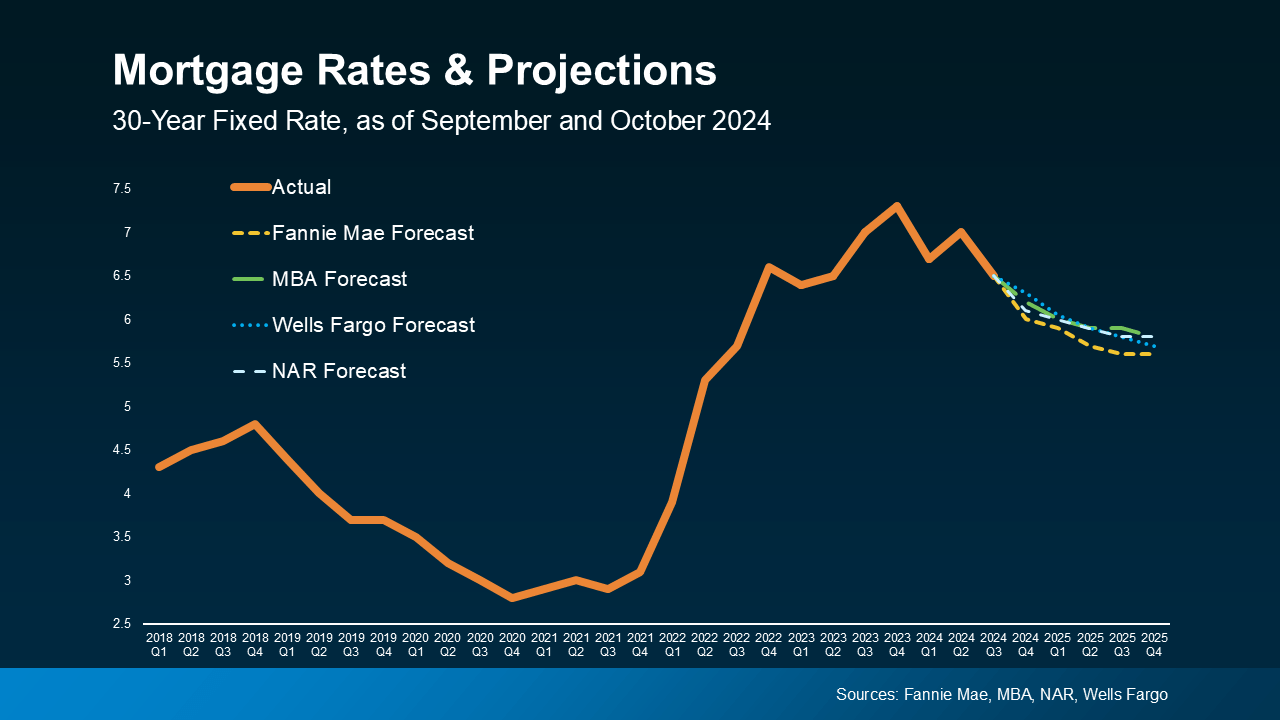

Mortgage Rates Are Forecast To Come Down

One of the biggest factors likely affecting your plans is mortgage rates, and the forecast looks positive. After rising dramatically in recent years, experts project rates will ease slightly throughout the course of 2025 (see graph below):

While that decline won’t be a straight line down, the overall trend should continue over the next year. Expect a few bumps along the way, because the trajectory of rates will depend on new economic data and inflation numbers as they’re released. But don’t get too hung up on those blips and reactions from the market as they happen. Focus on the bigger picture.

Lower mortgage rates mean improving affordability. As rates come down, your monthly mortgage payment decreases, giving you more flexibility in what you can afford if you buy a home.

This shift will likely bring more buyers and sellers back into the market, though. As Charlie Dougherty, Director and Senior Economist at Wells Fargo, explains:

“Lower financing costs will likely boost demand by pulling affordability-crunched buyers off of the sidelines.”

As that happens, both inventory and competition among buyers will ramp back up. The takeaway? You can get ahead of that competition now. Lean on your agent to make sure you understand how the shifts in rates are impacting demand in your area.

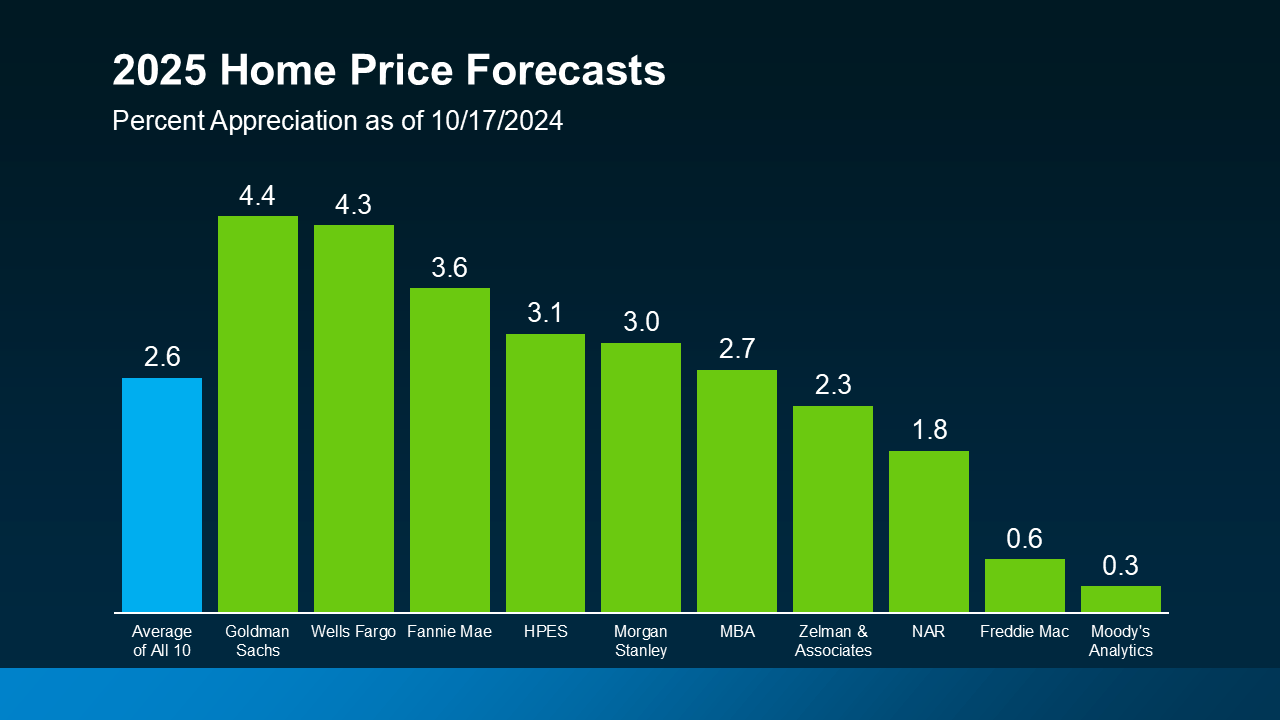

Home Price Projections Show Modest Growth

While mortgage rates are expected to come down slightly, home prices are forecast to rise—but at a much more moderate pace than the market has seen in recent years.

Experts are saying home prices will grow by an average of about 2.5% nationally in 2025 (see graph below):

This is far more manageable than the rapid price increases of previous years, which saw double-digit percentage growth in some markets.

What’s behind this ongoing increase in prices? Again, it has to do with demand. As more buyers return to the market, demand will rise – but so will supply as sellers feel less rate-locked.

More buyers in markets with inventory that’s still below the norm will put upward pressure on prices. But with more homes likely to be listed, supply will help keep price growth in check. This means that while prices will rise, they’ll do so at a healthier, more sustainable pace.

Of course, these national trends may not reflect exactly what’s happening in your local market. Some areas might see faster price growth, while others could see slower gains. As Lance Lambert, Co-Founder of ResiClub, says:

“Even if the average national home price forecast for 2025 is correct, it’s possible that some regional housing markets could see mild home price declines, while some markets could still see elevated appreciation. That has been, after all, the case this year.”

Even the few markets that may see flat or slightly lower prices in 2025 have had so much appreciation in recent years – it may not have a big impact. That’s why it’s important to work with a local real estate expert who can give you a clear picture of what’s happening where you’re looking to buy or sell.

Bottom Line

With mortgage rates expected to ease and home prices projected to rise at a more moderate pace, 2025 is shaping up to be a more promising year for both buyers and sellers.

If you have any questions about how these trends might impact your plans, connect with a local agent. That way you’ve got someone to help you navigate the market and make the most of the opportunities ahead.

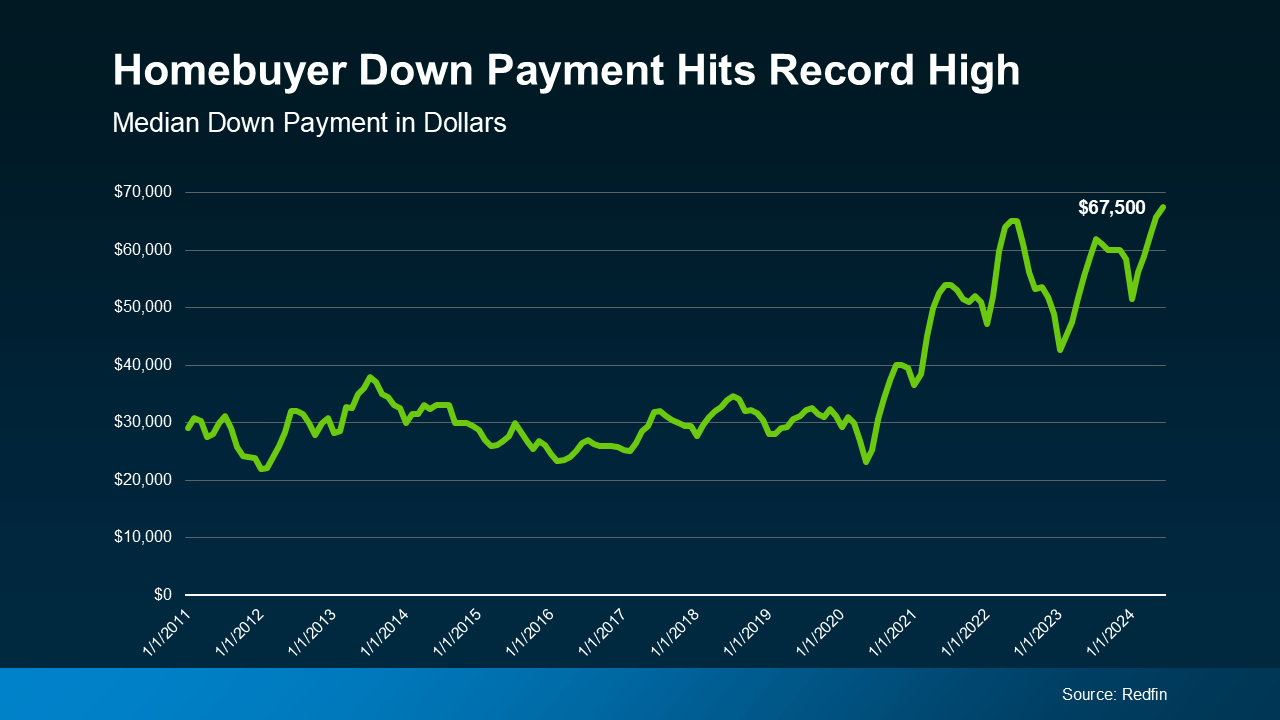

Did you know? Homeowners are often able to put more money down when they buy their next home. That’s because, once they sell, they can use the equity they have in their current house toward their next down payment. And it’s why as home equity reaches a new height, the median down payment has too.

According to the latest data from Redfin, the typical down payment for U.S. homebuyers is $67,500—that’s nearly 15% more than last year, and the highest on record (see graph below):

Here’s why equity makes this possible. Over the past five years, home prices have increased significantly, which has led to a big boost in equity for current homeowners like you. When you sell your house and move, you can take the equity that gives you and apply it toward a larger down payment on your new home. That’s a major opportunity, especially if you’ve had concerns about affordability.

Now, it’s important to remember you don’t have to make a big down payment to buy your next home—there are loan programs that let you put as little as 3%, or even 0% down. But there’s a reason so many current homeowners are opting to put more money down. That’s because it comes with some serious perks.

Why a Bigger Down Payment Can Be a Game Changer

1. You’ll Borrow Less and Save More in the Long Run

When you use your equity to make a bigger down payment on your next home, you won’t have to borrow as much. And the less you borrow, the less you’ll pay in interest over the life of your loan. That’s money saved in your pocket for years to come.

2. You Could Get a Lower Mortgage Rate

Providing a larger down payment shows your lender you’re more financially stable and not a large credit risk. The more confident your lender is in your credit score and your ability to pay your loan, the lower the mortgage rate they’ll likely be willing to give you. And that amplifies your savings.

3. Your Monthly Payments Could Be Lower

A bigger down payment doesn’t just help you reduce how much you have to borrow—it also means your monthly mortgage payment may be smaller. That can make your next home more affordable and give you a bit more breathing room in your budget.

4. You Can Skip Private Mortgage Insurance (PMI)

If you can put down 20% or more, you can avoid Private Mortgage Insurance (PMI), which is an added cost many buyers have to pay if their down payment isn’t as large. Freddie Mac explains it like this:

“For homeowners who put less than 20% down, Private Mortgage Insurance or PMI is an added insurance policy for homeowners that protects the lender if you are unable to pay your mortgage. It is not the same thing as homeowner’s insurance. It’s a monthly fee, rolled into your mortgage payment, that’s required if you make a down payment less than 20%.”

Avoiding PMI means you’ll have one less expense to worry about each month, which is a nice bonus.

Bottom Line

Down payments are at a record high, largely because recent equity gains are putting homeowners in a position to put more money down.

If you’re thinking about selling your current house and moving, reach out to a trusted real estate agent. They’ll help you figure out how much home equity you have right now, and how it can boost your buying power in today’s market.